Where to Buy

OG Farms is stocked at 100 licensed dispensaries across Michigan, with the deepest coverage in Detroit, New Buffalo, Monroe, Inkster, and Kalamazoo. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

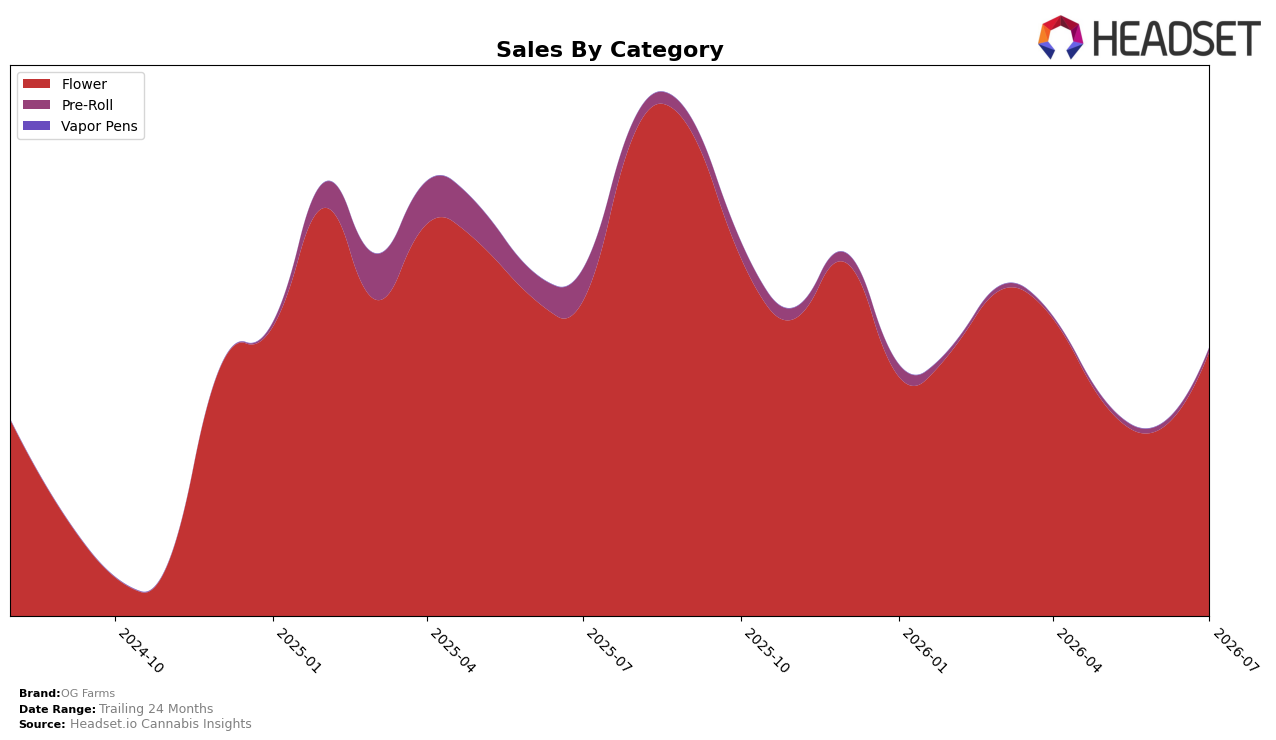

Market Insights Snapshot

OG Farms concentrated 98.49% of July 2026 sales in Flower, with Pre-Roll reduced to 1.51% share; within this mix, Flower grew 42.63% month over month while Pre-Roll fell 5.37% MoM, and year over year Flower declined 16.10% as Pre-Roll contracted 87.22%. Despite brand-level sales down 22.61% YoY against a 55.64% YoY increase in average price to $15.95, Flower’s sharp MoM rebound alongside an almost negligible Pre-Roll presence signals a deliberate pivot toward higher-priced Flower and away from low-price Pre-Roll, concentrating exposure in a single category that both lifted short-term volume and amplified sensitivity to category swings.

In Michigan Flower, OG Farms sits at rank 16 while carrying a 98.49% category concentration and a 42.63% MoM uptick in Flower, which indicates momentum within its core lane but limited diversification to buffer the 16.10% YoY category decline. With average Flower pricing at $17.27 versus a brand-average price up 55.64% YoY, the positioning implies a premium-leaning Flower strategy that can capture monthly surges yet leaves July 2026 performance vulnerable to further YoY softness unless the 1.51% Pre-Roll share stabilizes or new categories are added to smooth volatility.

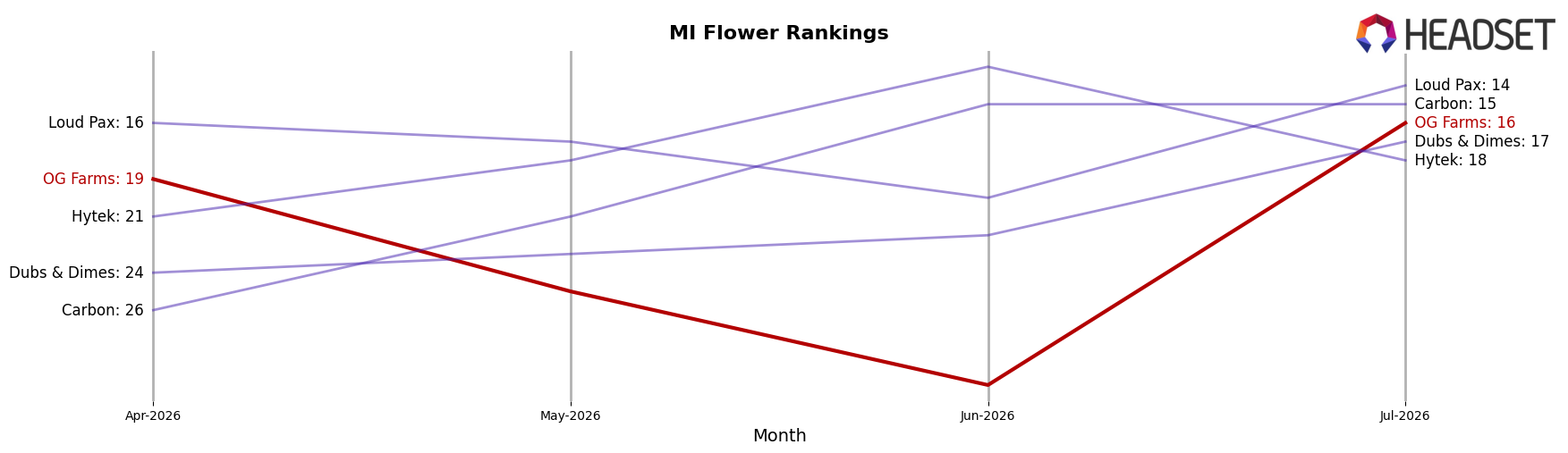

Competitive Landscape

OG Farms sits at rank #16 in Michigan Flower in July 2026, slipping 1 position year over year from #15, yet improving 3 spots versus April 2026 when it was #19; meanwhile, category leader High Minded holds at #1 year over year despite a 12.46% sales decline, and Goodlyfe Farms advanced from #5 to #3 on 36.83% sales growth. With a prior peak at #9 in September 2025 and a three-month climb from #19 to #16, the mix of a slight YoY rank dip (−1) alongside short-term upward movement (+3) implies OG Farms is stabilizing mid-tier but must outpace faster risers like Mischief, which leapt from #10 to #4 on 59.39% growth, to re-enter the top 10.

Notable Products

Grape Pie (28g) set the tone in July 2026 with a 193.6% month-over-month surge to rank 1, while Candy Fumez (28g) followed at rank 2 with a 95.7% gain. Gorilla Glue (28g) added breadth with a 139.7% rise to rank 3, and Bop Gun (28g) contrasted with a -54.4% drop to rank 8. Six of the top ten are 28g Flower SKUs, indicating OG Farms is consolidating demand around large-format Flower where outsized movers are reshaping the leaderboard.

Biscotti (28g) slipped a modest -1.1% at rank 5 as Bop Gun (Bulk) advanced 65.6% to rank 7, suggesting pack-size trade-offs are shifting within the same strain family. Kombucha (28g) fell -15.3% to rank 10, introducing downside at the tail even as top ranks concentrate gains; combined with Wedding Cake Badder (Bulk) holding rank 9 at $20,879, the mix tilts toward Flower over extracts. The pattern implies OG Farms is leaning into high-velocity 28g Flower to capture volume while de-prioritizing slower 28g variants and keeping bulk options as selective volume levers.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.