Where to Buy

Missouri's Own Edibles is stocked at 59 licensed dispensaries across Missouri, with the deepest coverage in KCMO, St. Louis, Independence, Joplin, and Branson. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

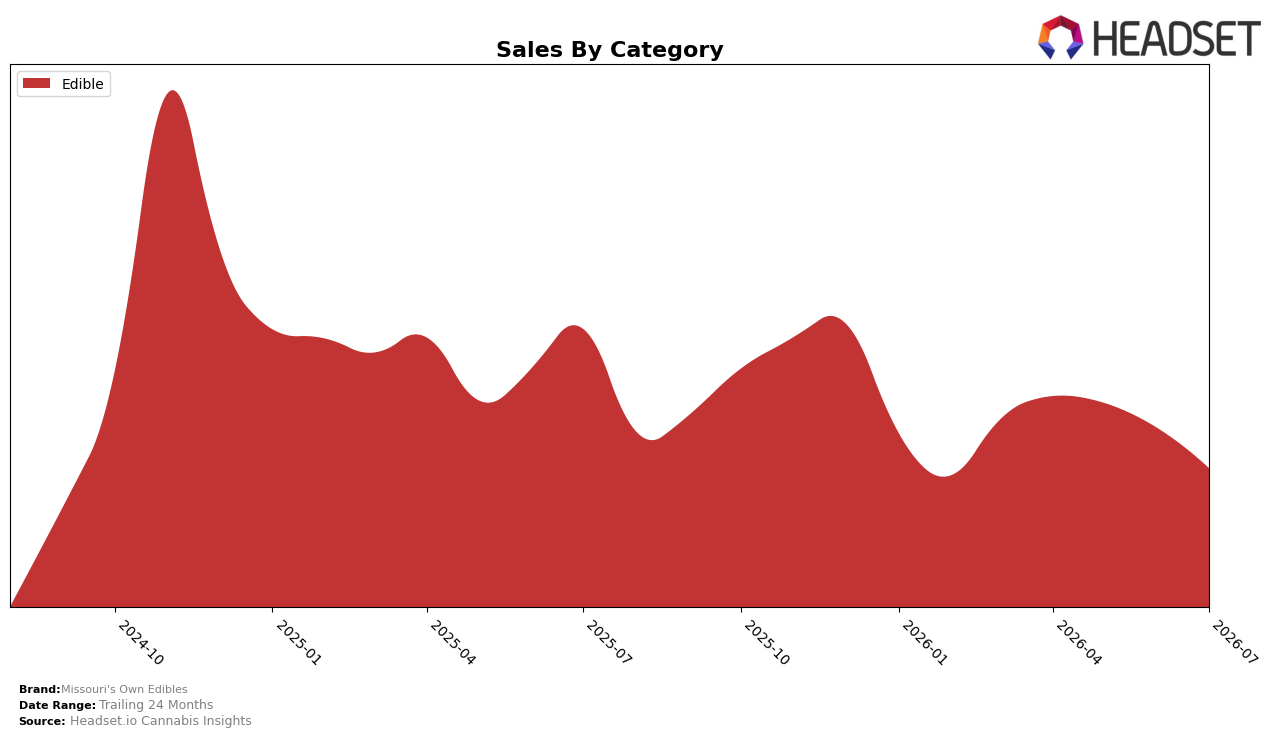

Missouri's Own Edibles operated as a single-category brand in Missouri Edible in July 2026, with Edible holding 100.0% category mix and posting a -21.5% year-over-year sales change alongside a -7.3% month-over-month decline. Within that concentration, average price was $16.60 with a -4.3% YoY price contraction, while sales rank in Missouri Edible sat at position 18, anchoring the brand squarely in the mid-pack and implying that the all-in Edible focus is compressing both volume and rank momentum.

The combination of a -21.5% YoY sales drop and a -7.3% MoM slide, alongside a -4.3% YoY price reduction, suggests price-led defense is not offsetting demand softness, which keeps the brand at rank 18 in Missouri Edible rather than climbing toward higher tiers. With 100.0% exposure to Edible and a 24-month sales change of -37.9%, the current mix constrains upside optionality, implying that without mix diversification or a sharper price-pack-size strategy, the brand’s positioning will likely remain mid-tier rather than advancing in rank or recapturing share.

Competitive Landscape

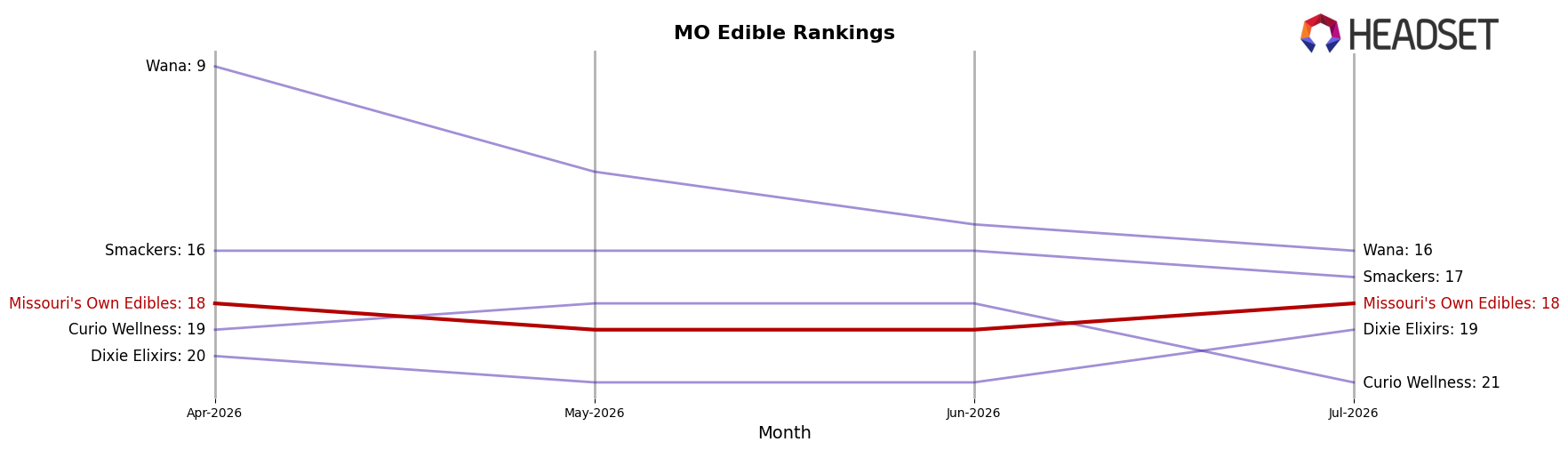

Missouri's Own Edibles sits at rank #18 in MO Edible for July 2026, unchanged YoY from rank #18, and flat versus three months ago at #18; the brand’s peak of #15 in November 2024 marks a three-position slide from its best point, while category leaders moved in divergent directions as Good Day Farm rose from #3 to #2 and Smokiez Edibles fell from #2 to #5. Compared with Gron / Grön holding #1 with a -5.47% YoY sales change and Wyld easing from #4 to #3 alongside a -4.24% YoY sales change, Missouri's Own Edibles’ static #18 rank and three-position gap from its November 2024 peak imply a stalled share position where upward mobility will require displacing mid-tier risers rather than chasing the top three.

Notable Products

CBD/CBN/THC 4:3:2 Indica Pawpaw Tranquility Fruit Gummies 10-Pack (200mg CBD, 150mg CBN, 100mg THC) posted an 82.9% month-over-month surge to rank 5, while Hybrid Raspberry Gummies 10-Pack (100mg) fell 14.9% to rank 7. At the top, CBN/THC 1:1 Indica Blackberry Gummies 10-Pack (100mg CBN, 100mg THC) slipped 12.6% but held rank 1, and CBG/THC 1:1 Sweet Green Apple Gummies 10-Pack (100mg CBG, 100mg THC) declined 8.5% at rank 2. With four of the top ten anchored in CBG-forward or CBN-forward ratios and one high-dose Indica gainer up 12.0% at rank 4, the mix points to a pivot from classic 1:1s toward differentiated minor-cannabinoid and higher-dose solutions.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.