Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Aeriz is stocked at 267 licensed dispensaries across Illinois, Arizona, and California, 213 of them in Illinois, with the deepest coverage in Chicago, Springfield, East Peoria, Naperville, and Normal. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

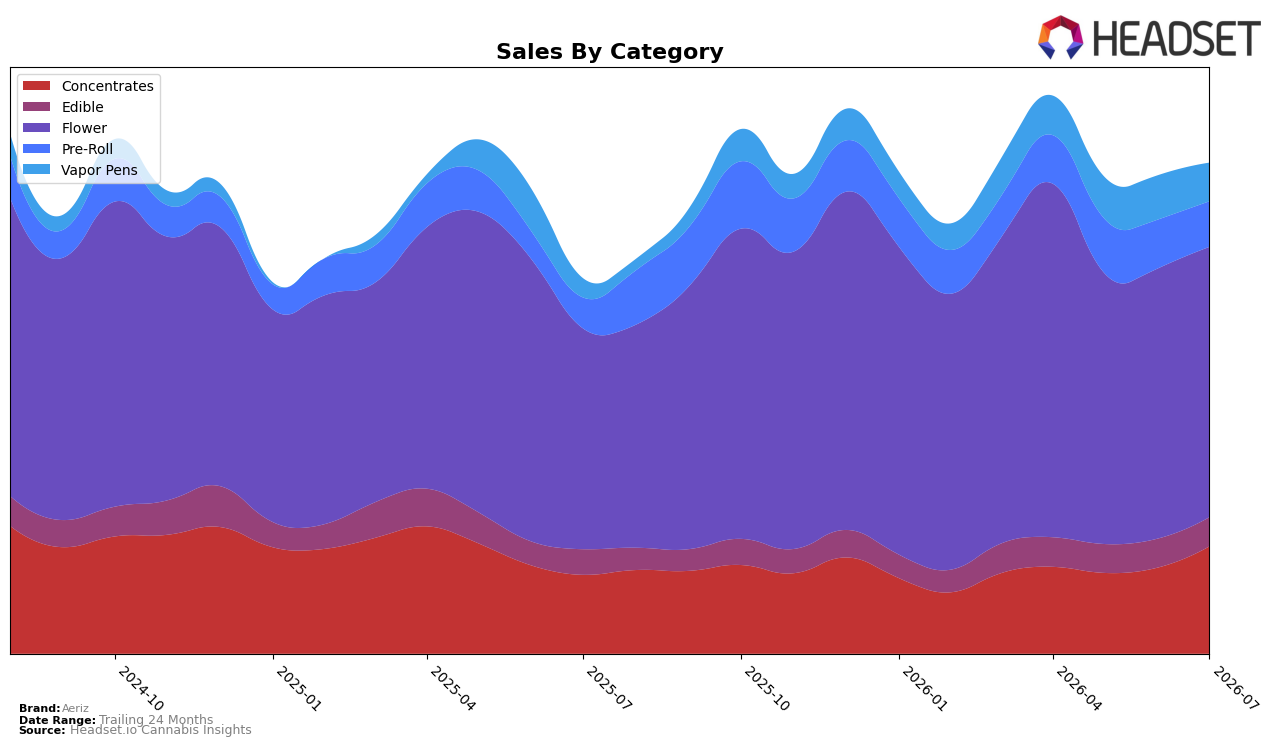

Aeriz’s mix in July 2026 concentrates around Flower at 49.56% share with 20.76% YoY growth and a 0.05% MoM uptick, while Concentrates expanded to 21.58% share with 29.33% YoY and 20.30% MoM growth. Pre-Roll holds 10.96% share with 29.75% YoY growth but a -4.80% MoM dip, and Vapor Pens at 9.77% share posted 51.76% YoY alongside a -9.14% MoM decline; Edible sits at 8.13% share with 8.08% YoY and 0.35% MoM growth. With overall brand sales up 24.79% YoY and average price up 1.50%, the pattern implies Aeriz is leaning into higher-velocity inhalables where YoY momentum (51.76% in Vapor Pens and 29.33% in Concentrates) offsets near-term MoM softness, concentrating revenue in Flower while widening the platform in Concentrates.

Holding rank 7 in Flower in Illinois alongside a 49.56% mix share indicates reliance on a mature anchor, but the 20.30% MoM surge in Concentrates and 51.76% YoY in Vapor Pens shift the center of gravity toward segments with faster gains. The modest 0.05% MoM in Flower and -9.14% MoM in Vapor Pens suggest near-term volatility that can be buffered by Concentrates’ momentum and steady Edible growth of 0.35% MoM, implying positioning as a Flower-led brand that is actively reallocating toward dabbable and cart formats to capture incremental share without overexposing to a single category.

Competitive Landscape

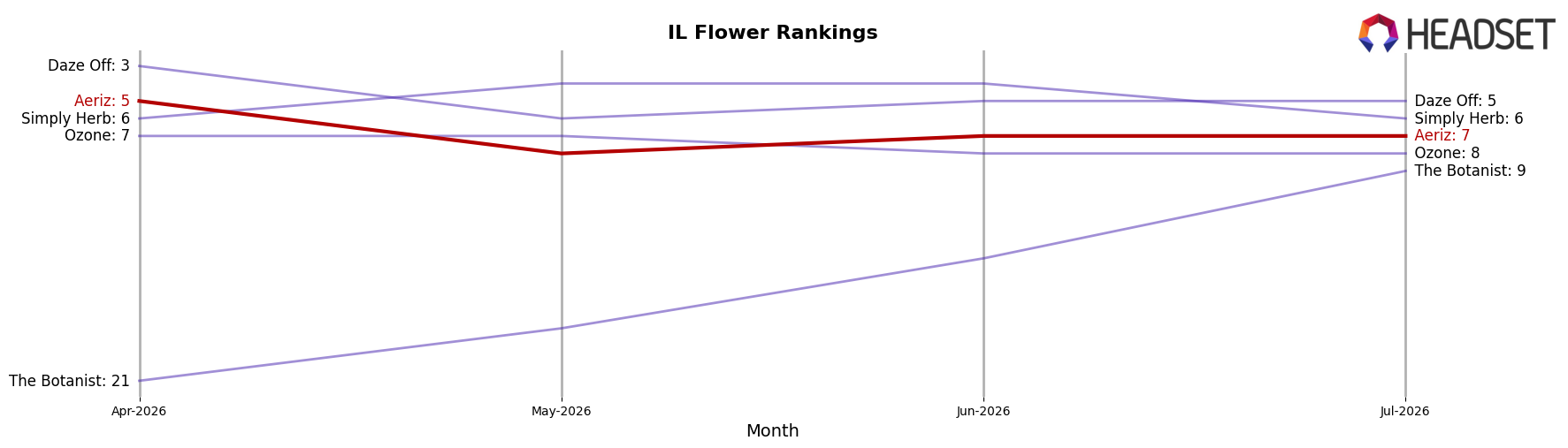

Aeriz sits at rank #7 in July 2026, a 4-place improvement from #11 year over year, but down 2 places from its three-month position of #5 in April 2026, when it also hit a peak rank of #5; meanwhile, High Supply / Supply held #1 year over year and in July 2026 despite a -3.0% YoY sales change, and &Shine moved up from #8 to #4 on an 87.4% YoY sales increase, indicating competitors are gaining rank faster even as Aeriz improves. The combination of a 4-rank YoY climb alongside a 2-rank slip since April 2026 implies Aeriz’s trajectory is upward over the year but losing momentum quarter-to-quarter as faster-rising peers compress the middle tier.

Notable Products

Jenny Kush Pre-Roll 2-Pack (1g) posted the standout move in July 2026 with a 65.3% month-over-month gain, climbing to rank 2, while G-Tank Pre-Roll 2-Pack (1g) slid 12.0% to rank 4. Jenny Kush (3.5g) remained the top seller at rank 1 despite a 5.3% decline, and three of the top ten are Pre-Roll SKUs, signaling a tilt toward ready-to-consume formats over bulk Flower. GMO Full Spectrum Hash Oil (1g) advanced 45.9% to rank 7 as two other Full Spectrum Hash Oil SKUs held ranks 5 and 6, concentrating share in concentrates alongside Pre-Rolls. The mix implies Aeriz is reallocating demand toward convenience and potency-led formats, positioning Pre-Rolls and FSHO as growth anchors while flagship Flower steadies the base.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.