Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

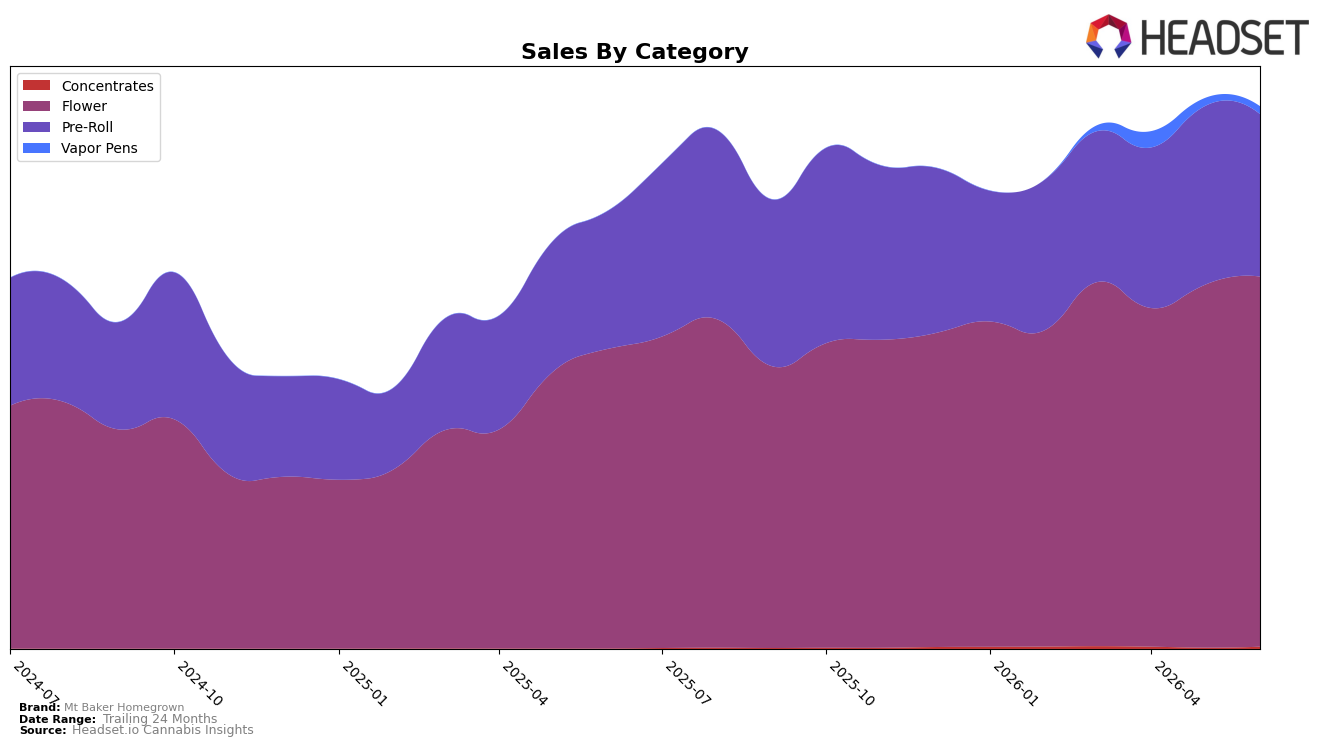

In June 2026, Mt Baker Homegrown concentrated 68.31% of sales in Flower with year-over-year growth of 23.55% and month-over-month growth of 2.06%, while Pre-Roll held 29.94% share with 17.59% year-over-year growth but a 9.12% month-over-month decline. Smaller lines moved in opposite directions: Vapor Pens at 1.40% share slipped 2.67% month over month with no comparable year-over-year base, whereas Concentrates, though just 0.35% share, surged 97.68% month over month and 1,139.92% year over year. With Flower leading and Pre-Roll contracting month to month, the mix implies recent volume is tilting back toward Flower even as niche categories add incremental breadth.

The brand’s 16 rank in Flower in Washington alongside a 5.35% year-over-year increase in average price and a 2.06% month-over-month Flower lift suggests pricing power is being absorbed without suppressing core demand. At the same time, a 9.12% month-over-month pullback in Pre-Roll against a 97.68% month-over-month spike in Concentrates indicates substitution toward higher-potency or differentiated formats, implying Mt Baker Homegrown’s near-term positioning is anchored in Flower leadership while selectively expanding into Concentrates to diversify beyond a Pre-Roll plateau.

Competitive Landscape

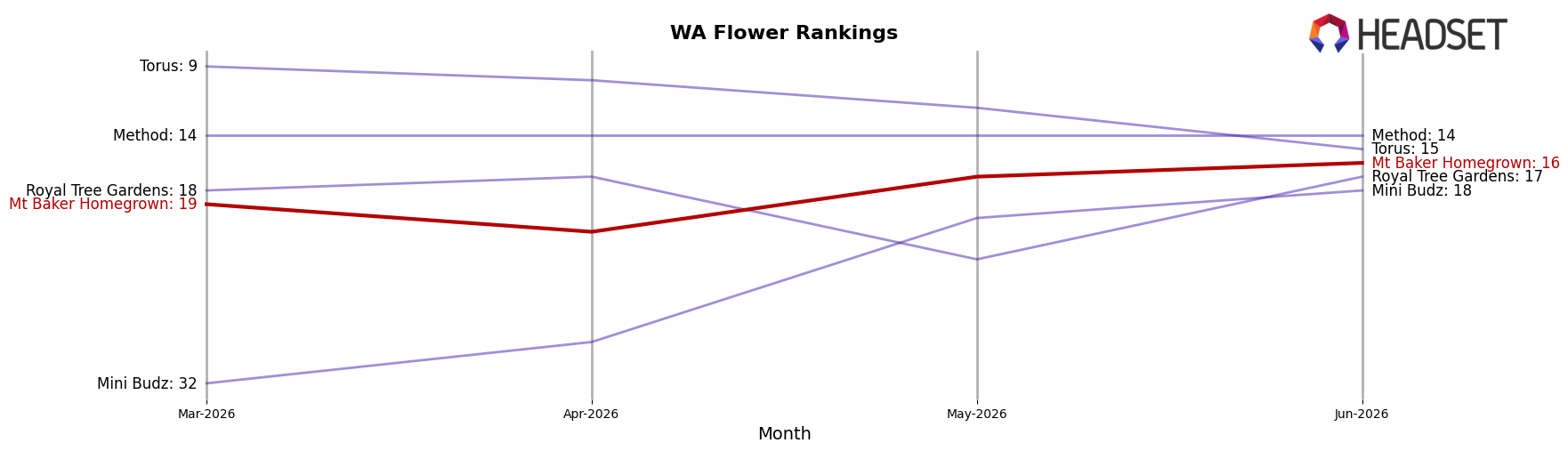

Mt Baker Homegrown sits at rank #16 in WA Flower in June 2026, improving 9 positions from #25 year over year, and up 3 spots from #19 in March 2026; the current position also marks a peak rank of #16 in June 2026. In contrast, Phat Panda held steady at #1 year over year with a 16.6% YoY sales increase, while Legends stayed at #2 despite a 19.8% YoY sales decline, and Sweetwater Farms advanced to #5 alongside a 65.8% YoY sales gain. The mix of stable leaders and faster-rising mid-pack brands implies Mt Baker Homegrown’s rank trajectory is upward but crowded, suggesting that consolidating share now is necessary to translate the 9-rank YoY climb into durable top-15 presence.

Notable Products

Blueberry Pre-Roll 10-Pack (5g) posted the steepest movement in June 2026 with a -53.2% MoM drop while sliding to rank 9, whereas Gelato 33 Pre-Roll 10-Pack (5g) fell -22.3% yet held rank 1. Gelato #33 (14g) in Flower declined -9.8% at rank 4, and Permanent Marker Pre-Roll 2-Pack (1g) decreased -12.7% at rank 6. With eight of the top ten in Pre-Roll and two multi-pack SKUs moving down over -20%, the portfolio is concentrated in value-pack formats that are now absorbing price or velocity pressure, implying a near-term need to rebalance toward fewer but stickier Pre-Roll leaders and a steadier Flower anchor.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.