Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Local Cannabis Co. is stocked at 141 licensed dispensaries across Missouri, California, and 2 other states, 137 of them in Missouri, with the deepest coverage in St. Louis, KCMO, Columbia, Kansas City, and St Peters. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

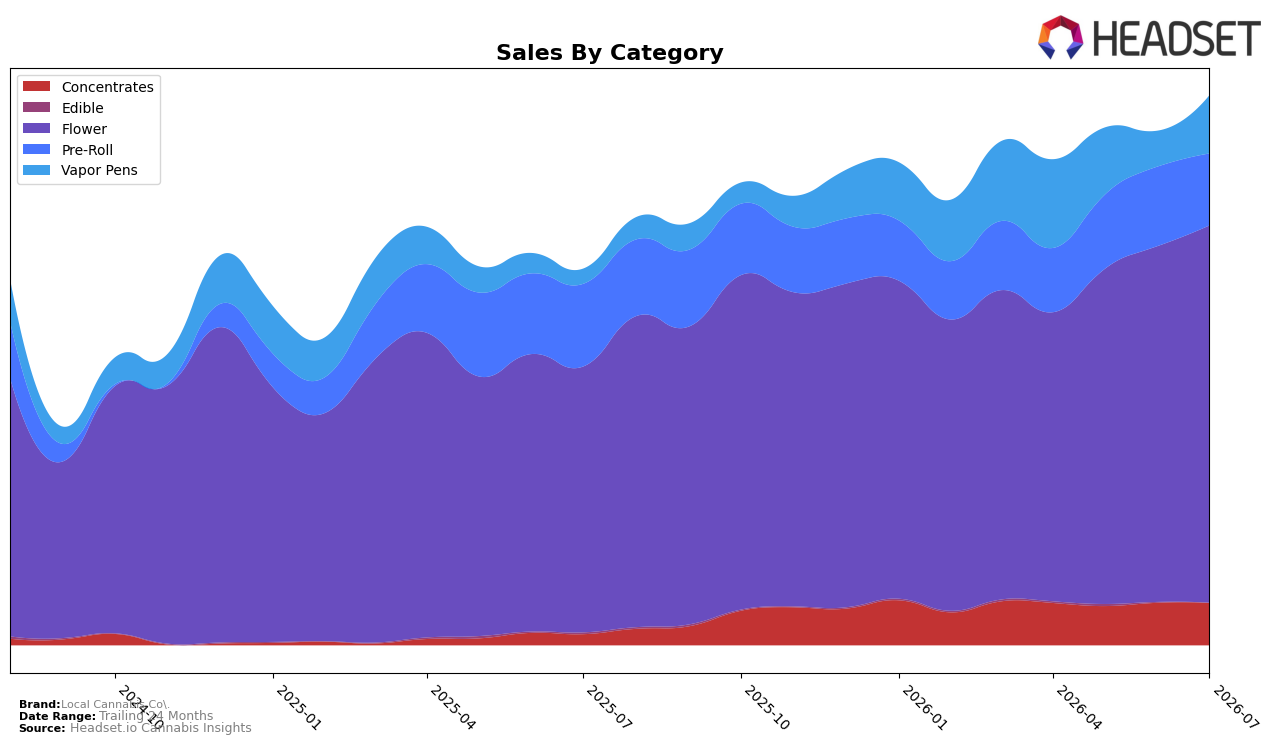

In July 2026, Local Cannabis Co. concentrated 68.45% of sales in Flower, where category revenue rose 41.83% year over year and 5.94% month over month, while Vapor Pens expanded to 10.61% share with a 277.79% year-over-year surge and a 62.25% month-over-month jump. By contrast, Pre-Roll declined to 13.10% share with a -12.87% year-over-year drop and a -9.43% month-over-month slide, and Concentrates held 7.73% share with a 272.83% year-over-year increase but a -0.55% month-over-month dip. Edible contracted to 0.11% share with -70.22% year over year and -42.90% month over month. This mix implies a pivot toward inhalables led by Flower and a rapidly scaling Vapor Pens line, with reallocations away from Pre-Roll and Edible concentrating growth where velocity is accelerating.

Holding rank 5 in Flower in Missouri while Flower share sits at 68.45% indicates reliance on a single engine, but the 277.79% Vapor Pens year-over-year growth and 62.25% month-over-month lift provide a second leg that can rebalance category risk. The -12.87% year-over-year and -9.43% month-over-month contraction in Pre-Roll, alongside a -70.22% Edible decline, suggests deliberate pruning of lower-yield formats as average price rose 16.64% year over year to $32.55. The pattern implies a positioning shift toward premiumized inhalables anchored by Flower leadership and a higher-price Vapor Pens portfolio, improving pricing power while reducing exposure to slower or discounted categories.

Competitive Landscape

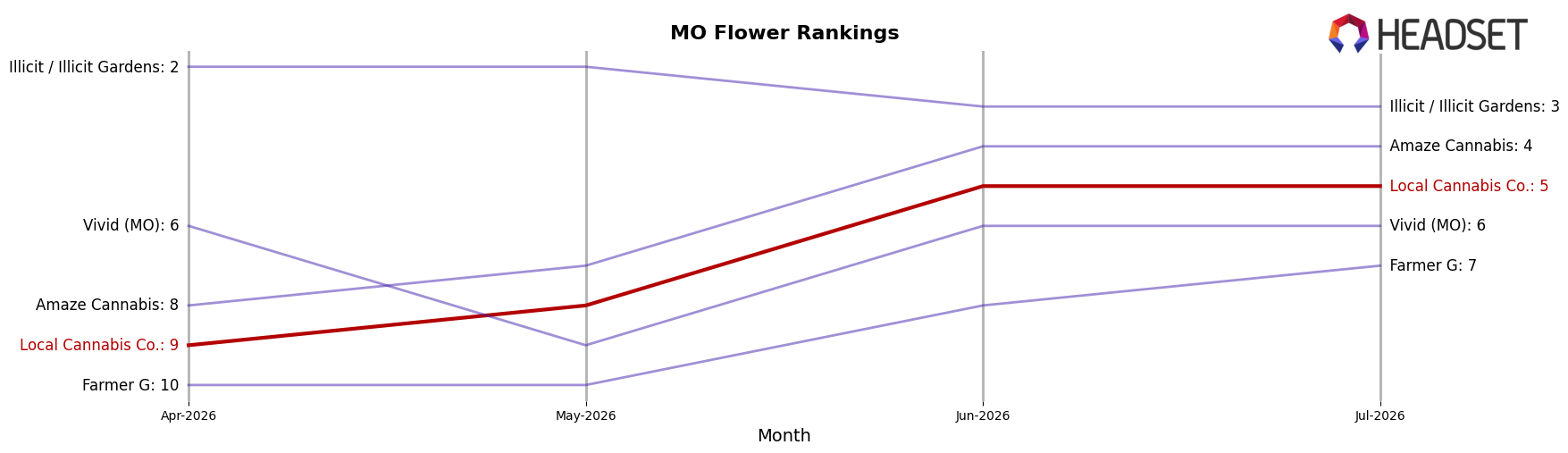

Local Cannabis Co. sits at rank #5 in MO Flower in July 2026 after a year-over-year climb of 5 positions from #10, and it improved 4 spots versus April 2026 when it was #9, signaling momentum toward its peak-to-date of #5 in July 2026; meanwhile, Flora Farms held #1 but posted a -1.3% year-over-year sales change, and Amaze Cannabis advanced to #4 with a 20.6% year-over-year sales increase, placing Local Cannabis Co. within one rank of a faster-rising rival; additionally, Sinse Cannabis moved from #4 to #2 with a 9.0% year-over-year sales gain while Illicit / Illicit Gardens stayed at #3 despite a -12.8% decline, indicating Local Cannabis Co.’s rank trajectory is being pulled upward by share shifts from incumbents but capped by adjacent competitors converting growth into higher ranks.

Notable Products

Orange 43 (3.5g) posted the steepest movement in July 2026 with a -58.3% month-over-month drop while holding rank 1, a divergence that implies price or inventory tactics sustained placement despite sharply lower throughput. WiFi #3 (3.5g) climbed 38.0% MoM to rank 4 and Pacific Cooler (3.5g) gained 28.9% MoM to rank 9, while WiFi #3 Pre-Roll (1g) in rank 2 grew a modest 3.2% MoM, and seven of the top ten are Flower SKUs, signaling category concentration over format diversification. With Flower occupying ranks 1, 3, 4, 5, 6, 7, 9, and 10 and only two Pre-Rolls in the top ten, the mix indicates Local Cannabis Co. is leaning into strain-led Flower velocity rather than expanding pre-roll share. The pattern implies a deliberate focus on Flower-led basket building, even at the cost of volatility in flagship items, as evidenced by the single-month revenue of $101,950 tied to Orange 43 (3.5g) amid its contraction.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.