Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

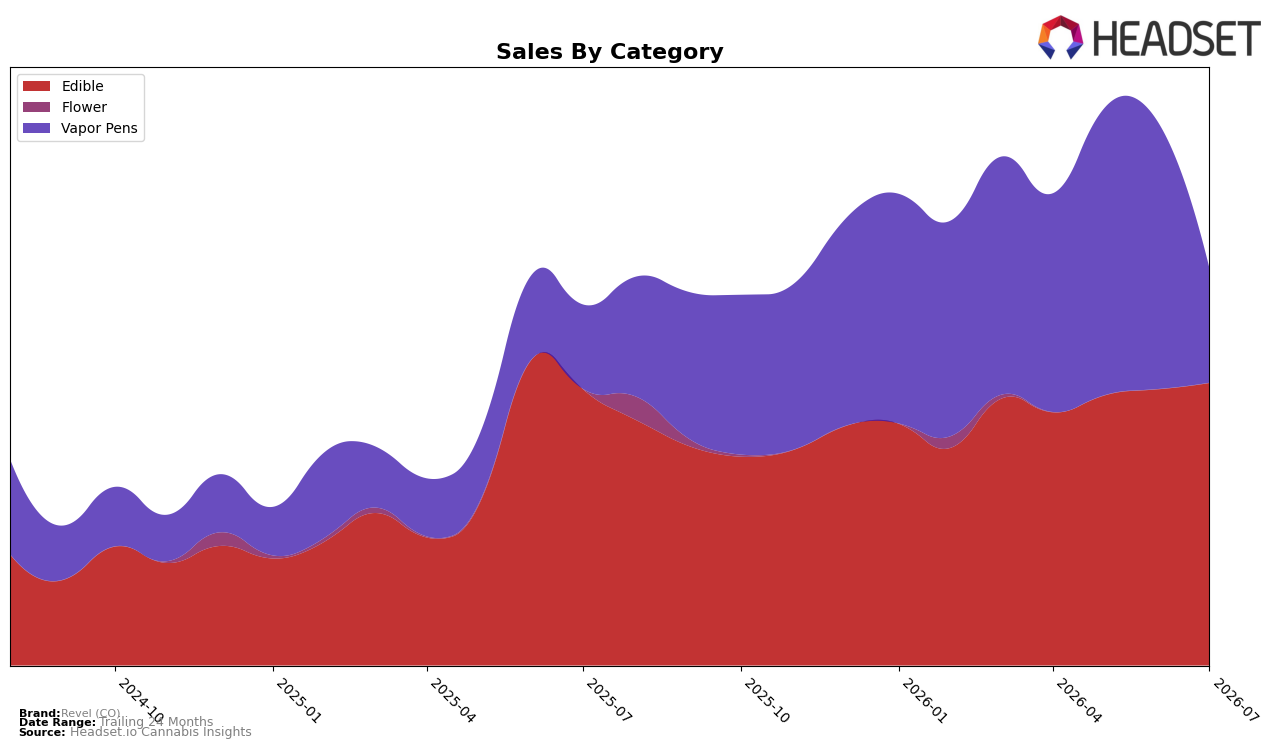

In July 2026, Revel (CO) concentrated 71.19% of sales in Edible, up 2.28% month over month and 2.29% year over year, while Vapor Pens accounted for 28.81% of sales but fell 57.18% month over month despite a 35.59% year-over-year gain. Average price rose 17.80% year over year to $13.17, with Edible priced at 10.95 and Vapor Pens at 26.49, and overall brand sales grew 10.08% year over year while 24‑month sales expanded 102.02%. With Edible anchoring the mix and holding a rank of 7 in Colorado Edible, the pattern implies Revel (CO) is leaning into a stable, price-accretive Edible base while accepting higher volatility in Vapor Pens to chase selective upside.

The shift—Edible share holding near 71.19% alongside a 2.28% MoM lift, versus Vapor Pens’ 57.18% MoM drop despite a 35.59% YoY rise—suggests Revel (CO) is optimizing for consistent Edible throughput and letting Vapor Pens function as a cyclical growth vector. With brand-level sales up 10.08% year over year and average price up 17.80% while maintaining a rank of 7 in Colorado Edible, the implication is that Revel (CO) is trading some short-term volume in higher-priced formats for margin and rank stability anchored in Edible, positioning the brand to prioritize price and shelf reliability over chasing volatile pen share.

Competitive Landscape

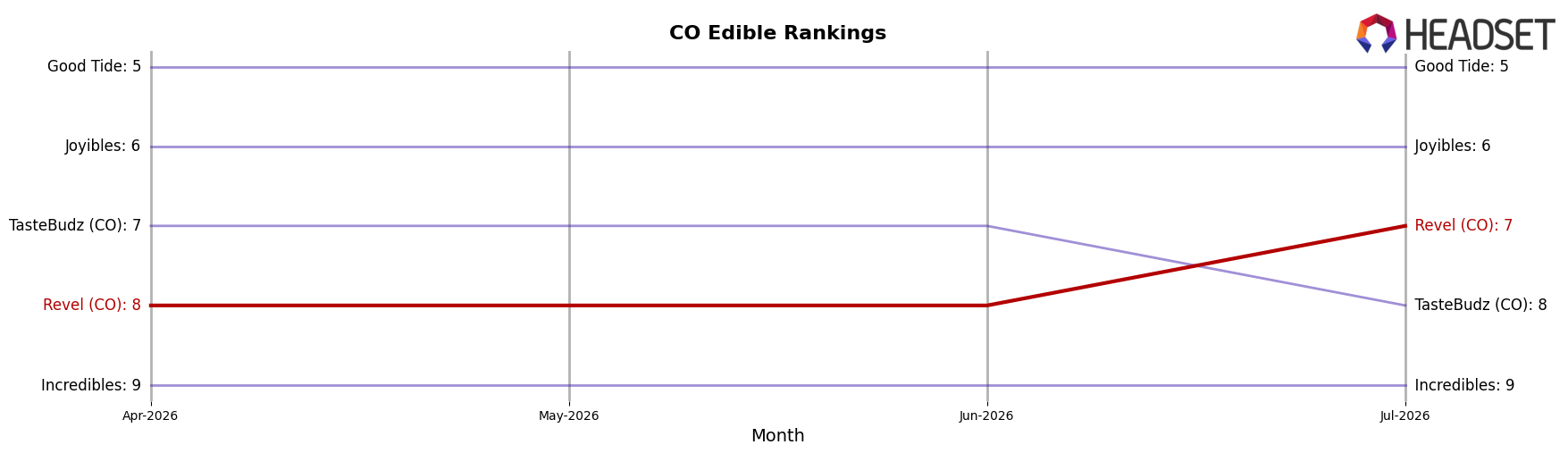

Revel (CO) sits at rank #7 in Colorado Edible for July 2026, improving 1 place from #8 year over year and up 1 place from #8 three months ago; this matches its peak rank of #7 in July 2026 while category leaders moved unevenly, with Wyld holding #1 year over year despite a 24.38% sales decline and Dialed In Gummies climbing from #3 to #2 on 15.80% growth. Meanwhile, Wana slipped from #2 to #3 alongside a 16.17% contraction, contrasted with Ript staying at #4 with 5.92% growth; the pattern implies Revel (CO)’s modest upward rank change is coming from relative stability against mixed competitor momentum, indicating headroom to convert small share gains into durable top-5 contention.

Notable Products

Pineapple Crown Distillate Disposable (2g) posted the steepest decline in July 2026, down 54.6% MoM and slipping to rank 8, while Wild Blueberry Distillate Disposable (2g) fell 48.3% MoM to rank 7, together signaling accelerated contraction in Vapor Pens versus Edibles holding ranks 1–5. At the top, THC/CBG 2:1 Uplifted Mango Tangerine Gummies 10-Pack (100mg THC, 50mg CBG) inched up 2.7% MoM to remain rank 1, and Energetic Lemon Lime Gummy (100mg) rose 10.8% MoM at rank 4, with five of the top ten as Edible SKUs concentrating demand away from inhalables. The THC/CBD/CBC 1:1:1 Relaxed Peach Lemonade Gummies 20-Pack (100mg THC, 100mg CBD, 100mg CBC) dipped 2.1% MoM but held rank 2, and total Edibles leadership contrasts with a Vapor Pens tier that includes a CBD:THC 1:1 Wild Blueberry Distillate Cartridge (1g) down 22.2% at rank 6 and new Pineapple Crown Distillate Cartridge (1g) arriving at rank 9 with $14,211 in sales. The pattern implies Revel (CO) is consolidating around functional gummy formats while retrenching or reevaluating Vapor Pens that are losing share and rank velocity.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.