Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Mo-jo (NV) is stocked at 21 licensed dispensaries across Nevada, with the deepest coverage in Las Vegas, Henderson, North Las Vegas, Reno, and Mesquite. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

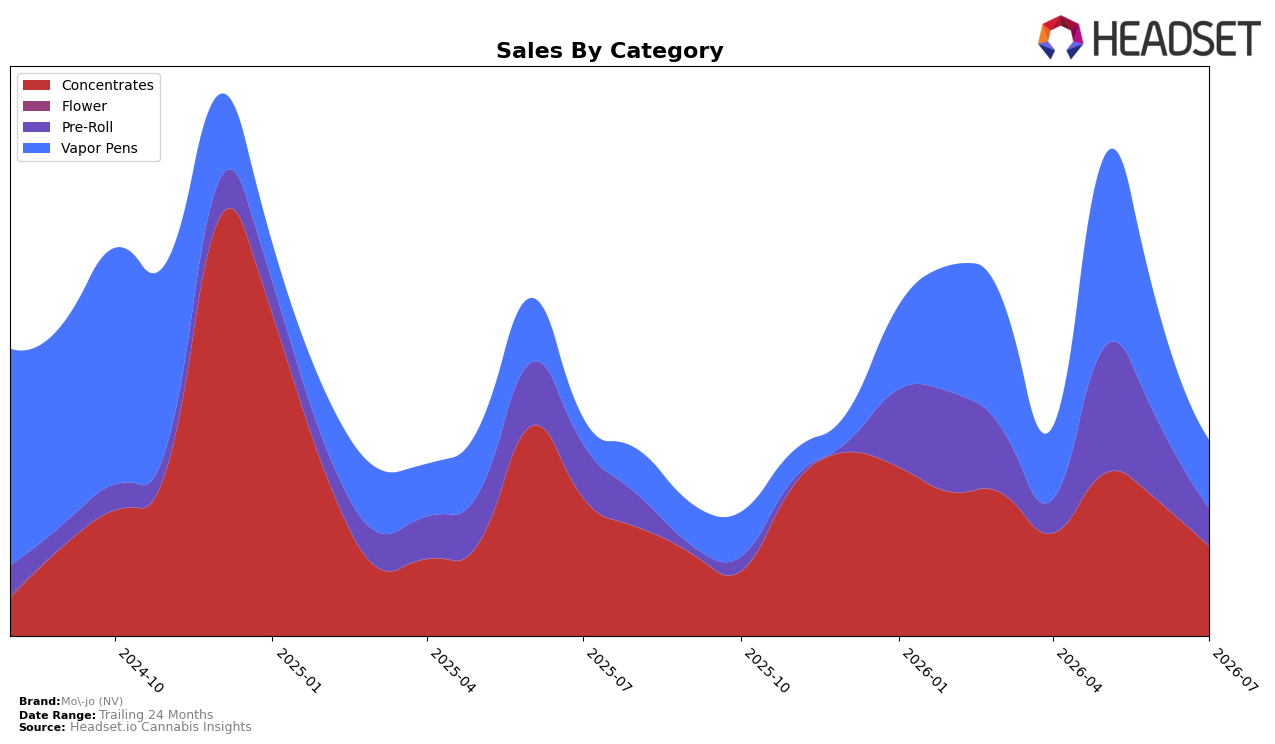

In July 2026, Mo-jo (NV)'s mix concentrated in Concentrates at 46.06% share while Vapor Pens held 34.87% and Pre-Roll 19.07%, with Concentrates down 34.89% year over year and 33.56% month over month, Vapor Pens up 162.22% year over year but down 39.71% month over month, and Pre-Roll down 30.40% year over year and 53.29% month over month. Average price rose 49.73% year over year to $24.76 as category-level declines in Concentrates and Pre-Roll coincided with a larger Vapor Pens mix, implying price-led revenue defense amid volume contraction. The pattern implies a pivot away from historically larger Concentrates volume toward higher-priced items and a more volatile Vapor Pens contribution, with July’s month-over-month double-digit drops across all three categories signaling exposure to demand elasticity and promotional cycles in Nevada.

Holding rank 16 in Nevada Concentrates while that category fell 33.56% month over month and 34.89% year over year, alongside a 162.22% year-over-year surge in Vapor Pens but a 39.71% month-over-month pullback, suggests Mo-jo (NV) is mid-pack in a declining core and reliant on a growth-adjacent, volatility-prone segment. With Pre-Roll’s 53.29% month-over-month decline and 30.40% year-over-year drop shrinking its 19.07% share, the mix now leans on two categories moving in opposite year-over-year directions, indicating that sustaining position will require stabilizing Concentrates throughput while smoothing Vapor Pens’ swings rather than chasing share where demand is whipsawing.

Competitive Landscape

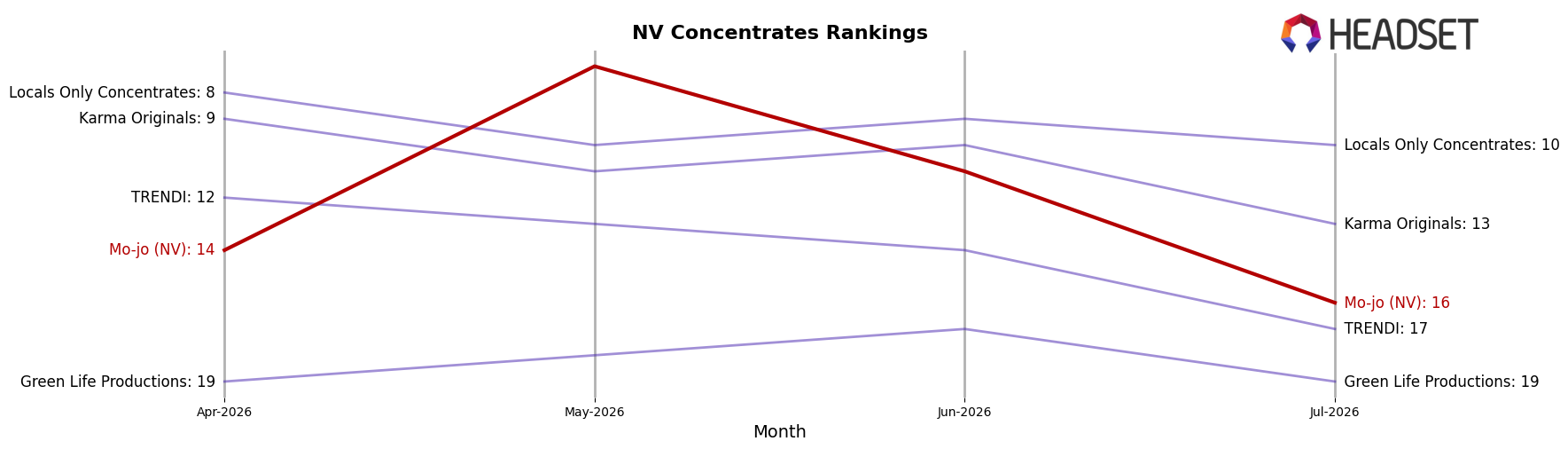

Mo-jo (NV) sits at rank #16 in NV Concentrates in July 2026, down 4 positions year over year from #12 and 2 spots since April 2026’s #14, a retreat from a peak of #4 reached in January 2025. Meanwhile, Hippies surged from #32 to #3 with a 670.3% YoY sales change, while Medizin held at #1 despite a 29.7% YoY sales decline, indicating that upward mobility at the top coexists with volatility. This combination—Mo-jo (NV) slipping 2 ranks over the last three months while City Trees edged from #5 to #4 amid a 14.9% sales contraction—implies that Mo-jo (NV)’s rank trajectory is being shaped more by competitors’ rapid gains and positional stickiness than by broad market expansion, pointing to a share-defense challenge rather than a category tailwind.

Notable Products

Zodiac Killer Distillate Cartridge (1g) posted the steepest contraction at -29.98% month over month while sliding to rank 4, and The Jam Distillate Cartridge (1g) also fell -17.07% at rank 3, indicating demand is rotating within the pen lineup rather than expanding uniformly. Pineapple Fanta Live Cartridge (1g) holds rank 1 and Peachy Pleasure Distillate Cartridge (1g) sits at rank 2, while five of the top six are Vapor Pens, concentrating share at the top even as mid-tier SKUs weaken; this mix implies Mo-jo (NV) is consolidating around a few lead flavors while pruning underperforming variants. Pineapple OG Cured Badder (4g) reaches rank 9 with $5,604 in July 2026 and, together with two other Concentrates in ranks 7–9, signals heavier-size or value-oriented Concentrates are acting as a secondary growth lane alongside pens; the pattern points to a barbell strategy where flagship pens drive visibility and larger-pack Concentrates capture basket trade-up.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.