Market Insights Snapshot

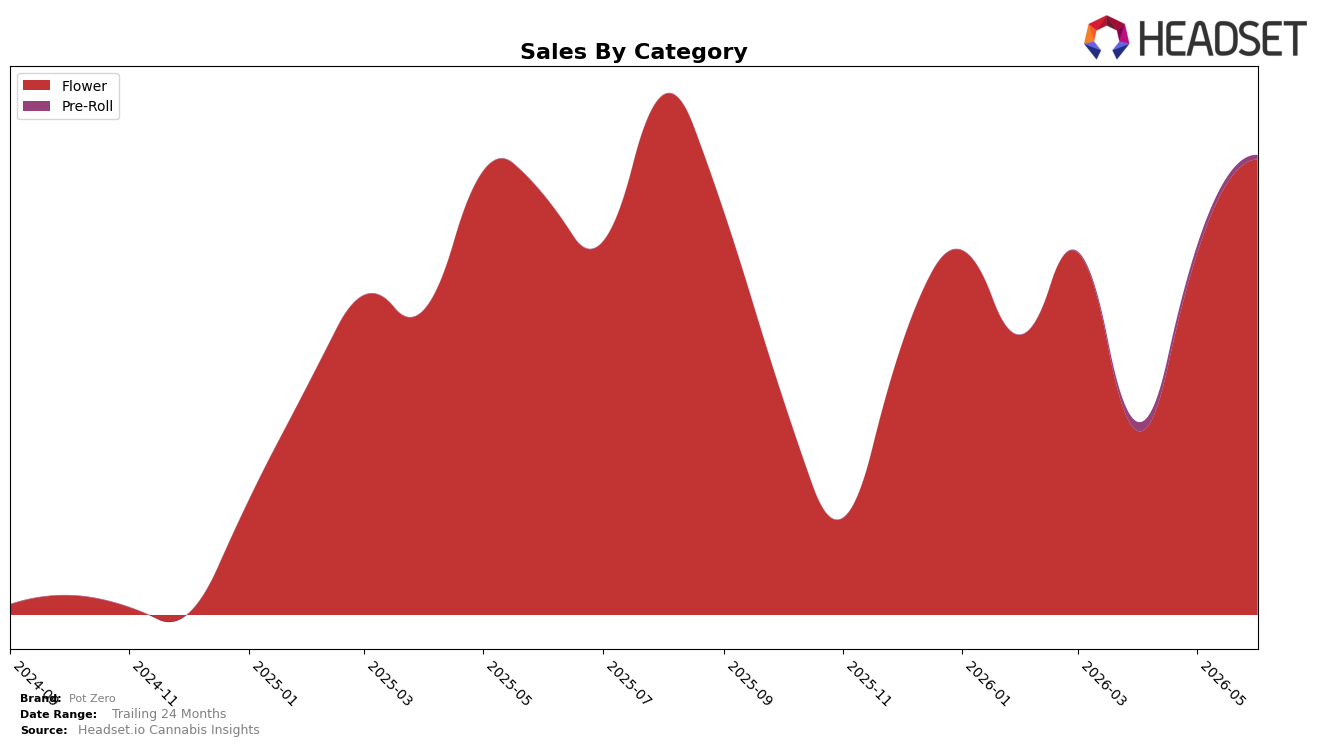

In June 2026, Pot Zero’s mix was overwhelmingly Flower at 99.12% share with Pre-Roll at 0.88% share, and Flower sales rose 8.54% year over year while jumping 26.19% month over month; by contrast, Pre-Roll fell 48.01% month over month and had no reported year-over-year comp. The average price across the brand declined 54.01% year over year to $21.20, while Flower’s average price sat at $21.15 versus $27.32 in Pre-Roll, and the brand ranked 21 in Flower in Colorado. The pattern implies Pot Zero is consolidating around Flower volume growth and price-led accessibility, with Pre-Roll acting as a small, volatile edge case rather than a growth pillar.

The 26.19% month-over-month surge in Flower alongside a 99.12% category share and a 54.01% year-over-year brand-wide price drop indicates a deliberate price-to-volume trade that prioritizes rank stability at 21 over breadth. With Pre-Roll shrinking 48.01% month over month and holding just 0.88% share while Flower carries 8.54% year-over-year growth, the portfolio tilt implies a positioning anchored in core Flower velocity rather than diversification, aiming to convert lower price points into sustained share defense in Colorado and to signal that experimentation outside Flower will remain opportunistic rather than scaled.

Competitive Landscape

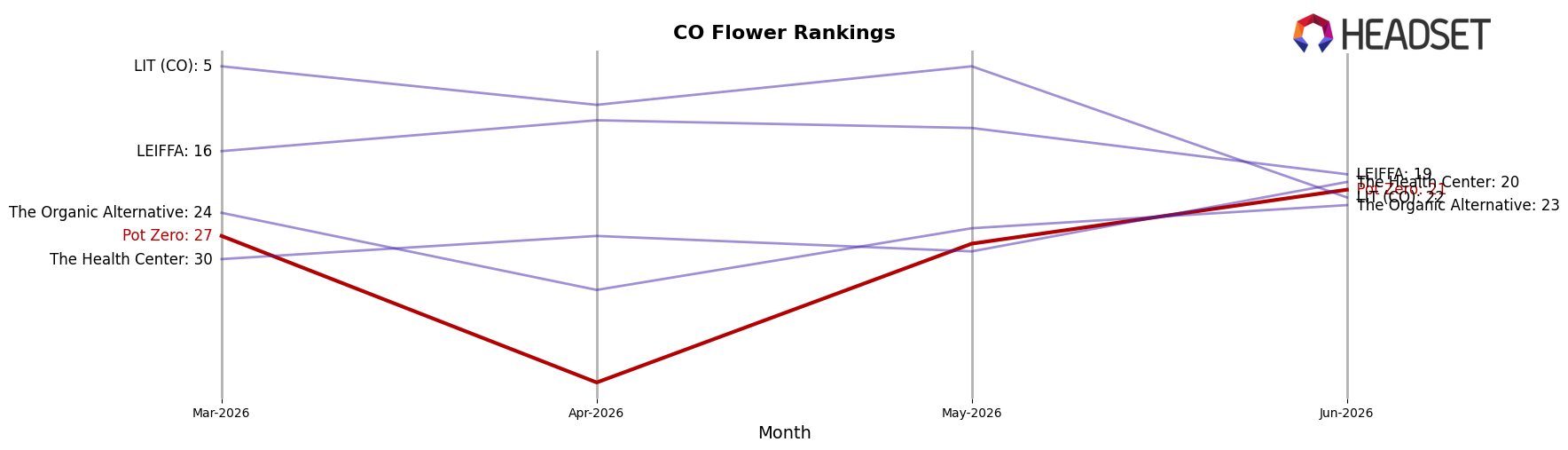

Pot Zero sits at rank #21 in Colorado Flower for June 2026, down 1 place year over year from #20, but up 6 places from March 2026’s #27, while still trailing its peak of #16 from August 2025; in contrast, Seed & Strain Cannabis Co. moved from #2 to #1 with 62.8% YoY sales growth and Natty Rems surged from #28 to #5 with 221.0% YoY growth, indicating that the competitive set is consolidating at the top. Against this backdrop, Good Chemistry Nurseries slipped from #1 to #3 with a -2.8% YoY sales change while Green Dot Labs held steady at #4 with 4.1% YoY growth, suggesting that Pot Zero’s modest YoY rank decline of 1 place coupled with a 6-place climb since March 2026 points to mid-pack volatility where incremental gains are achievable but require outpacing rapidly ascending peers.

Notable Products

Gush Mints (1g) posted the standout move in June 2026 with a +324.9% month-over-month surge to rank 2, while Huckleberry (1g) fell 30.0% and slipped to rank 4; this divergence implies volatility in single-gram demand even within the same category. Avalon (1g) climbed 68.7% to rank 1, edging past faster-growing but smaller Gush Mints (1g), indicating that velocity gains are pairing with scale at the very top. Five of the top ten are Popcorn 14g SKUs concentrated between ranks 5–10, and Hybrid Popcorn (14g) rose 11.1% at rank 6 while Avalon Popcorn (14g) anchored the segment with $25,518 in June 2026 sales; this concentration suggests Pot Zero is leaning toward value-size Flower as a volume moat while using 1g spikes to capture incremental trial.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.