Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

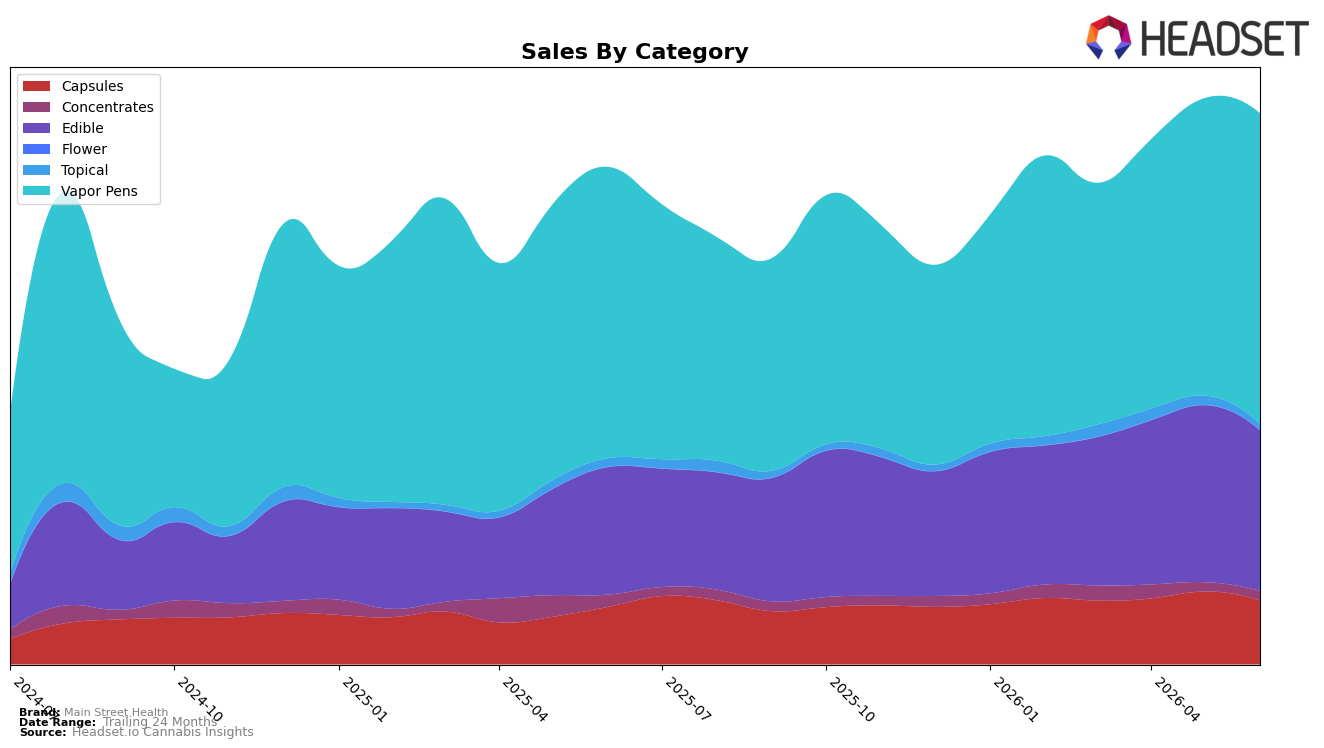

In June 2026, Main Street Health concentrated 56.46% of sales in Vapor Pens, where category sales rose 6.60% year over year and 4.34% month over month, while the brand’s average price fell 7.55% YoY, indicating volume-led gains. Edible expanded to 29.16% share with a 25.96% YoY lift but declined 9.29% MoM, and Capsules held 11.60% share with 11.14% YoY growth but a 12.24% MoM drop; meanwhile, Concentrates at 1.70% share fell 21.97% YoY but edged up 3.02% MoM, and Topical at 1.08% share contracted 28.41% YoY and 33.95% MoM. With Vapor Pens ranked 13th in Ohio and accounting for over half of mix, the pattern implies the brand is leaning on a price-reduced, higher-volume pen portfolio to offset MoM pullbacks in Edible and Capsules.

The divergence between Edible’s 25.96% YoY growth and 9.29% MoM decline, alongside Capsules’ 11.14% YoY increase and 12.24% MoM dip, implies that recent shopper missions are shifting back toward quicker-replenish Vapor Pens as prices ease, while slower-turn wellness formats temporarily cool. With Concentrates posting a 21.97% YoY decline but a 3.02% MoM uptick and Topical sliding 33.95% MoM, the mix suggests Main Street Health is prioritizing accessible inhalables over niche, premium-priced segments; combined with a 13th-place Vapor Pens rank, the implication is a mid-pack positioning that can gain share by sustaining sub-$21 average pricing in pens while selectively stabilizing Edible and Capsules to prevent further MoM share erosion.

Competitive Landscape

Main Street Health ranks #13 in OH Vapor Pens in June 2026, down 2 positions year over year from #11 while up 1 place versus March 2026’s #14, indicating lateral movement rather than recovery toward its peak of #10 last reached in March 2025. Against this, Rove rose from #10 year over year to #5 with 98.5% YoY sales growth, and Select moved from #5 to #4 with 24.1% YoY sales growth, tightening the top-5 and widening the gap from #13; meanwhile, Certified (Certified Cultivators) held #1 YoY and current, and Klutch Cannabis held #2 YoY and current, reinforcing a stable lead tier. The combination of a 2-position YoY slippage and only a 1-position quarter-on-quarter uptick implies Main Street Health risks being locked in the mid-teens unless it captures share from ascending mid-pack rivals that are converting growth into rank gains.

Notable Products

Nanoemulsified RSO Capsules 30-Pack (750mg) posted the steepest move in June 2026 with a -16.3% month-over-month decline and slid to rank 8, while Cinnamon Gummies 11-Pack (550mg) fell -21.7% at rank 9, pointing to pressure outside Vapor Pens. In contrast, Artifact - Blueberry Distillate Cartridge (1g) rose +24.7% to hold rank 1 with $103,207 in sales, and Artifact - Maui Wowie Distillate Cartridge (1g) dropped -11.8% at rank 3, indicating volatility within the same pen lineup. With seven of the top ten drawn from Vapor Pens and Artifact - Trainwreck Distillate Cartridge (1g) down -10.7% at rank 4 while Artifact - Panama Red Distillate Cartridge (1g) gained +19.8% at rank 6, the category shows mix rotation rather than category exit. The pattern implies Main Street Health is leaning further into Vapor Pens while edibles and capsules contract, consolidating focus around a few winning SKUs and pruning weaker non-inhalable formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.