Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

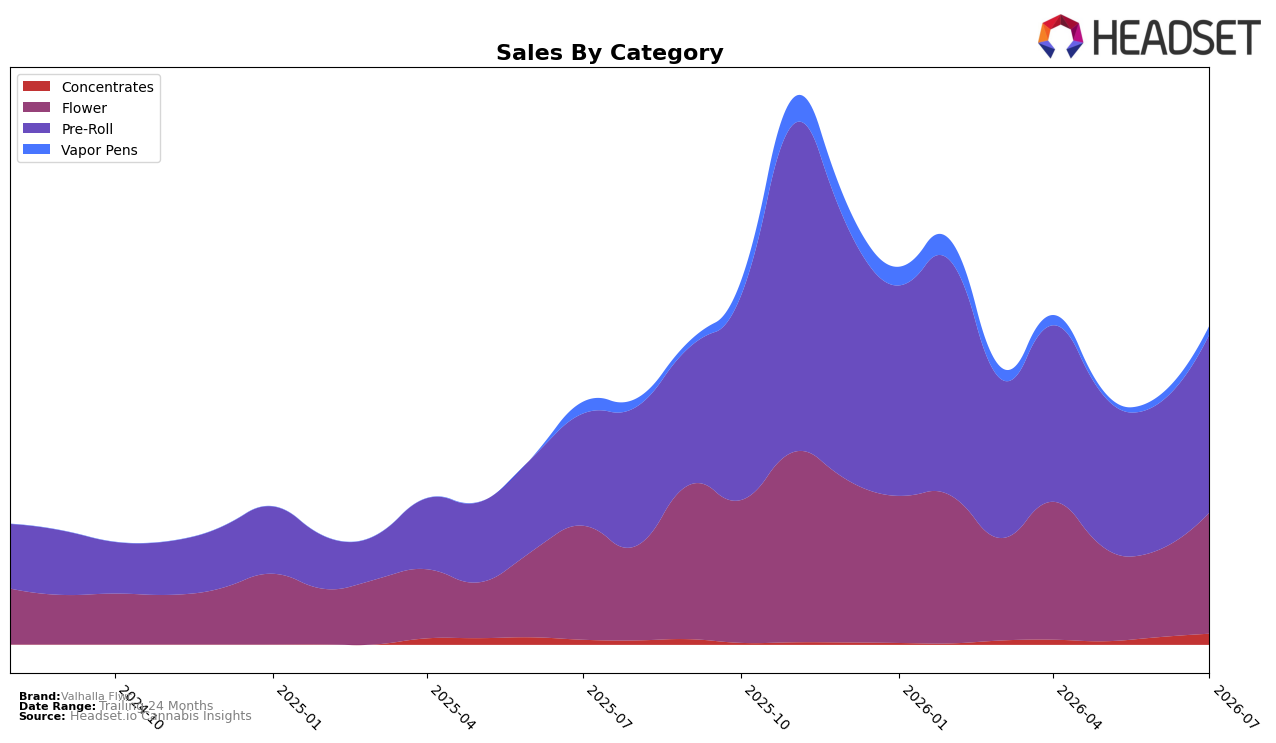

In July 2026, Valhalla Flwr’s mix concentrated in Pre-Roll at 55.92% share with year-over-year growth of 58.90% and month-over-month growth of 21.89%, while Flower held 37.99% share with 6.33% YoY and 39.43% MoM. Smaller lines shifted faster: Concentrates at 3.41% share jumped 125.58% YoY and 47.81% MoM, whereas Vapor Pens at 2.68% share fell 26.09% YoY despite a 20.56% MoM lift. With average price down 18.51% YoY to $28.93 alongside overall brand sales up 31.48% YoY, the pattern implies mix-driven unit expansion anchored in Pre-Roll and opportunistic gains in Concentrates are offsetting structural pressure in Vapor Pens.

The category tilt implies Valhalla Flwr is positioning as a value-forward Pre-Roll and Flower player in British Columbia, using double-digit MoM uplifts in Flower (39.43%) and Pre-Roll (21.89%) to consolidate share while sacrificing price to accelerate velocity. The outsized YoY surge in Concentrates (125.58%) with only 3.41% share indicates a test-and-scale runway, whereas the 26.09% YoY decline in Vapor Pens signals deprioritization or weaker resonance; together with a Pre-Roll category rank of 14 in British Columbia, the mix suggests the near-term path to rank gains is deeper penetration in Pre-Roll and targeted Concentrates expansion rather than reviving Vapor Pens.

Competitive Landscape

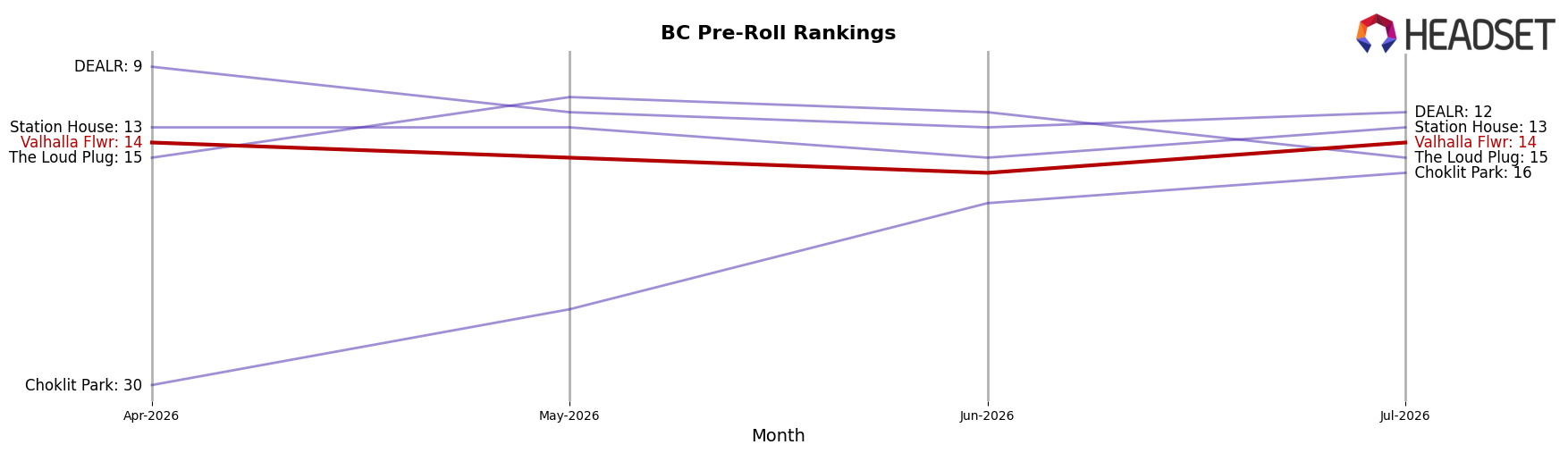

Valhalla Flwr sits at rank #14 in BC Pre-Roll in July 2026, improving 8 positions year over year from #22, while holding flat from April 2026 at #14; the brand peaked at #1 in October 2025, marking a 13-rank slide from that high. In contrast, General Admission maintained #1 year over year with a -22.3% YoY sales change, and Back Forty / Back 40 Cannabis rose from #17 to #2 alongside a 215.2% YoY sales increase, indicating that Valhalla Flwr’s rebound from #22 to #14 is outpaced by rivals moving faster up the leaderboard. The trajectory implies stabilization in the mid-teens rather than a return to the October 2025 #1 peak unless relative momentum versus top-five climbers accelerates.

Notable Products

Cosmic Cherry Pre-Roll (1g) posted the largest month-over-month gain at 75.1% and held rank 3, while Twisted Trio Variety Pack Pre-Roll 3-Pack (1.5g) climbed 56.2% to rank 5. Rainbow Lava Pre-Roll 3-Pack (1.5g) remained at rank 1 with 21.5% growth and the only disclosed raw dollar figure at $120,138, whereas Pebble Punch Pre-Roll 3-Pack (1.5g) in rank 2 inched up just 2.8%. With eight of the top ten occupied by Pre-Rolls and two Cosmic Cherry formats sitting inside the top 7, the mix indicates a deliberate tilt toward format depth in Pre-Rolls and strain-line extensions over breadth expansion into other categories.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.