Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

OMO - Open Minded Organics is stocked at 49 licensed dispensaries across New York, with the deepest coverage in New York, Buffalo, Farmingdale, Rochester, and Syracuse. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

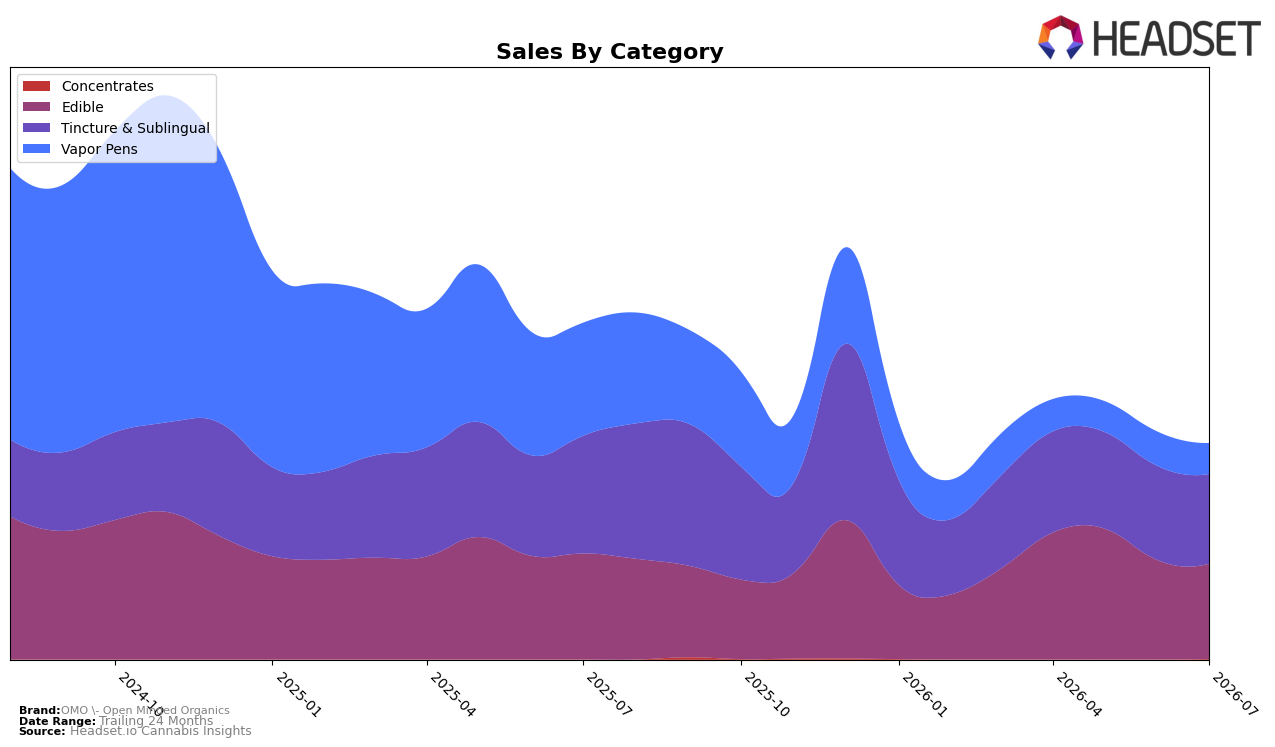

OMO - Open Minded Organics concentrated 85.5% of July 2026 sales in Edible and Tincture & Sublingual, with Edible at 44.11% share and Tincture & Sublingual at 41.44%, while Vapor Pens fell to 14.23% share. Year over year, Edible declined 10.0% and Tincture & Sublingual dropped 23.9%, but Vapor Pens contracted 72.8%; month over month, Edible slipped 4.0% and Tincture & Sublingual eased 4.7% versus a sharper 10.1% drop in Vapor Pens. Average price fell 15.2% year over year to $35.59 while Edible pricing sat lower at $25.83 and Tincture & Sublingual higher at $57.90, pointing to mix-driven ASP pressure. The pattern implies the brand is leaning into lower-priced Edibles while exiting higher-churn Vapor Pens, trading short-term revenue for steadier category exposure.

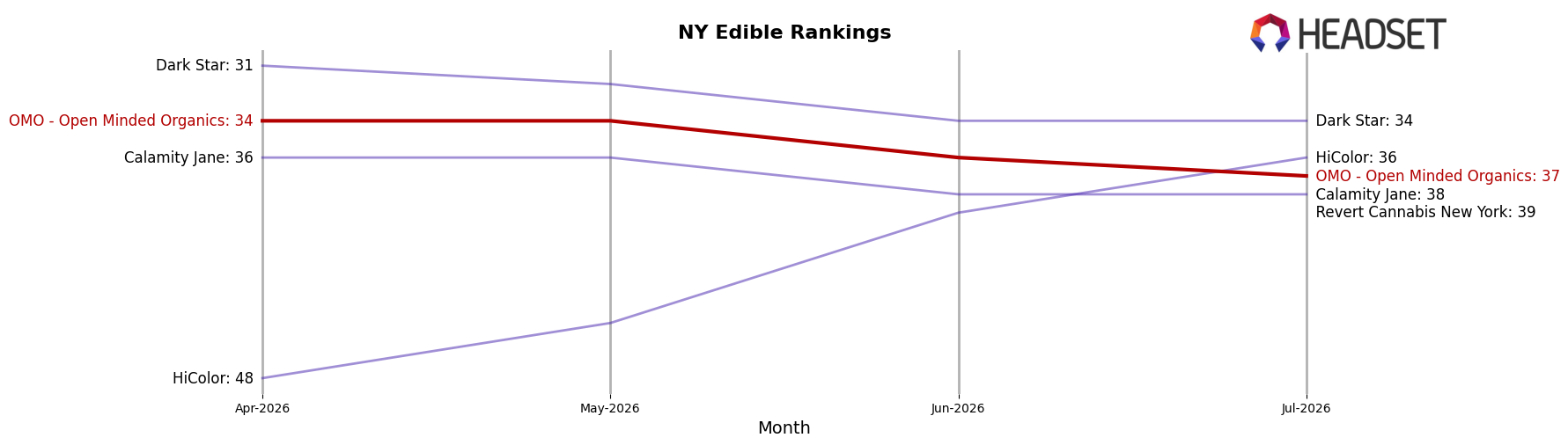

Within New York Edibles, a category rank of 37 combined with a 4.0% month-over-month dip and 10.0% year-over-year decline signals limited shelf velocity relative to peers in that segment, while the 23.9% year-over-year slide in Tincture & Sublingual alongside a 4.7% monthly decline suggests reduced repeat pull at higher price points. With Vapor Pens down 72.8% year over year and 10.1% month over month, the brand’s exposure to fast-cycling inhalables is shrinking, concentrating demand in formats where price elasticity is tighter. This positioning implies a pivot toward value-accessible Edibles to stabilize share while the premium Tincture & Sublingual line requires price-pack or potency architecture to defend rank and mitigate further share erosion.

Competitive Landscape

OMO - Open Minded Organics sits at rank #37 in New York Edible for July 2026, slipping 3 positions year over year from #34, while also falling 3 places versus three months prior from #34, indicating a downward drift as the category’s top tier consolidates. In contrast, Off Hours moved down from #1 to #2 alongside a -10.4% year-over-year sales change, whereas Wyld held steady at #3 with a 7.4% year-over-year sales increase, signaling that stability or gains among leaders are coinciding with OMO - Open Minded Organics’ slide from its August 2024 peak of #25 to the current #37; the trajectory implies share is concentrating at the top, and without a rank rebound of at least 8-10 positions, OMO - Open Minded Organics risks further marginalization in late 2026.

Notable Products

Sweet Tangie DSO Gummies 10-Pack (100mg) posted the steepest decline in July 2026 at -41.8% while sliding to rank 10, and Strawberry DSO Gummies 10-Pack (100mg) fell -14.1% at rank 7, indicating flavor-specific demand is fragmenting even as Blueberry RSO Gummies 10-Pack (100mg) jumped +108.6% to rank 1. Standardized DSO Infused Oil Tincture (1000mg THC, 30ml) dipped -6.4% at rank 2 while the 100mg variant rose +8.7% at rank 3, pointing to price/strength laddering where the flagship potency is giving up mix to lower-dosage entry. Four of the top ten are Edible SKUs concentrated in RSO/DSO gummies, yet Vapor Pens weakened with Purple Urkle RSO Distillate Cartridge (1g) down -21.9% at rank 9 versus Cherry Glurp (1g) down -0.8% at rank 8, implying format momentum is consolidating in value-driven edibles despite volatility by flavor. The pattern suggests OMO - Open Minded Organics is pivoting toward an edible-led mix anchored by a breakout hero SKU while tightening portfolio breadth in underperforming vape and DSO gummy flavors to stabilize repeat velocity and margin per unit.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.