Where to Buy

Rolling Green Cannabis is stocked at 276 licensed dispensaries across New York, with the deepest coverage in New York, Buffalo, Rochester, Queens, and Syracuse. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

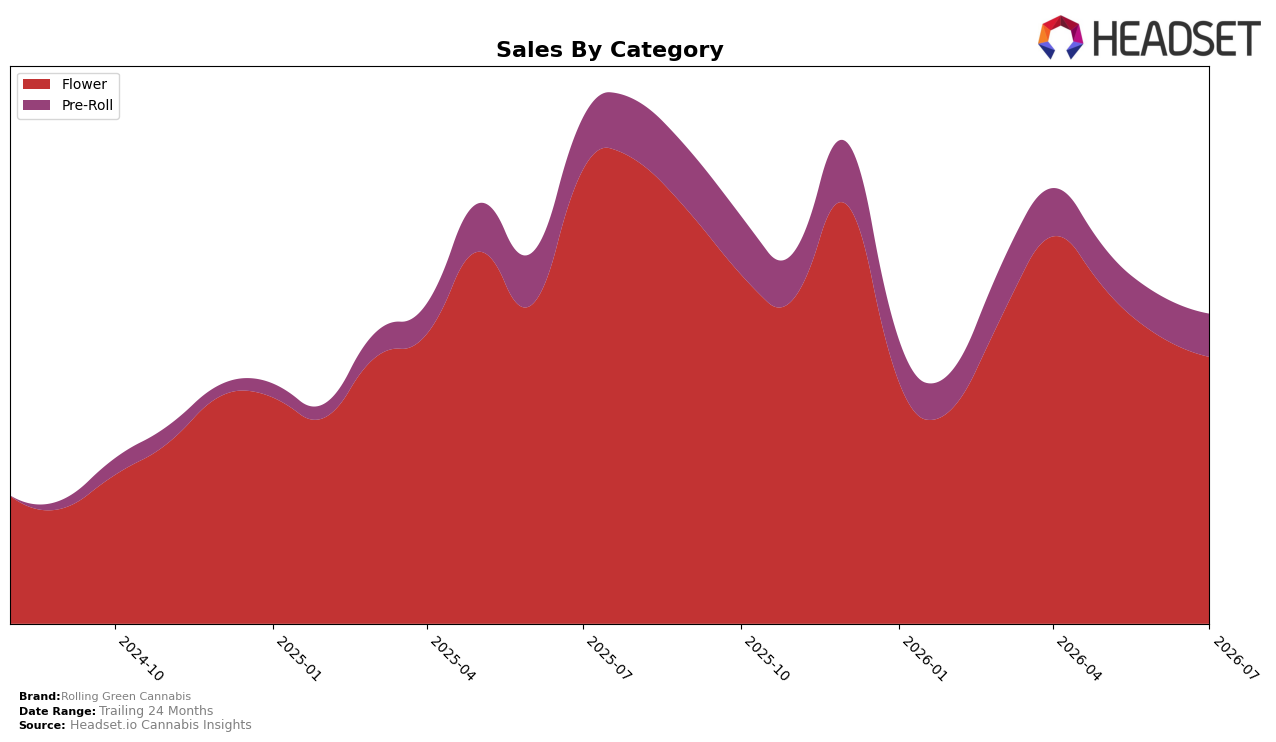

Rolling Green Cannabis concentrated 81.08% of July 2026 sales in Flower while 18.92% came from Pre-Roll, with Flower down 39.15% year over year and 6.92% month over month, contrasted by Pre-Roll down 11.57% year over year but up 3.19% month over month; this mix shift sits alongside a 35.33% brand sales decline year over year and a 6.61% drop in average price. In New York Flower specifically, the brand held rank 7, indicating mid‑tier placement even as the category’s weight exposes the brand to outsized volatility; together, these numbers imply over-reliance on a contracting Flower base while Pre-Roll provides a modest counterweight.

The divergence—Flower shrinking faster (-39.15% YoY) than the overall brand (-35.33% YoY) while Pre-Roll softens less (-11.57% YoY) and grows month over month (+3.19%)—implies that incremental share reallocation toward Pre-Roll could reduce revenue variance and price pressure. With average price down 6.61% and Flower average price at 56.82 versus Pre-Roll at 13.35, maintaining rank 7 in New York Flower will likely require selective price discipline and sku pruning, while leaning into Pre-Roll momentum to stabilize July-to-August mix and protect unit velocity.

Competitive Landscape

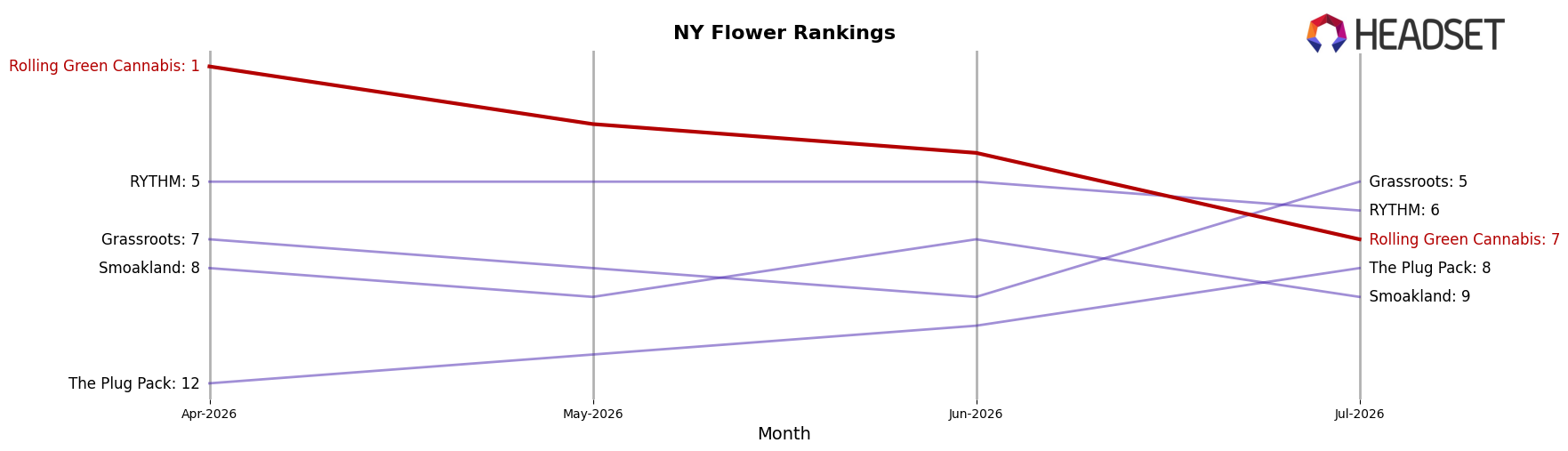

Rolling Green Cannabis sits at rank #7 in NY Flower in July 2026, down 5 places from its #2 position year over year and 6 places from its #1 spot in April 2026; this drop contrasts with Find. holding #1 while improving 7 positions YoY and growing sales 46.7%, and Grassroots advancing to #5 with a 15-place YoY climb and 79.8% sales growth. Compared with Leal at #2 after a 5-rank YoY rise and 34.4% sales growth, Rolling Green Cannabis’s slide from peak implies share is concentrating toward faster-rising leaders, signaling that recent momentum loss since April 2026 risks persistent mid-tier positioning unless rank recovery reverses the 6-spot three-month decline.

Notable Products

Oreoz (3.5g) posted the steepest move in July 2026 with a -21.7% month-over-month decline while slipping to rank 7, contrasting with Green Crack Pre-Roll (1g) rising 52.4% MoM to rank 3. Blue Dream Pre-Roll (1g) led at rank 1 with a 1.3% MoM uptick and Super Lemon Haze Pre-Roll (1g) at rank 2 grew 18.3% MoM, and five of the top ten were Pre-Roll SKUs, indicating the lineup is tilting toward fast-turn inhalables. The top five ranks were entirely Pre-Rolls with Tangerine Dream Pre-Roll (1g) up 23.0% MoM to rank 5, while Trainwreck Pre-Roll (1g) edged down -1.6% MoM at rank 4, a spread that implies pre-roll velocity is concentrating in fruit-forward and classic sativa strains. This mix points to Rolling Green Cannabis shifting merchandising and inventory toward Pre-Roll dominance while allowing select Flower items to play a secondary, price-sensitive role around the $60,696–$82,452 range, implying a strategy anchored in high-frequency, top-ranked SKUs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.