Where to Buy

The Plug Pack is stocked at 84 licensed dispensaries across New York, with the deepest coverage in New York, Syracuse, Queens, Binghamton, and Buffalo. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

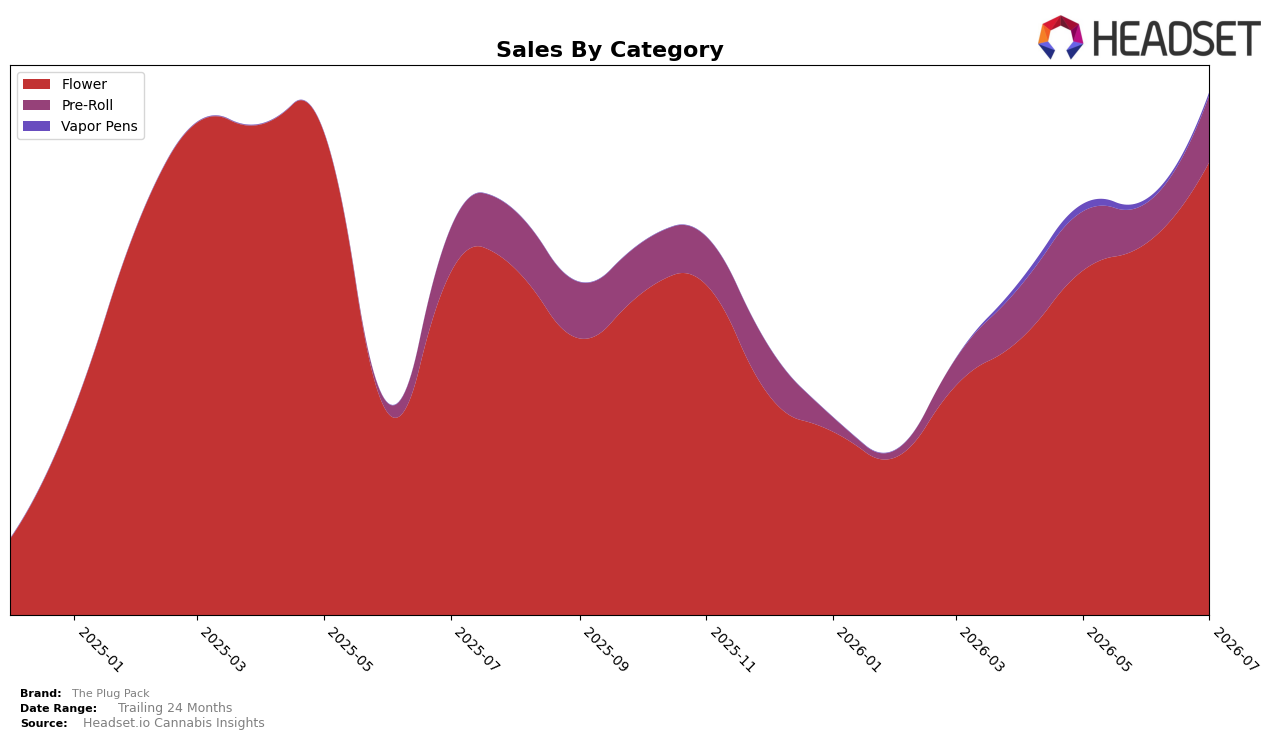

The Plug Pack concentrated 86.69% of July 2026 sales in Flower with year-over-year growth of 32.30% and month-over-month acceleration of 21.73%, while Pre-Roll held 12.73% share with sharper year-over-year expansion of 51.47% and a month-over-month jump of 67.38%. Vapor Pens were a marginal 0.58% share with a 16.97% month-over-month decline and no year-over-year baseline, coinciding with a 39.78% year-over-year drop in average price to $59.51. The pattern implies a deliberate tilt toward value-accessible inhalable formats where Pre-Roll’s faster 51.47% year-over-year and 67.38% month-over-month gains act as the incremental growth engine, while Flower remains the volume anchor despite price compression.

Within New York Flower, a rank of 8 signals mid-pack visibility that benefits from the 21.73% month-over-month lift in Flower and the 67.38% month-over-month surge in Pre-Roll as a feeder, yet the 39.78% average price decline introduces trade-down pressure that could cap rank mobility without further mix shift. The juxtaposition of 32.30% year-over-year growth in Flower against 51.47% in Pre-Roll suggests positioning that leans into convenience-driven occasions, with the 0.58% Vapor Pens share and its 16.97% month-over-month drop indicating limited traction in oil-based formats relative to combustion-led demand; the implication is a near-term focus on scaling Pre-Roll to convert incremental trips while protecting Flower’s rank through price-pack architecture.

Competitive Landscape

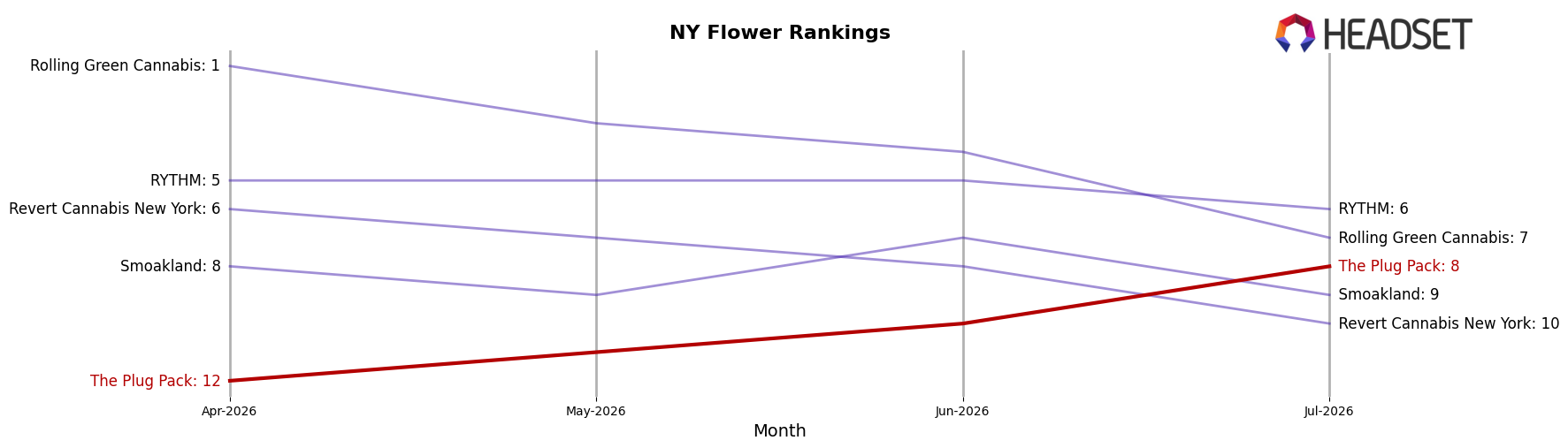

The Plug Pack sits at rank #8 in NY Flower in July 2026, improving 3 positions from #11 year over year and 4 positions from #12 over the last three months; against the broader ladder, Find. advanced from #8 to #1 while Dank. By Definition holds #3 despite a -51.5% sales change, indicating that The Plug Pack’s upward movement comes amid both rapid ascents and retreats at the top. With a historical peak of #2 in March 2025 and current placement outside the top five while Grassroots jumped to #5 from #15 alongside a 79.8% YoY sales increase, the pattern implies The Plug Pack is regaining rank but must accelerate share capture to convert mid-table momentum into sustained top-tier presence.

Notable Products

Tequila Sunrise (28g) holds rank 1 with 251,731 dollars while Bomb Pop (28g) climbs to rank 2 on a 37.5% month-over-month increase, and Cherry Pie (28g) slips at rank 10 with a -3.4% decline; the lack of any >50% surges or >10% drops places the month in a consolidation phase where rank stability matters more than velocity. Lychee Dream (28g) sits at rank 9 with +5.5% MoM and the Tequila Sunrise Pre-Roll (1g) moves up with +16.3% MoM at rank 8, but Pre-Rolls overall (ranks 4, 6, 7, 8) concentrate four of the top ten even as Flower controls the top three ranks; this split implies The Plug Pack is anchoring demand with large-format Flower while seeding repeat purchase through lighter-ticket Pre-Rolls. The product mix points to a strategy that prioritizes flagship Flower SKUs for share capture while using incremental Pre-Roll gains to broaden basket penetration and stabilize monthly revenue.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.