Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

PAX is stocked at 735 licensed dispensaries across California, New York, and 11 other states, 303 of them in California, with the deepest coverage in Los Angeles, San Diego, San Francisco, Sacramento, and Fresno. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

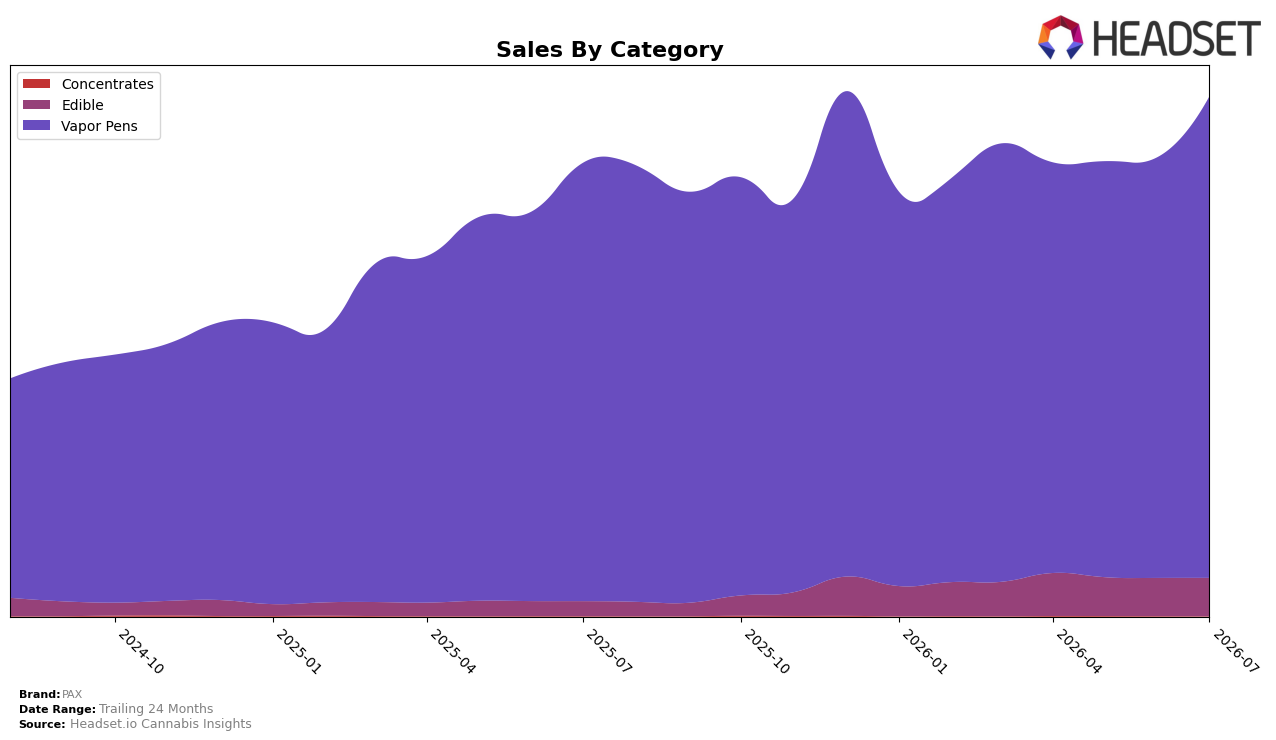

PAX concentrated 92.67% of July 2026 sales in Vapor Pens with a 14.38% month-over-month lift and 9.84% year-over-year growth, while Edible held 7.32% share with a 0.60% MoM uptick and 160.41% YoY surge; Concentrates fell to 0.01% share with an 80.96% MoM drop and 78.42% YoY decline. Average price fell 5.92% YoY to $39.91 even as total brand sales grew 14.66% YoY, and in Vapor Pens the brand sat at rank 2 in Colorado; together these shifts imply PAX is using lower prices to accelerate Vapor Pen volume while selectively scaling Edible as a secondary growth pillar.

The 92.67% Vapor Pen mix alongside a 160.41% YoY rise in Edible suggests deliberate category barbell positioning: defending a rank-2 Vapor Pen slot in Colorado with a 14.38% MoM push, while incubating Edible to diversify revenue without diluting the core. With overall sales up 14.66% YoY and average prices down 5.92% YoY, the pattern implies PAX is trading margin for share in Vapor Pens to maintain rank while allocating incremental gains from Edible’s 7.32% share to hedge against further Concentrates contraction of 80.96% MoM and 78.42% YoY.

Competitive Landscape

PAX sits at rank #2 in Colorado Vapor Pens in July 2026, improving 1 spot YoY from #3, while holding #2 over the last three months but off its March 2026 peak at #1; in contrast, Spherex maintained #1 YoY with a 7.2% sales lift and Batch Extracts moved from #4 to #3 alongside a 61.5% YoY increase, indicating that PAX’s slight rank gain amid faster-rising rivals implies a stable incumbent position that risks erosion if conversion or assortment velocity does not outpace challenger growth.

Notable Products

Wild Strawberry Live Rosin Gummies 10-Pack (100mg) posted the steepest shift in July 2026 with a -12.1% month-over-month drop as it slid to rank 9, while Trip - Blue Dream Fresh Pressed Live Rosin Diamonds Disposable Pax Era Pod (1g) rose 18.5% to hold rank 1. Trip - Maui Wowie Live Resin Diamonds Disposable Pax Era Pod (1g) in rank 2 gained 5.6% MoM, versus Trip - Northern Lights Live Rosin Diamonds Disposable Pax Era Pod (1g) at rank 3 easing -1.3%, and six of the top ten were Vapor Pens rather than Edibles. Raspberry Lime Live Rosin Gummies 10-Pack (100mg) advanced 8.4% at rank 4 even as Edibles concentration was four SKUs in the top ten, implying gummies are fragmenting while Era Pod-led Vapor Pens consolidate mix around a few leaders.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.