Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

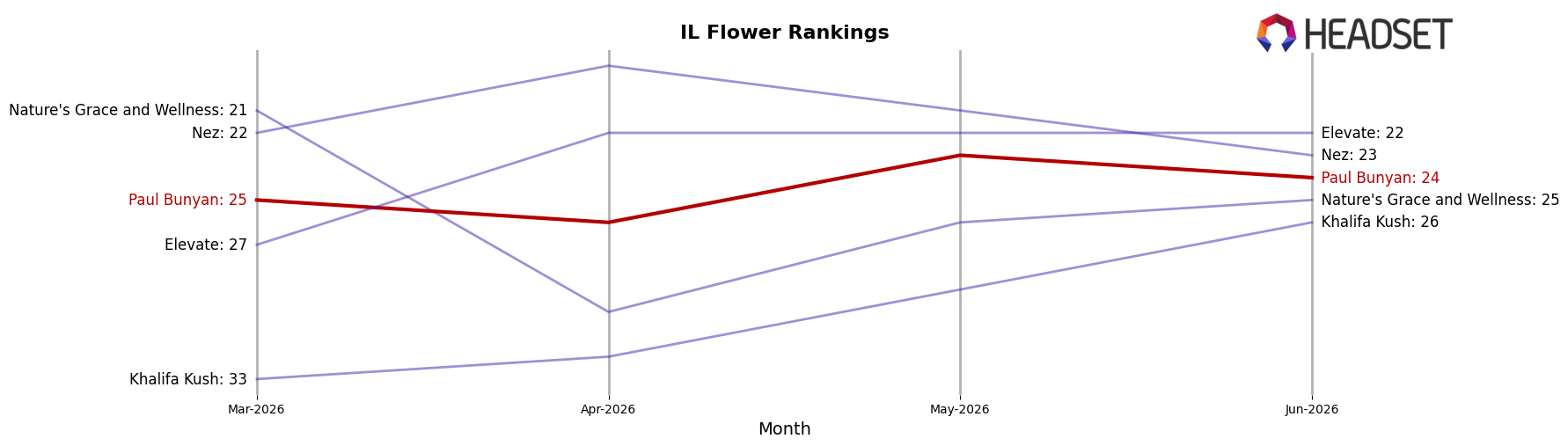

Paul Bunyan concentrated 81.15% of June 2026 sales in Flower while Pre-Roll held 18.79%, with Concentrates at 0.06%; within that mix, Flower declined -2.69% year over year and -9.67% month over month, whereas Pre-Roll grew 40.16% year over year but fell -28.68% month over month. Despite brand-level sales rising 89.66% year over year and average price up 1.33%, category depth narrowed as Concentrates plunged -97.58% year over year and -69.15% month over month, and the brand sat at rank 24 in Flower in Illinois. The combined signal is a reliance on Flower for volume with volatility in Pre-Roll momentum, implying a mix strategy that lifts annual growth but heightens month-to-month risk around a single anchor category.

With Flower at 81.15% share and a rank position of 24 in Illinois Flower, the brand is anchored mid-pack while Pre-Roll’s 40.16% year-over-year surge and -28.68% month-over-month drop indicate trend-chasing exposure rather than durable repeat behavior; meanwhile, Concentrates’ -97.58% year-over-year collapse effectively removes a tertiary entry point. Given a 62.24% decline over 24 months alongside a current-year rebound of 89.66%, the positioning reads as recovery concentrated in Flower with limited category diversification, suggesting that sustaining share will depend on stabilizing Pre-Roll churn and arresting the -9.67% month-over-month Flower slide rather than adding breadth at negligible 0.06% Concentrates share.

Competitive Landscape

Paul Bunyan sits at rank #24 in June 2026, improving 2 positions from #26 year over year while slipping 1 spot from #25 over the last three months; this contrasts with High Supply / Supply holding #1 with a 0-position YoY change and 32.1% YoY sales growth, and RYTHM steady at #2 with a 0-position YoY change despite a -5.2% YoY sales decline. The current #24 is far from the #10 peak achieved in September 2024, and the year-over-year rise of 2 ranks alongside a recent 1-rank quarterly dip indicates stabilization below prior peak while top rivals either consolidate (High Supply / Supply flat at #1) or soften (RYTHM flat at #2 with negative growth), implying Paul Bunyan’s trajectory points to incremental share recovery that will likely require outperforming mid-tier climbers to re-enter the top 20.

Notable Products

MAC Pre-Roll (1g) fell 43.2% month over month to rank 1 in June 2026 while Lemon Cherry Gelati Pre-Roll (1g) dropped 29.8% at rank 2, indicating that the very top of the list is being propped up by declining pre-rolls rather than rising demand. Apple Fritter (3.5g) held rank 10 with $20,321 in June 2026 as three Flower SKUs occupied ranks 3–5, so half of the top ten are Flower while five of the top ten are Pre-Roll. The pattern implies a pivot toward Flower for volume stability as Pre-Roll volatility at the very top strains repeatability in June 2026.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.