Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Neighborgoods is stocked at 72 licensed dispensaries across Ohio, with the deepest coverage in Cincinnati, Columbus, Cleveland, Toledo, and Lakewood. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

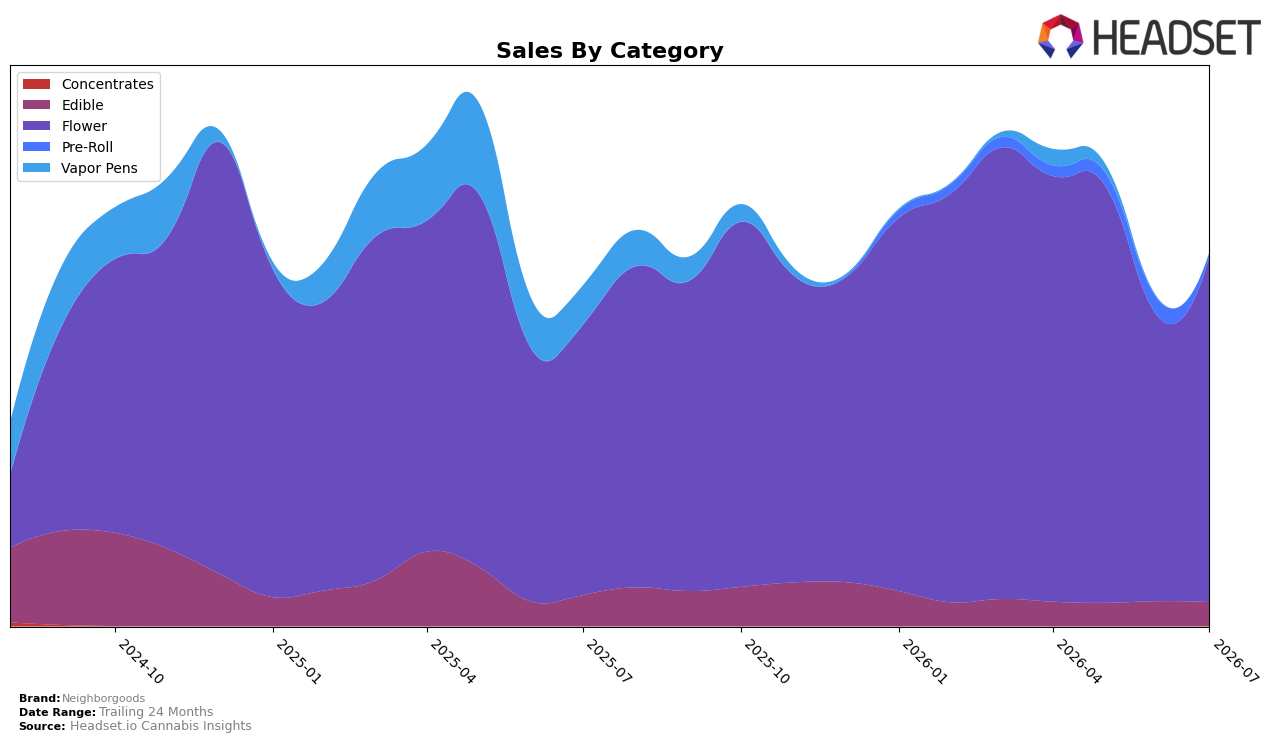

Neighborgoods concentrated 92.65% of July 2026 sales in Flower with year-over-year growth of 27.94% and month-over-month growth of 21.50%, while Edible held 6.32% share with a -23.14% YoY decline and -3.70% MoM dip; Pre-Roll slid to 1.03% share with a -77.02% MoM contraction and no YoY baseline. The brand’s average price rose 44.19% YoY to $44.93 as Flower’s average price sat higher at $51.21, indicating mix-up and price-up effects coexisting; combined with total brand sales up 9.85% YoY and a 24‑month expansion of 494.06%, the skew toward higher-priced Flower is driving topline while shrinking Edible and collapsing Pre-Roll curb diversification.

With Flower ranked 6 in Ohio and holding 92.65% share, the 21.50% MoM and 27.94% YoY gains suggest deeper reliance on a single category even as Edible’s -23.14% YoY and Pre-Roll’s -77.02% MoM drops thin out entry points. The pattern implies Neighborgoods is consolidating around premium-priced Flower to defend a mid‑single‑digit rank while forgoing volume capture from lower-priced formats, so sustaining rank 6 will likely depend on maintaining the Flower price ladder and selectively stabilizing Edible to prevent further share concentration risk.

Competitive Landscape

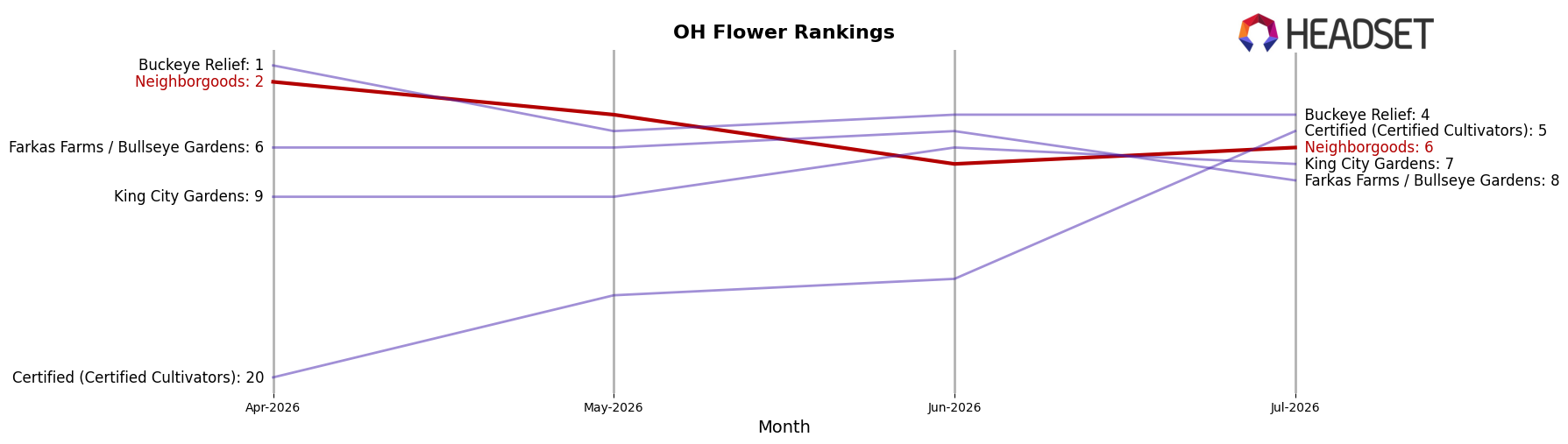

Neighborgoods is currently ranked #6 in OH Flower, improving 3 positions year over year from #9, but slipping 4 spots since April 2026’s #2 and falling from a peak of #1 in March 2026; meanwhile, RYTHM moved from #6 to #1 with 74.99% YoY sales growth, and Klutch Cannabis climbed from #21 to #3 on 403.04% YoY growth, indicating that Neighborgoods’ mid-year drop of 4 ranks alongside competitors’ upward mobility compresses share at the top and implies a shift from early-year leadership to a chase position unless rank recapture occurs.

Notable Products

Mixed Sativa Pre-Roll (1g) posted the steepest movement in July 2026 with a -22.0% month-over-month decline and held rank 6, while Cherry Lime Sunshine Liquid Live Resin Gummies 10-Pack (200mg) was effectively flat at -0.4% and sat at rank 8. Within Flower, Black Amber (14.15g) slipped -4.8% at rank 9, and five of the top ten SKUs are Flower products, indicating revenue concentration in bulk flower formats. The Soap (14.15g) and RS11 (14.15g) placements at ranks 1 and 2, combined with Cap J (14.15g) at rank 5, point to large-pack Flower anchoring the leaderboard despite weakness in Pre-Roll, with one Flower SKU delivering $182,613 in July 2026. The pattern implies Neighborgoods is leaning into high-volume Flower while trimming exposure to slower-turn Pre-Rolls to stabilize rank positions and protect share.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.