Where to Buy

Noble Farms is stocked at 80 licensed dispensaries across Oregon and Washington, 76 of them in Oregon, with the deepest coverage in Portland, Bend, Eugene, Medford, and Salem. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

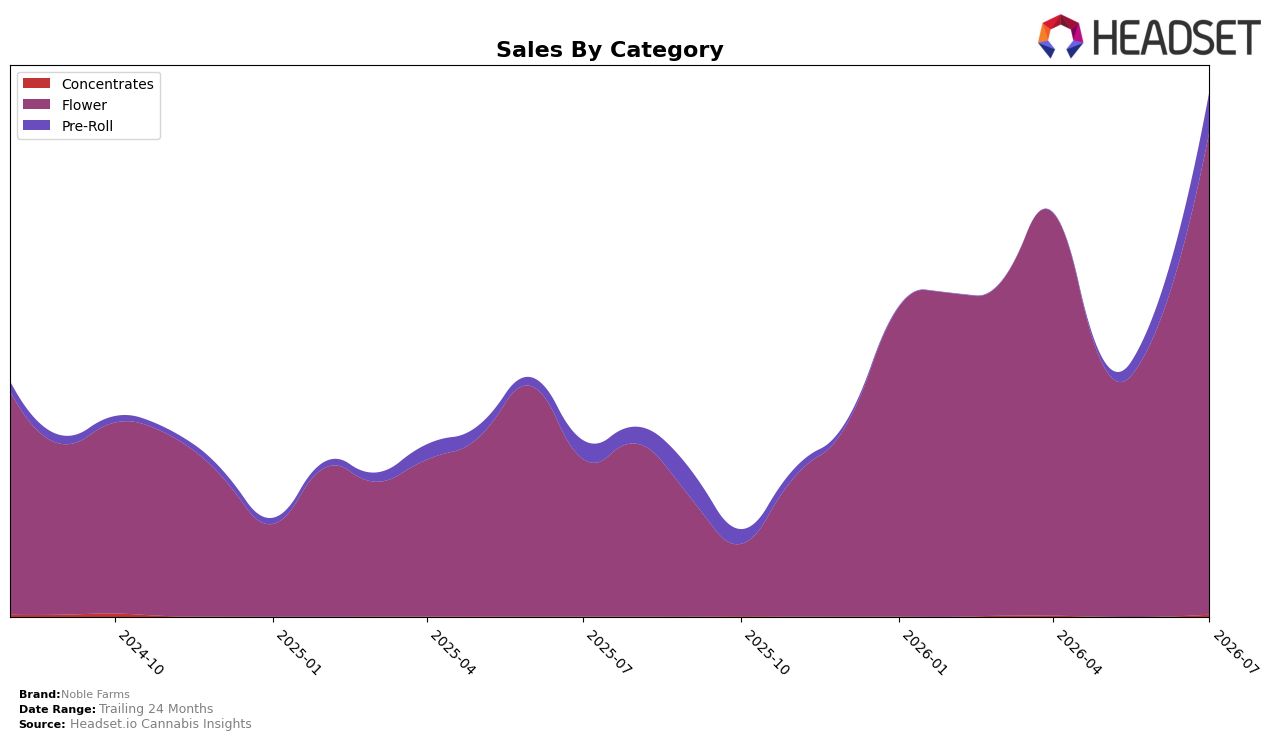

In July 2026, Noble Farms concentrated 92.0% share in Flower and 7.6% in Pre-Roll, with Concentrates at 0.4%, while Flower sales grew 207.7% year over year and 66.4% month over month. Pre-Roll expanded 115.7% year over year and 72.2% month over month, and Concentrates posted 870.9% year over year from a small base, signaling experimentation despite a near-zero share; the brand’s average price rose 46.6% year over year to $25.85, while Flower pricing averaged $32.02 in July 2026. Combined with overall brand sales up 198.8% year over year and 127.4% over 24 months, the tilt toward Flower with accelerating Pre-Roll suggests a volume-led expansion anchored in core inhalables, implying pricing power is being sustained without diluting mix.

Positioning-wise, the 92.0% Flower mix alongside a 16th rank in Flower in Oregon indicates the brand competes where it is most visible, and the 72.2% month-over-month lift in Pre-Roll offers a hedge within the same consumer mission. The 46.6% year-over-year average price increase alongside 66.4% month-over-month Flower growth points to headroom for premiumized units without suppressing demand, while the 870.9% year-over-year rise in Concentrates, albeit at 0.4% share, functions as optionality rather than a pivot. These shifts imply Noble Farms is consolidating a Flower-first identity in Oregon while selectively scaling complementary formats to protect share and price laddering within inhalables.

Competitive Landscape

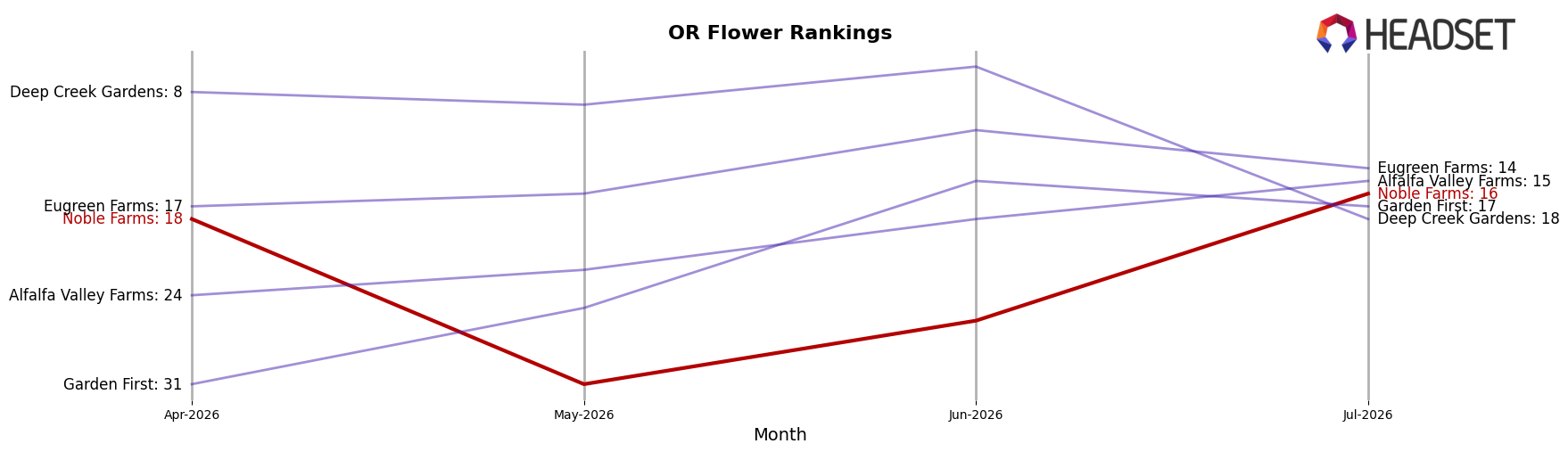

Noble Farms ranks #16 in OR Flower in July 2026, a 38-place climb from #54 year over year, and up 2 positions from #18 three months ago; this new #16 also marks its peak rank to date in July 2026. In contrast, PRUF Cultivar / PRŪF Cultivar held steady at #1 with a 0.5% rank change year over year while Grown Rogue advanced from #3 to #2, and Otis Garden jumped from #12 to #4 alongside an 86.2% sales increase; meanwhile, Bald Peak slipped from #2 to #5 with a -15.5% sales change. The combination of a 38-rank YoY surge and a 2-position gain since April 2026 implies Noble Farms is moving from peripheral to mid-pack consideration, but the top-five congestion suggests future share capture will depend on converting recent rank momentum into sustained velocity gains.

Notable Products

OMMP Bluberry Pre-Roll 2-Pack (1g) posted the standout move in July 2026 with a +90.8% month-over-month surge to rank 2, while Koji Sunberry Pre-Roll 2-Pack (1g) followed with +71.6% to rank 3, indicating that pre-roll momentum outpaced flat-to-unknown movement in several Flower SKUs. Orange Slyce (1g) held rank 1 despite no reported month-over-month figure, and three of the top five ranks are Flower, suggesting core volume still concentrates there even as pre-rolls accelerate. With two pre-rolls in the top three and Jack Herer x Silver Lining (1g) advancing +48.9% at rank 6 alongside Silver Snowman (1g) at +43.5% and rank 8, the mix tilts toward fast-moving value formats layered on a Flower-led base. The pattern implies Noble Farms is shifting toward a barbell of premium Flower ranks and high-velocity pre-rolls, positioning assortment to capture both trade-down and loyal strain-driven demand.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.