Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

CODES is stocked at 181 licensed dispensaries across Missouri, Louisiana, and Arkansas, 136 of them in Missouri, with the deepest coverage in KCMO, St. Louis, Columbia, Springfield, and Branson. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

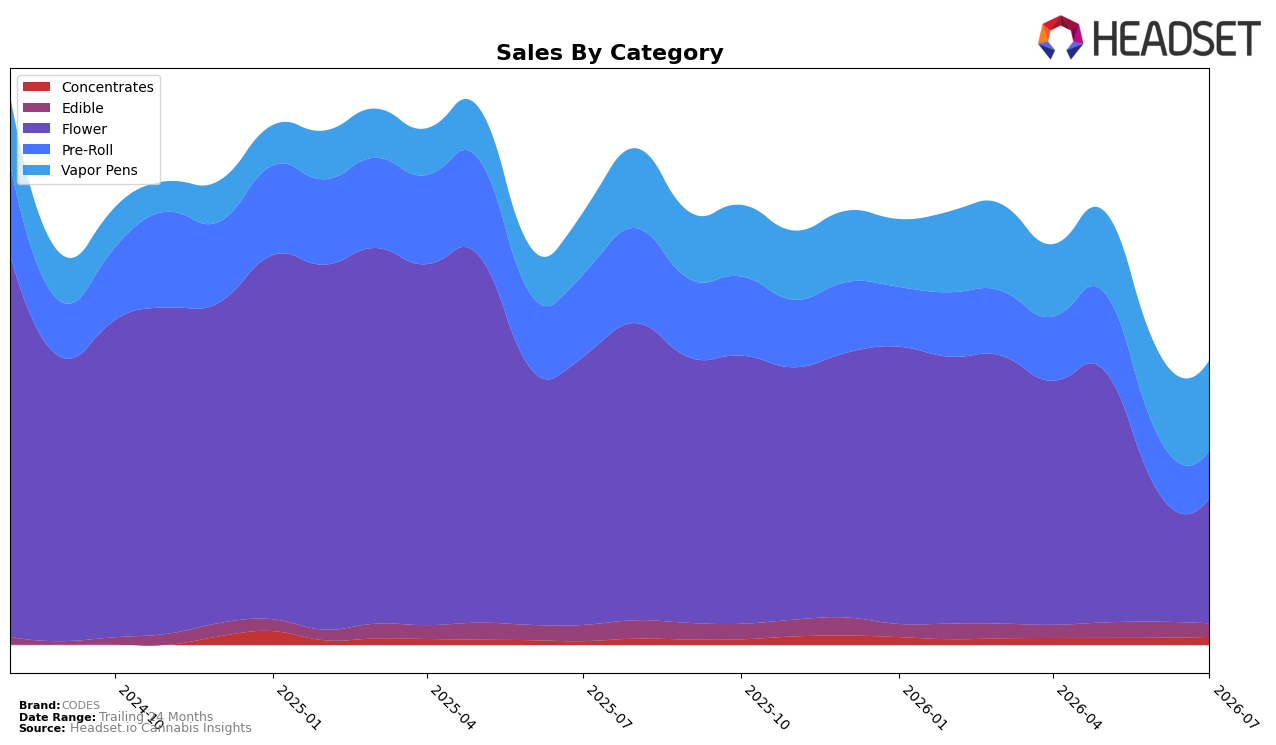

CODES concentrated 44.07% of July 2026 sales in Flower with a year-over-year decline of 53.38% and a month-over-month dip of 3.85%, while Vapor Pens rose to 31.71% share on 44.99% YoY growth and 6.54% MoM. Pre-Roll contracted to 16.76% share with YoY down 42.24% and MoM down 14.74%, and Edible slid to 4.68% share with YoY down 16.29% and MoM down 15.35%; meanwhile, Concentrates, though only 2.79% share, posted 113.78% YoY and 11.60% MoM growth. With an overall brand sales YoY change of -34.34% and an average price down 3.56%, the pattern implies mix-driven stabilization around Vapor Pens growth partially offsetting Flower and Pre-Roll declines, while Concentrates serves as a small but accelerating tailwind.

Vapor Pens’ 6.54% MoM lift alongside a 44.99% YoY increase positions the format as CODES’s near-term growth anchor, whereas Flower’s 53.38% YoY contraction and rank 8 standing in Missouri suggest reduced competitiveness in the top category. The steep MoM declines in Pre-Roll (-14.74%) and Edible (-15.35%), combined with a 3.85% MoM dip in Flower, indicate the brand is relying on higher-momentum inhalables to offset shrinking value segments; given Concentrates’ 113.78% YoY growth from a 2.79% base, the implication is a pivot toward potency-forward formats to defend share while the legacy Flower mix retrenches.

Competitive Landscape

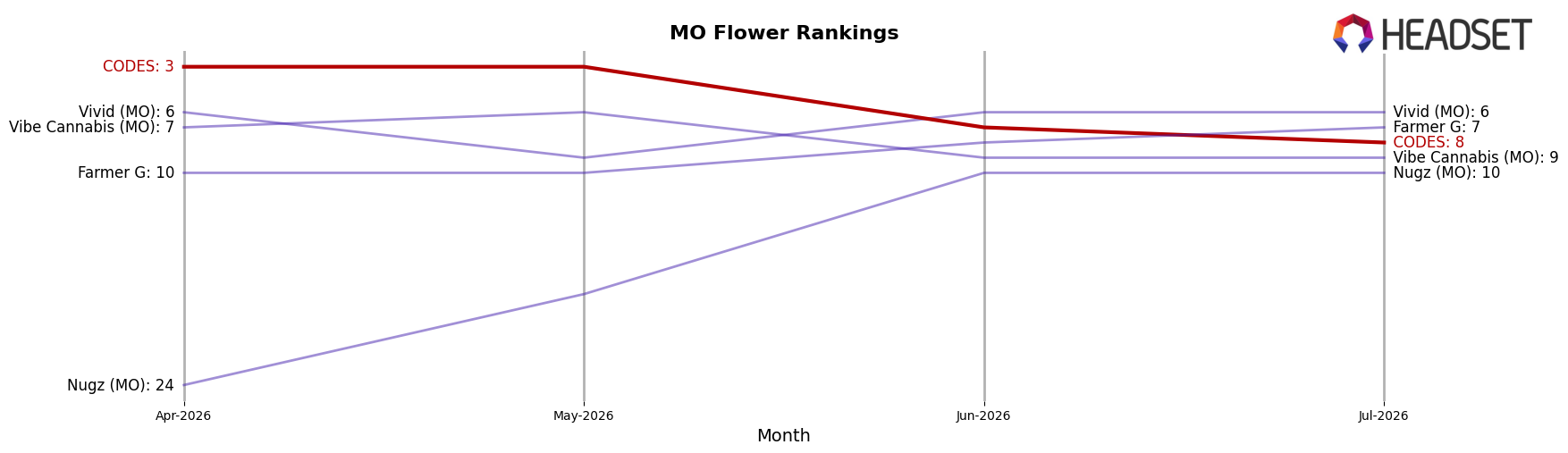

CODES sits at rank #8 in Missouri Flower in July 2026, down 6 positions from #2 year over year, and 5 spots below its April–June three-month position of #3; by contrast, Flora Farms held #1 with a -1.3% YoY sales change while Sinse Cannabis moved to #2 with +9.0% YoY, indicating CODES’ slippage is not purely category-wide. Further, Illicit / Illicit Gardens remains #3 despite a -12.8% YoY drop, whereas Amaze Cannabis advanced to #4 with +20.6% and Local Cannabis Co. climbed to #5 with +41.8%, implying CODES’ decline from a peak of #1 in August 2024 to #8 now stems from share being captured by faster-growing mid-pack rivals rather than uniform market contraction.

Notable Products

The Code- Tangie Berry BDT Distillate Disposable (1g) posted the steepest decline at -14.25% MoM while sliding to rank 4, contrasting with The Code- Lime Smoothie Ice BDT Distillate Disposable (1g) up 19.78% at rank 1. The Code - Mango Cream BDT Distillate Disposable (1g) accelerated 44.63% MoM to rank 6, and Triangle Mints Pre-Roll (1g) fell -10.92% at rank 8. With four of the top ten in Vapor Pens concentrated in the top six ranks and the leading SKU generating $295,342 in July 2026, the mix implies CODES is consolidating demand into a few flavored disposables while trimming traction in Pre-Rolls.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.