Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

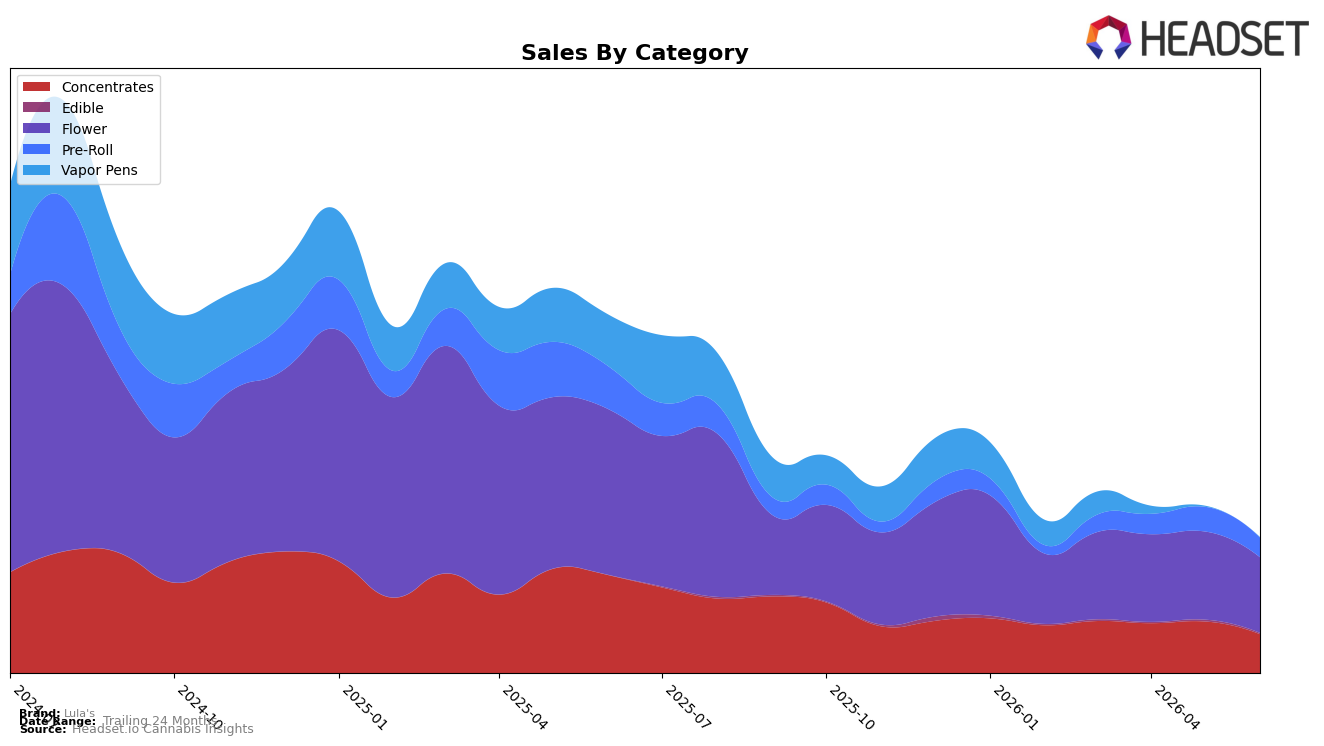

In June 2026, Lula's revenue mix concentrated further into Flower at 55.95% share while Concentrates held 28.66% and Pre-Roll accounted for 14.49%, as Vapor Pens contracted to 0.16% and Edible to 0.75%. Year over year, Flower declined 54.44% and Pre-Roll fell 54.24%, while Concentrates dropped 60.48%; month over month, Concentrates slid 24.77% and Pre-Roll decreased 20.11% versus a 14.25% pullback in Flower. Vapor Pens saw a 99.58% year-over-year fall and a 76.00% month-over-month decline, and Edible was down 35.85% month over month with no year-over-year read. With brand-wide sales down 62.29% year over year and an average price up 1.18%, the pattern implies Lula's is consolidating around Flower as relatively less negative MoM pressure there reshapes the portfolio toward lower volatility anchors.

Positioning now tilts toward core inhalables with Flower’s 55.95% share and a smaller but more elastic Concentrates base at 28.66%, while the collapse in Vapor Pens to 0.16% and the 20.11% month-over-month drop in Pre-Roll signal retreat from convenience-driven formats. The 14.25% month-over-month decline in Flower versus a steeper 24.77% in Concentrates indicates Lula's pricing and assortment are carrying more defensible demand in Flower despite a 54.44% year-over-year contraction, and the 1.18% brand-wide average price increase alongside a 62.29% sales decline points to mix-up within Flower toward higher-priced units. This mix and price posture implies Lula's near-term positioning is as a Flower-led operator in Illinois with rank 37 in Flower, prioritizing depth over breadth as it deemphasizes low-share, high-churn formats.

Competitive Landscape

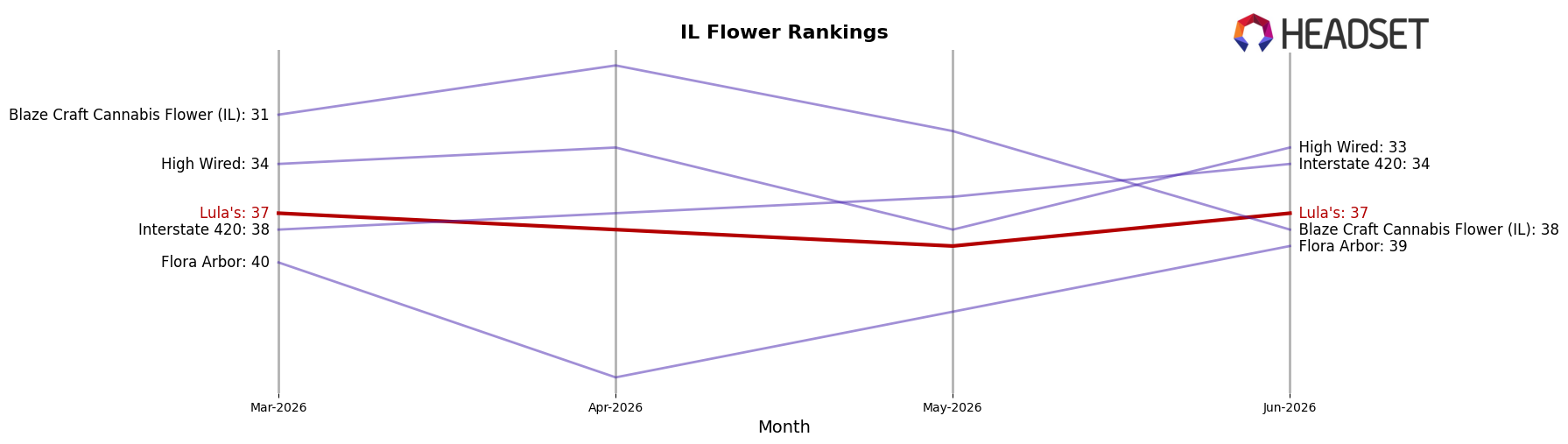

Lula's ranks #37 in Illinois Flower in June 2026, down 13 positions year over year from #24, and flat versus three months ago at #37; this contrasts with High Supply / Supply holding #1 with a 32.1% YoY sales increase while RYTHM stays at #2 despite a -5.2% YoY sales decline, and Good Green moving from #4 to #3 alongside 30.9% YoY growth. Compared with Lula's peak at #15 in August 2024, the -22 rank slide to #37 and the lack of quarter-on-quarter movement suggest share loss to incumbents, as &Shine advanced from #10 to #5 with 28.5% YoY growth while Simply Herb slipped from #3 to #4 with -16.8% YoY, implying Lula's current trajectory points to ongoing mid-tier displacement unless activation reverses the rank drift.

Notable Products

Lemon Cherry Garlic Pre-Roll (1g) posted the standout move in June 2026 with a +59.8% MoM surge to rank 2, while Doobie - Pink Drink Pre-Roll (1g) slid -14.7% to rank 4. Platinum Strawberries Pre-Roll (1g) held rank 1 as the category anchor, and with four of the top ten being Pre-Roll SKUs, the lineup tilts toward inhalables over edibles and flower. Jumbo Gem- Strawberry Lemonade Gummy (50mg) fell -35.8% at rank 10 against rising Pre-Roll momentum, reinforcing a shift in mix toward fast-turn Pre-Roll formats.

Mamba Marker Cured Sugar (1g) ranked 5 and Mac Stomper Cured Badder (1g) ranked 7, signaling concentrates stability even as edible share softens, with Strawberry Sunset Nuggies (14g) at rank 8 balancing flower presence at $16,960. The combined rank positions—1, 2, 3, and 4 occupied by Pre-Rolls—indicate merchandising and consumer pull are concentrating at the top of the chart, implying Lula's is consolidating demand around value-accessible pre-roll experiences.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.