Market Insights Snapshot

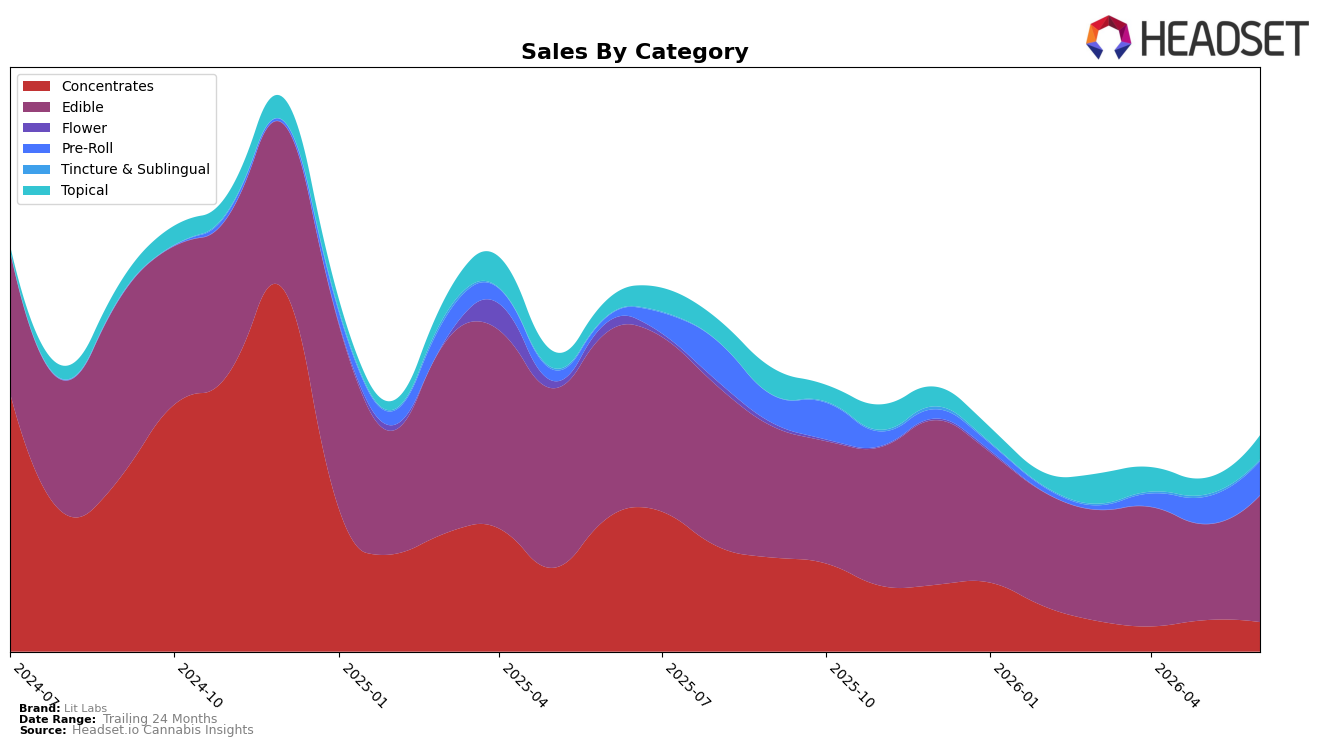

In June 2026, Lit Labs concentrated 58.83% of sales in Edible, where category sales were down 32.16% year over year but up 31.90% month over month, while Pre-Roll rose to a 15.74% share with a 535.11% YoY surge and a 26.78% MoM increase. Concentrates fell to 13.64% share with a 78.15% YoY decline and a 6.07% MoM drop, as Topical reached 11.19% share with 49.93% YoY growth and 45.99% MoM growth. Despite a 179.91% YoY rise, Tincture & Sublingual remained a 0.61% sliver and slipped 29.80% MoM, while the brand’s average price fell 23.19% YoY to $4.46. The mix implies Lit Labs is pivoting away from Concentrates toward Edible and Pre-Roll, using lower prices and faster-growing Topical to offset volume contraction in legacy segments.

With Edible anchoring the portfolio and ranking 57th in Michigan Edible, the 31.90% MoM gain paired with a 32.16% YoY decline suggests a recovery path driven by promotional intensity rather than category expansion, while Pre-Roll’s 535.11% YoY rise and 26.78% MoM lift indicate a bid to capture impulsive, lower-friction occasions. The 78.15% YoY contraction in Concentrates against Topical’s 49.93% YoY and 45.99% MoM growth points to a deliberate rebalancing toward formats with broader baskets, and the 23.19% YoY price reduction signals a value posture intended to regain share in mass segments. Net, the pattern positions Lit Labs as a value-led, convenience-oriented player leaning on Edible and Pre-Roll for reach and on Topical for incremental lift, while deemphasizing high-ASP Concentrates to stabilize rank and share.

Competitive Landscape

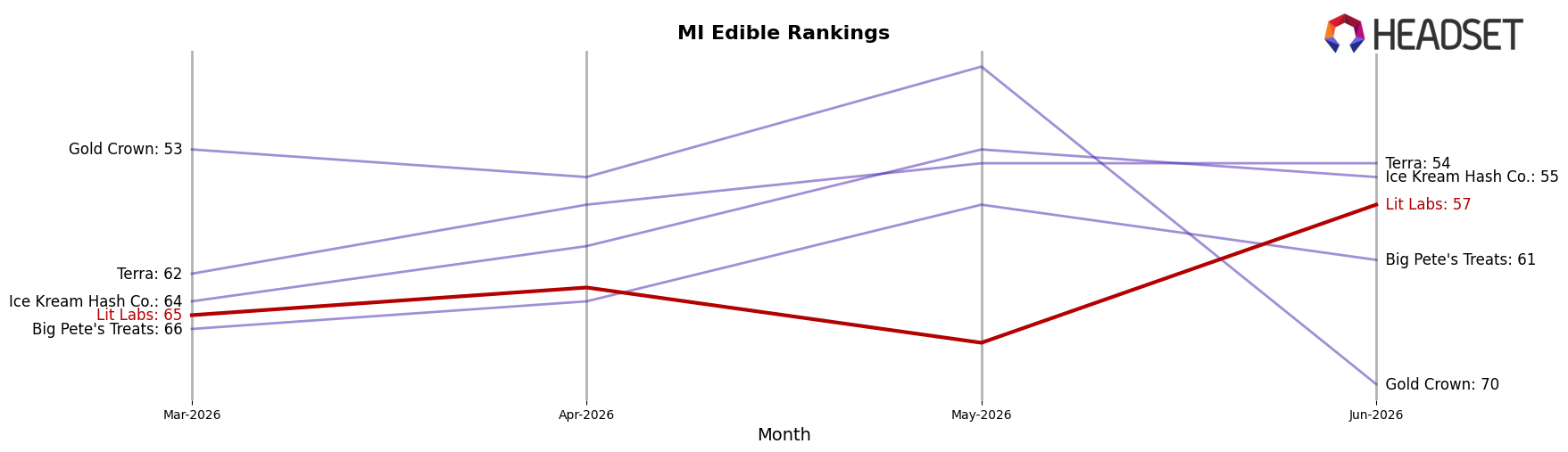

Lit Labs sits at rank #57 in MI Edible for June 2026, down 5 positions from #52 in June 2025, while improving 8 places from #65 in March 2026; against a prior peak of #45 in September 2024, the current placement is 12 ranks lower, and the year-over-year decline in ladder position signals relative share erosion. In contrast, Wyld held #1 year-over-year yet faced a 13.4% sales decline, and MKX Oil Company stayed at #3 with a 10.8% sales increase, indicating that category leadership is stable at the top even as growth mixes shift; this divergence, paired with Lit Labs’ 5-rank YoY drop and 8-rank quarter-on-quarter gain, implies a mid-tier rebound from recent lows but an ongoing struggle to regain September 2024 peak positioning.

Notable Products

Sour Strawberry Pomegranate Rosin + Resin Full Spectrum Vegan Gummies 10-Pack (200mg) posted the standout move in June 2026 with a 160% month-over-month surge to rank 3, while Mango Rosin + Resin Full Spectrum Vegan Gummies 10-Pack (200mg) also cleared the +50% threshold at +52% to rank 4. At the top, Blue Razz Rosin + Resin Full Spectrum Gummies 10-Pack (200mg) rose +26% to hold rank 1, contrasted by Watermelon Rosin + Resin Full Spectrum Vegan Gummies 10-Pack (200mg) falling -41% at rank 7, indicating polarization within similar form factors. With all top-10 SKUs in Edible gummies and the top four slots advancing between +26% and +160%, the mix implies Lit Labs is consolidating around a concentrated gummy portfolio that favors fruit-forward variants with momentum while pruning lagging flavors.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.