Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

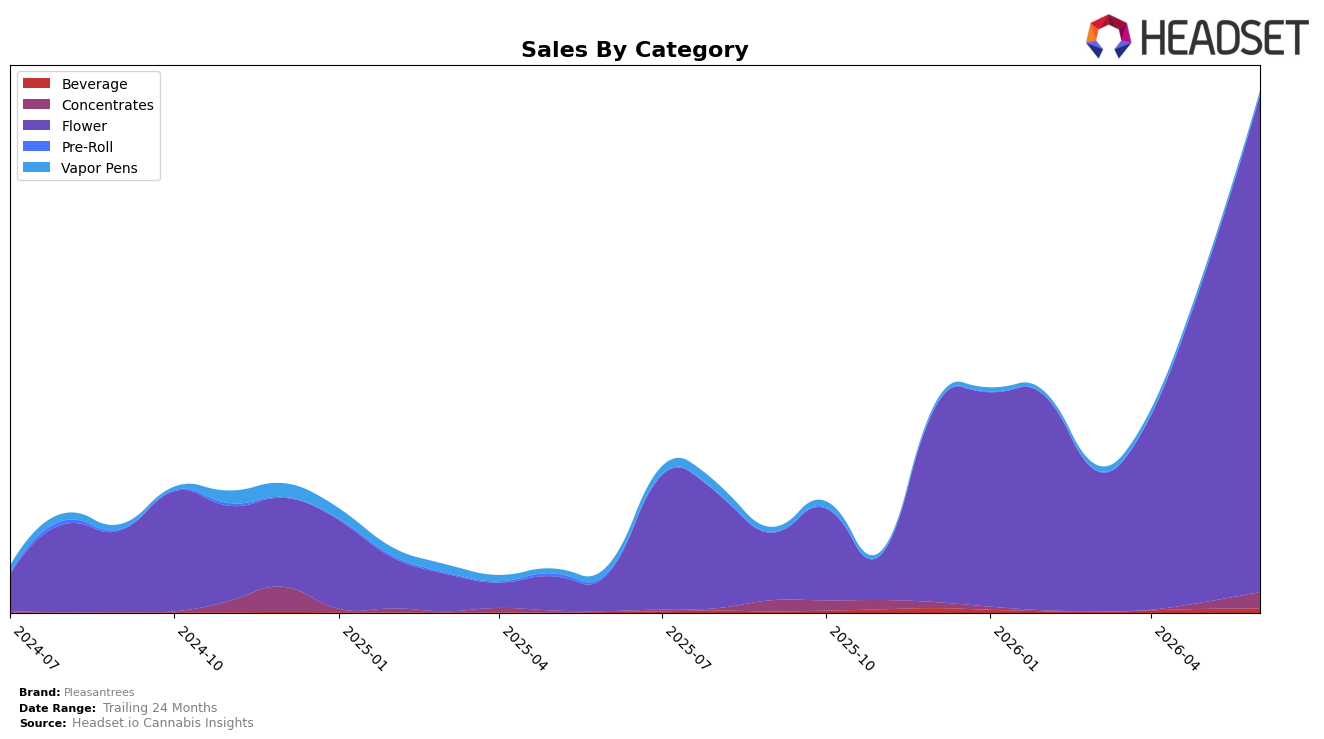

Pleasantrees concentrated 95.47% of June 2026 sales in Flower, up 51.70% month over month and 1,230.89% year over year, while rank in Flower stood at 32 in Michigan. Secondary bets shifted: Concentrates held 3.10% share with a 151.42% month-over-month surge and 3,706.52% year-over-year growth, while Vapor Pens contracted to 0.67% share with an 18.66% month-over-month decline and a 43.11% year-over-year drop. Beverage remained a niche at 0.75% share with 2.82% month-over-month growth and 492.13% year-over-year growth. Average price fell 3.40% year over year to $23.93, while Flower’s average price sat higher at $24.36; the pattern implies volume-led gains anchored in Flower, with Concentrates emerging as a volatile but expanding add-on and Vapor Pens shedding relevance.

The divergence—Flower up 51.70% month over month while Vapor Pens down 18.66% month over month—suggests merchandising and consumer trade-down concentrated towards inhalables with simpler value cues, supported by a 3.40% brand-wide price deflation. With Concentrates up 151.42% month over month but still just 3.10% share, and Beverage inching 2.82% month over month at 0.75% share, Pleasantrees is positioned as a Flower-first player using selective depth in Concentrates to capture potency-driven shoppers while ceding lighter-use occasions in Vapor Pens; this mix, combined with a 32 rank in Michigan Flower, implies near-term share wins depend on sustaining Flower volume while carefully scaling Concentrates without diluting price architecture.

Competitive Landscape

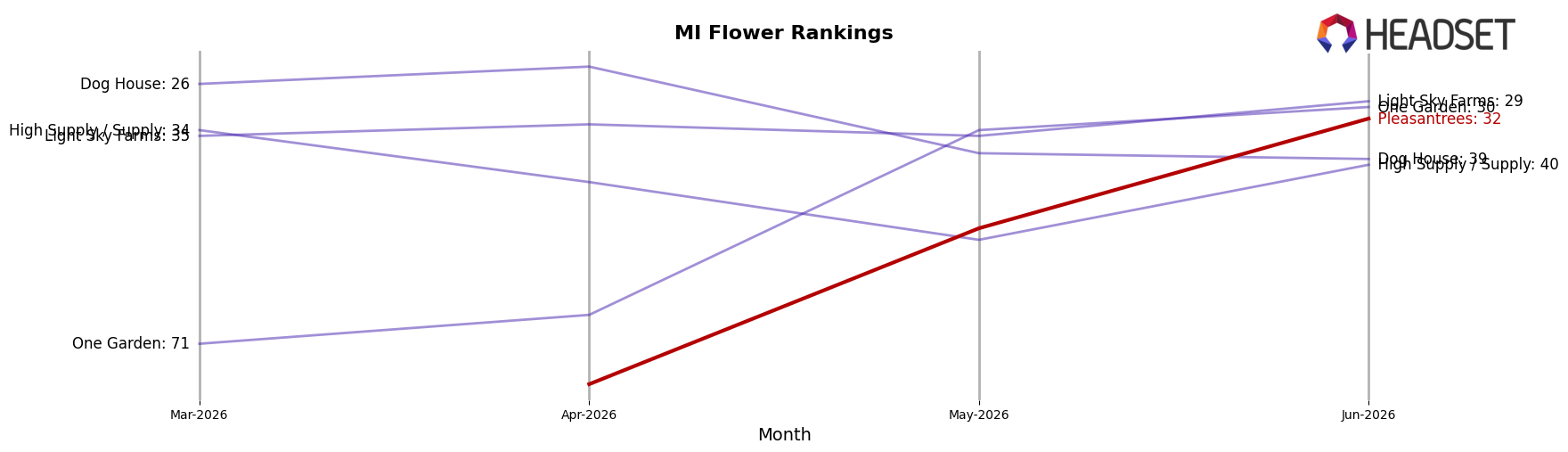

Pleasantrees is ranked #32 in MI Flower in June 2026, up 196 positions from #228 year over year and up 76 positions from #108 in March 2026, marking its peak rank to date at #32; against this backdrop, High Minded held #1 with a 0-position YoY change despite a 13.7% YoY sales decline, while Goodlyfe Farms advanced to #2 from #5 alongside a 44.1% YoY sales increase, indicating Pleasantrees’ late-entry surge is occurring amid leaders that are either consolidating at the top or accelerating from mid-pack, and the trajectory implies Pleasantrees is transitioning from fringe presence to competitive relevance if it can convert rapid rank gains into sustained top-30 stability.

Notable Products

Blue Zushi (3.5g) leads June 2026 at rank 1 while nine of the top ten are Flower SKUs, concentrating over 90% of the visible leaderboard in a single category, which indicates Pleasantrees is leaning into Flower dominance rather than diversifying formats. Runtz (Bulk) holds rank 2 and Cereal Killa (Bulk) sits at rank 3, and the tie at rank 7 between Gazzurple (Bulk) and Truffle Cake (Bulk) signals a crowded mid-tier that may compress margins as adjacent SKUs compete for similar share. With Zlushiez (Bulk) at rank 8 and Crip'd Keeper (Bulk) at rank 9, the back half shows tighter clustering by rank positions than the top three, implying velocity skews to a few leaders while the rest fragment demand. The mix points to a strategy where premium Flower like Blue Zushi anchors traffic and A-run bulk strains shoulder volume, suggesting Pleasantrees is prioritizing depth within Flower over breadth across categories to sustain basket size and simplify inventory turns.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.