Where to Buy

Panda (MO) is stocked at 115 licensed dispensaries across Missouri and Oklahoma, 107 of them in Missouri, with the deepest coverage in St. Louis, KCMO, Springfield, Columbia, and Joplin. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

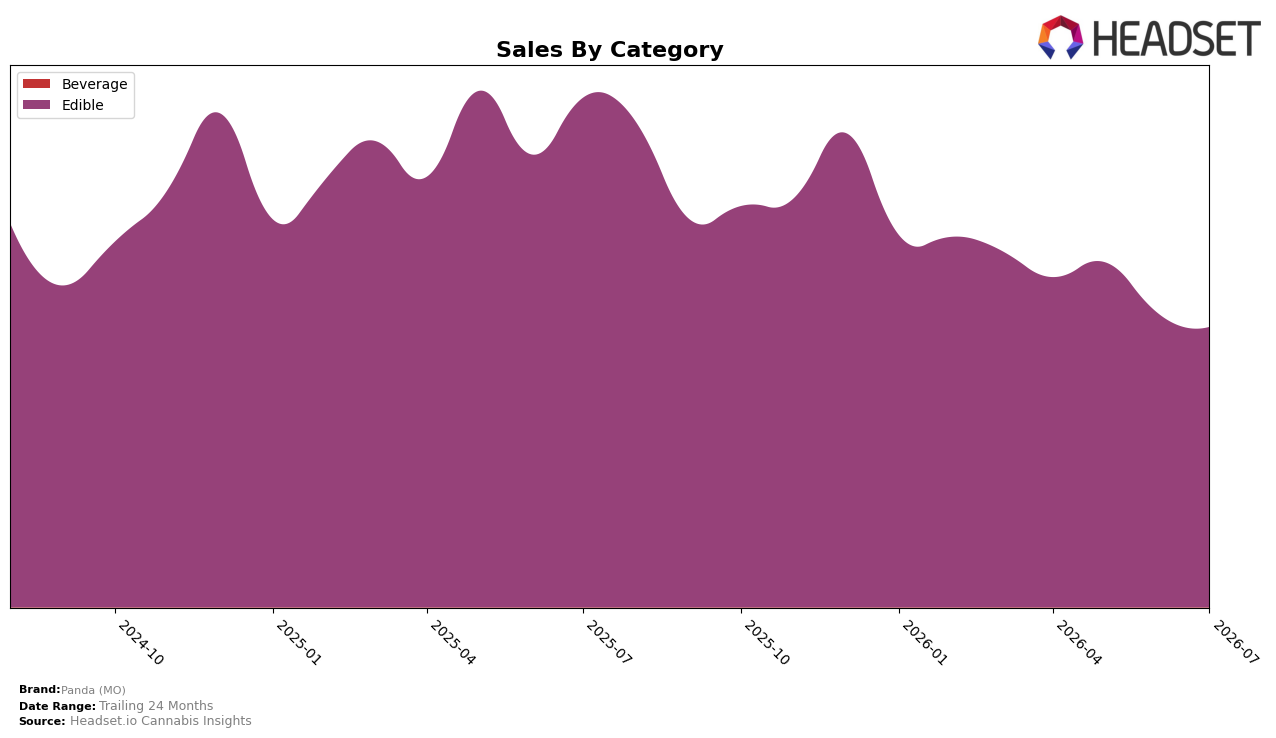

Panda (MO) concentrated 99.99% of July 2026 sales in Edible, while Beverage held 0.01% and carried no year-over-year or month-over-month trend, indicating a near-single-category profile rather than a portfolio. Within Edible, year-over-year sales fell 45.03% and month-over-month slipped 4.66%, while the brand-wide average price in July 2026 edged up 0.53% year over year, producing a mix of volume contraction against a stable price point. In Missouri Edible, the brand sat at rank 10, and brand-level sales were down 45.03% year over year and 43.76% over 24 months, implying that July 2026 merchandising should prioritize depth within Edible over breadth because diversification is not contributing measurable lift.

The 99.99% Edible share paired with a rank of 10 and a 4.66% month-over-month decline implies the brand is exposed to seasonal and promotional swings within a single aisle rather than buffered by cross-category demand. With July 2026 average prices up 0.53% year over year while sales fell 45.03% in Edible, the elasticity signal points to volume as the primary drag rather than price compression, suggesting that regaining shelf velocity in Missouri hinges on mix tactics inside Edible (form factors, pack sizes) rather than price cuts or Beverage expansion. The positioning takeaway is to defend and climb from rank 10 in Edible by reallocating support toward high-velocity Edible subsegments and timing resets to counter the recent 4.66% month-over-month dip, because the near-zero Beverage base will not shift total share in the near term.

Competitive Landscape

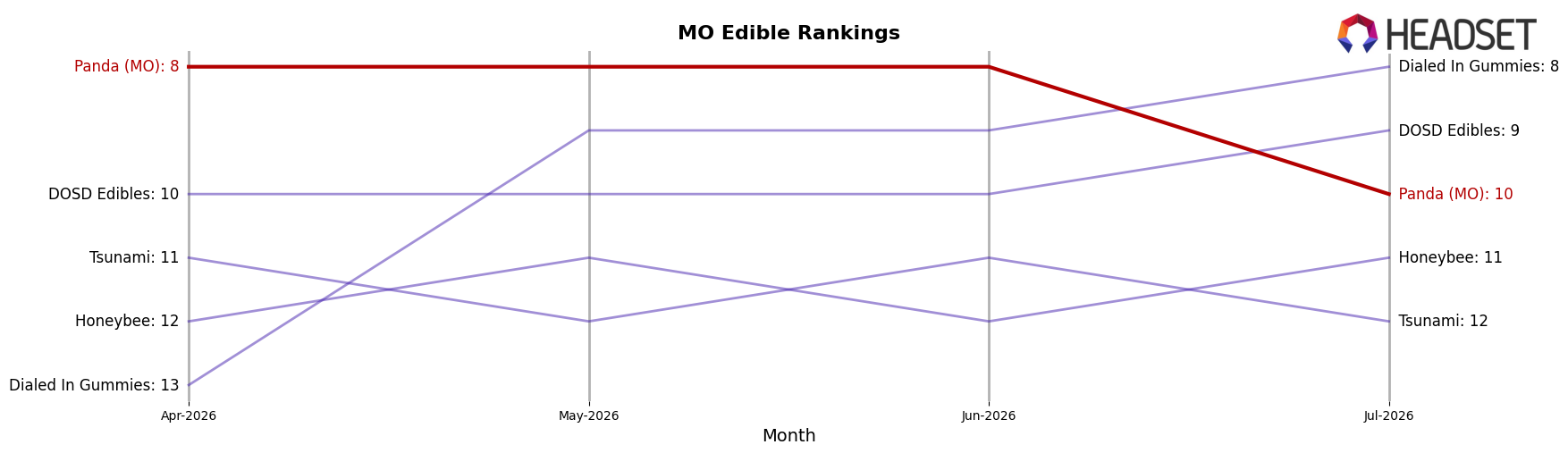

Panda (MO) sits at rank #10 in Missouri Edible for July 2026, down 5 places year over year from #5, and 2 places lower than April 2026 when it was #8; versus peers, Good Day Farm holds #2 with a 1-place gain from #3 year over year while growing sales by 11.8%, and Smokiez Edibles is #5 after sliding 3 spots from #2 with sales down 18.1%, indicating Panda (MO)’s 5-rank YoY decline and 2-rank drop since April 2026 reflect share being ceded to climbers like Good Taste moving from #8 to #4 while Panda (MO) has not converted its July 2025 peak of #5 into sustained placement.

Notable Products

Strawberry Lemonade FECO Gummies 20-Pack (100mg) posted the steepest decline at -19.8% month over month and slid to rank 2, while Mixed Berry FECO Gummies 20-Pack (100mg) fell -16.5% to rank 4, indicating demand is rotating away from standard 100mg FECO formats. Black Cherry FECO Gummies 2-Pack (100mg) dipped a lighter -4.0% yet held rank 1, and Sativa Mango Punch Feco Fruit Gummies 20-Pack (300mg) contracted -13.7% at rank 8, showing potency-tiered packs are not insulating against softer pull-through. With eight of the top ten being Edible gummies and the 500mg Mixed Berry variant down -7.0% at rank 5 against the 20-Pack Black Cherry at rank 7 and -8.3%, the pattern points to price-pack architecture, not flavor, as the primary lever; Panda (MO) should lean into fewer, clearer value tiers and rationalize overlapping 100mg SKUs to protect velocity.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.