Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Matter. is stocked at 176 licensed dispensaries across New York, Pennsylvania, and 5 other states, 109 of them in New York, with the deepest coverage in New York, Buffalo, Queens, Depew, and East Syracuse. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

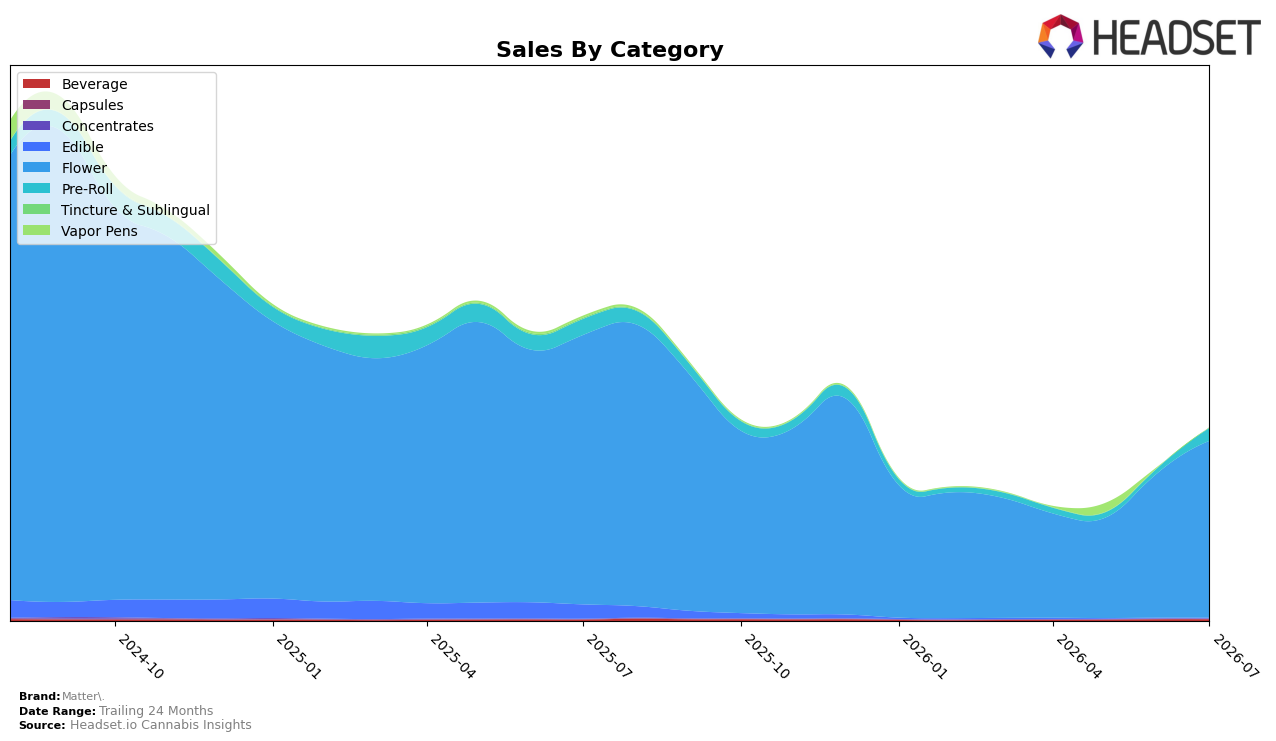

Matter. concentrated 92.53% of July 2026 sales in Flower, where year-over-year sales fell 34.43% even as month-over-month sales rose 21.99%, while Pre-Roll held 6.50% share with a 20.65% year-over-year decline but a 166.91% month-over-month surge. Beverage accounted for 0.89% share with a 28.50% year-over-year increase and a 0.51% month-over-month dip, and Edible sat at 0.09% share after a 98.82% year-over-year drop but a 13.21% month-over-month uptick; combined with an 18.04% year-over-year decline in average price and a 36.91% brand-level sales contraction, this pattern implies a volume-leaning rebound concentrated in Flower while small-format trial emerges in Pre-Roll.

With Flower anchored at rank 20 in Ohio and holding 92.53% mix, the 21.99% month-over-month lift alongside a double-digit price compression of 18.04% year-over-year suggests share defense via accessible pricing rather than premium trade-up, while the 166.91% month-over-month spike in Pre-Roll at only 6.50% share signals an on-ramp format that can diversify basket entry without displacing Flower. Beverage’s 28.50% year-over-year growth at sub-1% share and Edible’s 98.82% year-over-year contraction indicate peripheral categories are not yet meaningful demand pillars; taken together, the positioning implication is a Flower-first brand stabilizing via price elasticity, with Pre-Roll expansion as the practical path to broaden reach without diluting the core.

Competitive Landscape

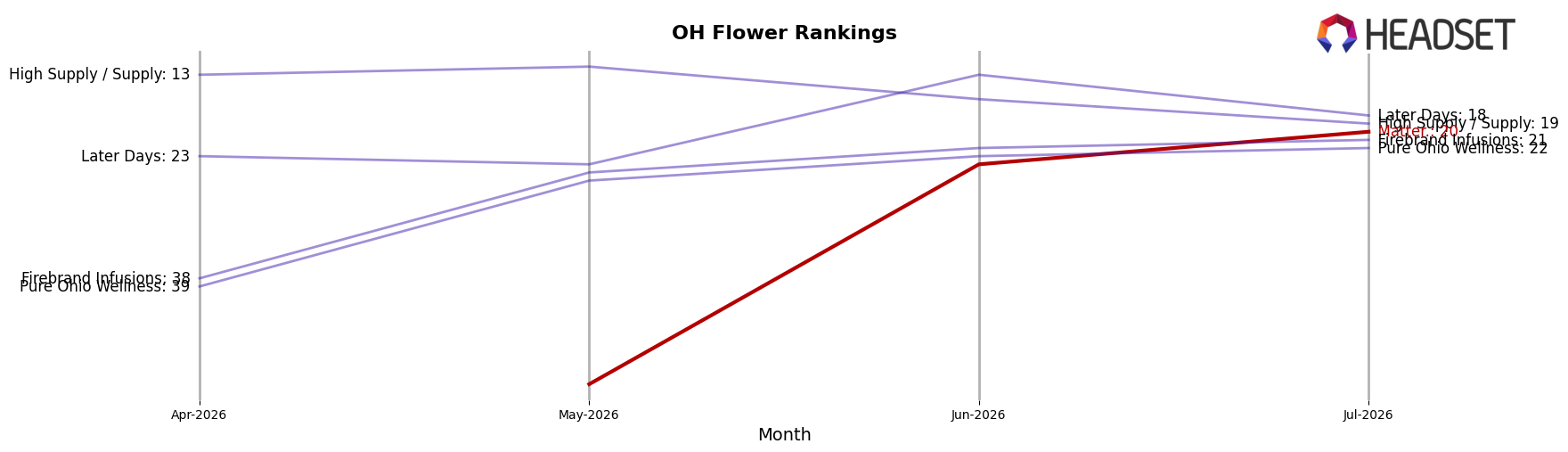

Matter. sits at rank #20 in OH Flower in July 2026, with no recorded year-over-year rank change available, while peers at the top moved sharply: RYTHM climbed to #1 with a 6-position YoY rise and 74.99% sales growth, and Klutch Cannabis advanced to #3 with a 21-position YoY jump and 403.04% growth; in contrast, Riviera Creek held #2 despite a 15.97% YoY decline, and Buckeye Relief is #4 with a 2-position YoY gain but a 10.49% sales decline. With Matter. at its peak rank of #20 in July 2026 and competitors moving multiple ranks year-over-year, the pattern implies Matter.’s current positioning is static relative to a reshuffling top tier, requiring either share capture or mix shifts to avoid further dilution in rank.

Notable Products

Slurricane (14g) delivered the standout movement with a 191.6% month-over-month surge to $199,796 and jumped to rank 2, while Bananaconda (14.15g) also spiked 156.7% to rank 4, contrasting with Lemon Strawberry (14.15g) slipping 7.7% at rank 9; five of the top ten are 14g-plus Flower SKUs, concentrating momentum in larger pack sizes. Super Boop (2.83g) rose 42.0% at rank 1 as Intergalactic (14.15g) was nearly flat at +1.8% at rank 3, and Intergalactic (2.83g) advanced 15.9% at rank 6, indicating that while smaller formats contribute, outsized gains are being captured by 14g lines. The pattern implies Matter. is tilting toward value-driven bulk flower where triple-digit gains and top-5 ranks cluster, signaling a strategy that prioritizes basket-size expansion over breadth of smaller SKUs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.