Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

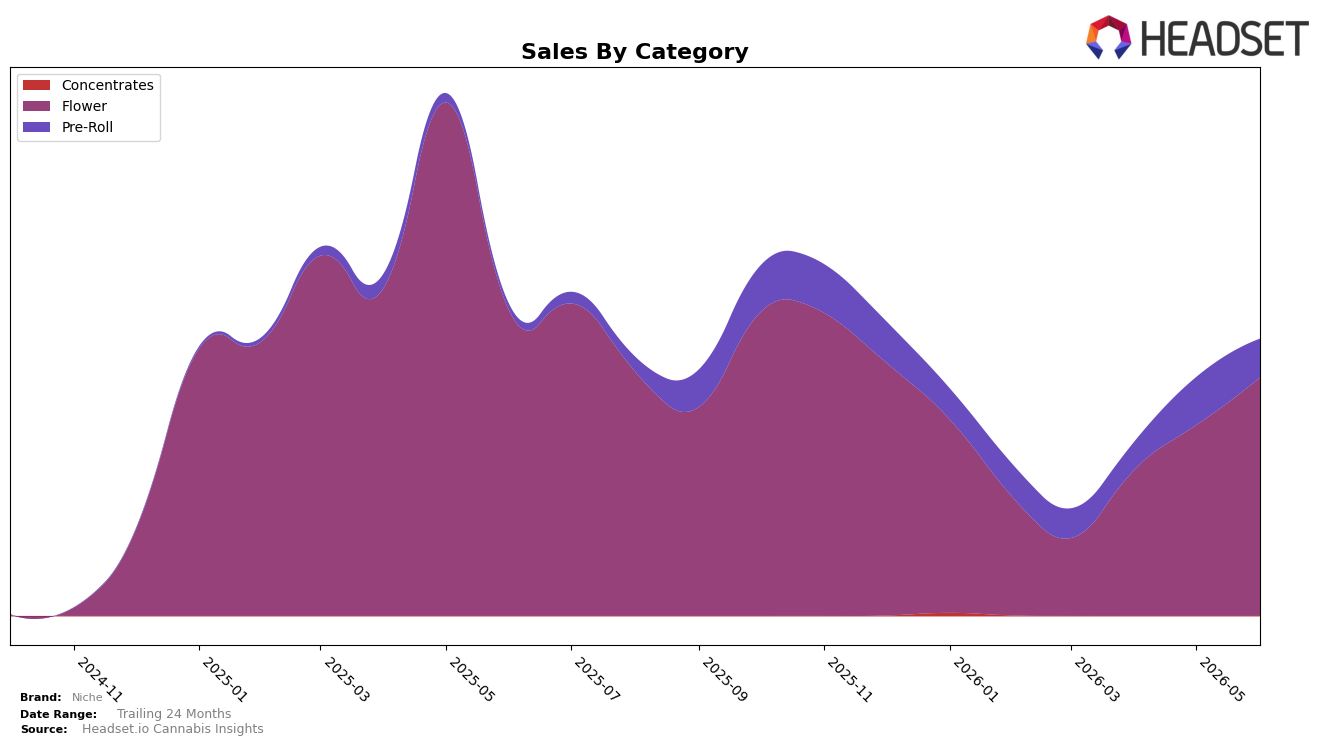

Niche concentrated 86.11% of June 2026 sales in Flower, where sales were down 21.69% year over year but up 24.98% month over month, while Pre-Roll held 13.89% share with a 525.76% year-over-year surge and a 19.42% month-over-month decline. The average price fell 18.47% year over year to $33.98 alongside a total brand sales decline of 10.86% year over year, indicating that June 2026 growth was driven by unit volume in lower-priced segments even as the Flower-heavy mix limited top-line recovery. The pattern implies a pivot from premium-priced reliance toward volume-focused categories, positioning Niche to trade more on accessibility than on price per unit within its current mix.

With Flower anchoring the portfolio at rank 28 in New Jersey Flower and delivering a 24.98% month-over-month rebound, Niche’s category footprint ties near-term momentum to a single core lane while relying on Pre-Roll for incremental reach despite a 19.42% month-over-month pullback. The 525.76% year-over-year Pre-Roll expansion against an 18.47% average price decline and a 10.86% brand sales contraction suggests a trade-down dynamic that can lift units but compress mix quality; this implies that maintaining the June 2026 lift requires stabilizing Flower velocity while selectively expanding Pre-Roll to balance rank pressure with margin discipline.

Competitive Landscape

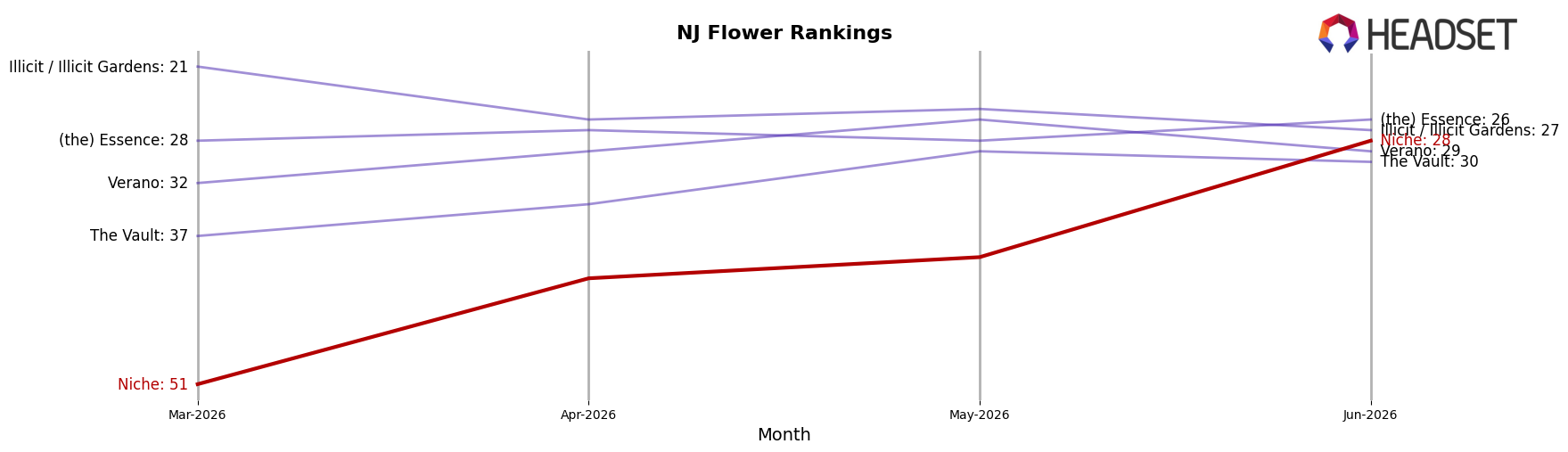

Niche sits at #28 in NJ Flower in June 2026, down 2 ranks year over year from #26 but up 23 places versus March 2026’s #51, indicating recovery from a recent trough despite a YoY slippage. Meanwhile, Find. climbed from #12 to #1 with 225.99% YoY sales growth, while Ozone held at #2 despite a -10.61% YoY sales decline, establishing a bar where rank momentum can decouple from sales direction. Niche’s peak of #16 in May 2025 and current #28 positioning versus competitors that either surged in rank (e.g., Good Green from #11 to #3) or maintained top-5 status (Simply Herb from #9 to #4) implies that recent quarter-over-quarter gains must persist to translate the 23-place rebound since March 2026 into durable top-20 reentry.

Notable Products

Pie Scream (3.5g) posted the largest move in June 2026 with +129.4% MoM to rank 1, while Bluephoria (3.5g) fell 39.4% MoM at rank 7, indicating volatility clustered at both the top and mid-table. Pink Ink (3.5g) rose 69.0% MoM to rank 3 as First Class Gas (3.5g) inched up 4.5% at rank 2, suggesting gains are concentrated in a couple of breakout Flower SKUs rather than broad lift. With seven of the top ten as Flower entries and Pre-Rolls split between a +63.3% MoM Zereal Milk Pre-Roll 2-Pack (1g) at rank 4 and a -14.6% MoM Pie Scream Pre-Roll 2-Pack (1g) at rank 5, category momentum is skewed toward Flower while Pre-Roll performance is mixed. The pattern implies Niche is tilting its commercial mix toward high-velocity Flower leaders while pruning or repositioning uneven Pre-Rolls to stabilize mid-rank churn.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.