Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

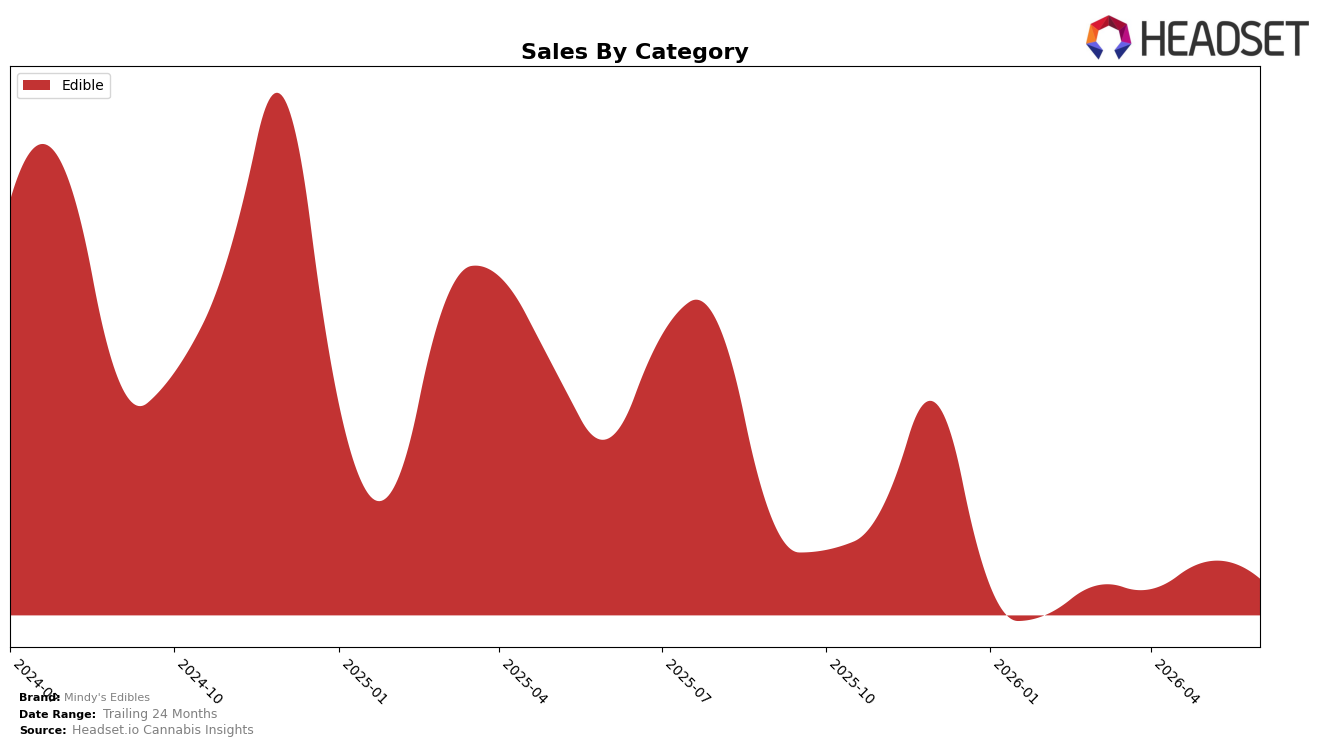

In June 2026, Mindy's Edibles operated as a single-category brand, with Edible accounting for 100.0% of sales and averaging $15.45 per unit, while year-over-year sales declined 12.7% and month-over-month sales slipped 1.7%. Within Illinois Edible, the brand held rank 16, pairing a 10.7% YoY price decline with a 12.7% YoY sales decline, which signals volume elasticity below one; the small 1.7% MoM sales dip alongside a flat category mix suggests no offset from other formats. The implication is that a pure-play Edible stance left no buffer against Edible-specific demand softness, so maintaining rank 16 amid a double-digit YoY contraction points to share defense coming from distribution or retention rather than price-led volume wins.

The category concentration and the 10.7% YoY price reduction, combined with a 12.7% YoY sales drop and a rank of 16 in Illinois, imply the brand is competing on accessibility rather than premiumization, with pricing traction not converting to proportional volume gains. The 1.7% MoM decline, alongside an unchanged 100.0% category mix and a two-year sales contraction of 27.7%, indicates a structural positioning risk: dependence on Edibles caps upside during category slowdowns and limits cross-category trade-up or retention levers. Net effect: to move up from rank 16 while price is down 10.7% YoY yet sales still fall 12.7% YoY, the brand must pivot positioning toward differentiated value or format expansion rather than additional price concessions.

Competitive Landscape

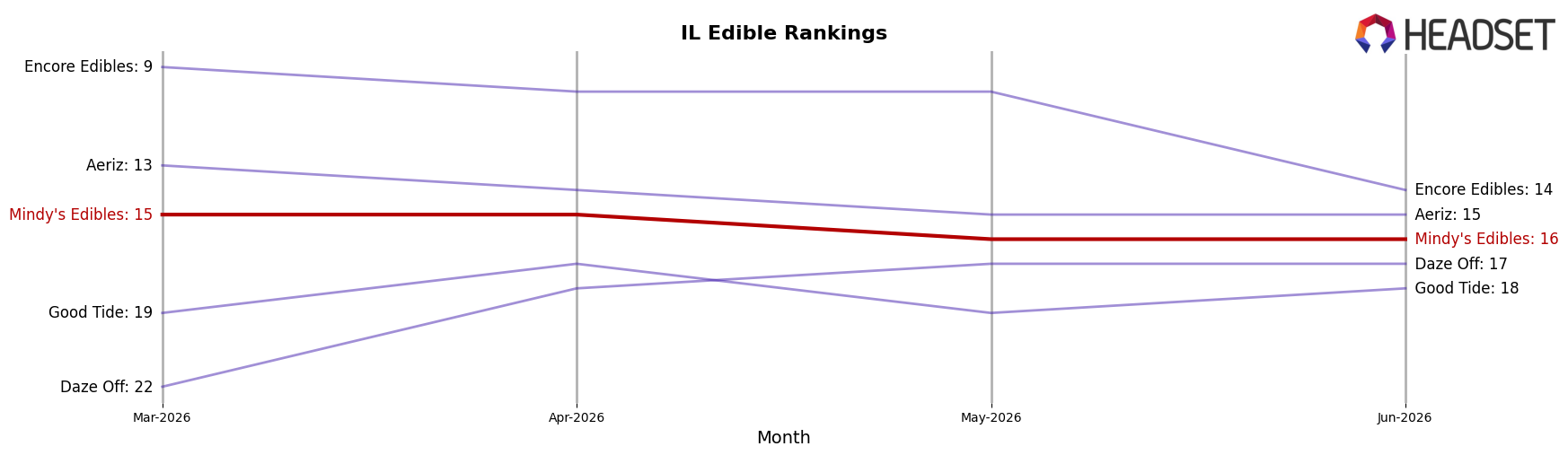

Mindy's Edibles sits at rank #16 in IL Edible for June 2026 after sliding 3 positions from #13 year over year, and it also fell 1 spot from #15 in March 2026 while remaining 6 ranks below its peak of #10 in December 2024; meanwhile, Incredibles held at #1 after moving up from #2 year over year even with a 1.9% sales decline, and Wyld slipped from #1 to #2 alongside a 17.5% sales drop, indicating that Mindy's Edibles is losing relative position in a reshuffling top tier where incumbents trade places despite mixed growth signals.

Notable Products

Botanical White Grapefruit Gummies 20-Pack (100mg) fell 20.9% month over month to rank 8, while Freshly Picked Berries Gummies 20-Pack (50mg) dropped 12.6% at rank 4, indicating softness at the lower-dose and botanical edge of the lineup. At the top, CBD/THC 1:1 Lush Black Cherry Gummies 20-Pack (100mg CBD, 100mg THC) stayed at rank 1 despite a 5.0% decline, and Glazed Clementine Orange Gummies 20-Pack (100mg) climbed 19.8% at rank 2, with four of the top ten being Gummies that anchor the brand’s share of shelf. Cool Keylime Kiwi Gummies 20-Pack (100mg) was nearly flat at +0.5% in rank 5 as chocolates were static near ranks 9–10 with about $5.9K, signaling that Gummies remain the volume engine even as certain flavors cycle down. The mix suggests Mindy's Edibles is consolidating around core 100mg Gummies with selective flavor winners, while trimming exposure to niche botanical profiles.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.