Market Insights Snapshot

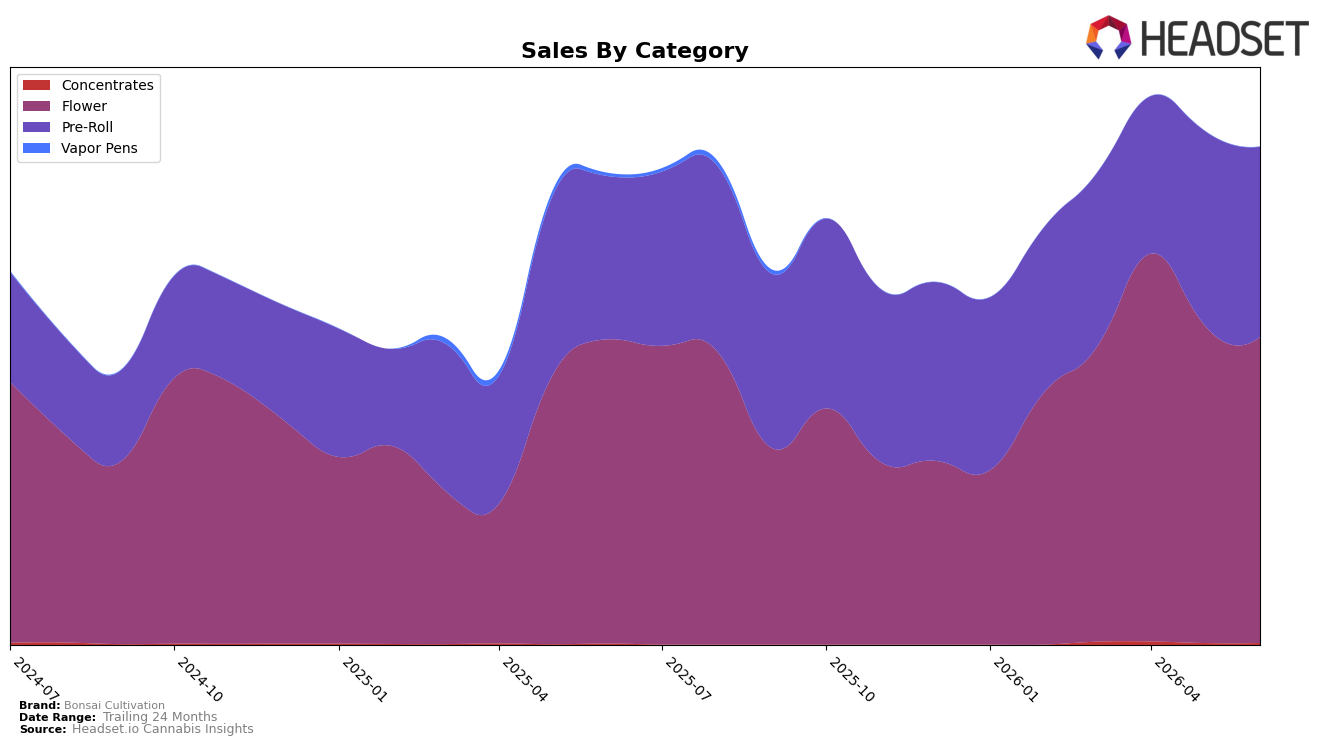

In June 2026, Bonsai Cultivation’s mix tilted toward Flower at 61.47% share while Pre-Roll held 38.21% and Concentrates remained a sliver at 0.32%. Flower volume softened month over month at -3.73% despite a marginal 0.54% year-over-year gain, whereas Pre-Roll advanced 16.67% year over year but dipped -2.13% month over month; Concentrates grew 2.69% month over month and 63.06% year over year from a small base. With average prices up 9.29% year over year alongside a brand-level sales increase of 5.62% year over year, the mix shift implies that price lift is offsetting volume pressure in Flower while Pre-Roll’s faster year-over-year growth is narrowing the gap, signaling a gradual diversification away from a single-category dependency.

The current ranking context in Colorado Flower at rank 10, paired with a 61.47% share concentration in Flower and concurrent -3.73% month-over-month Flower change, suggests Bonsai Cultivation is less insulated from rank volatility than a more balanced mix would be. Pre-Roll’s 16.67% year-over-year growth and 38.21% share, against a -2.13% month-over-month dip, indicate that near-term softness did not derail a category that is contributing a larger portion of annual growth; combined with Concentrates’ 63.06% year-over-year surge but just 0.32% share, the pattern implies the brand’s positioning hinges on stabilizing Flower while using Pre-Roll momentum to defend rank and gradually test higher-margin niches without overexposing the portfolio.

Competitive Landscape

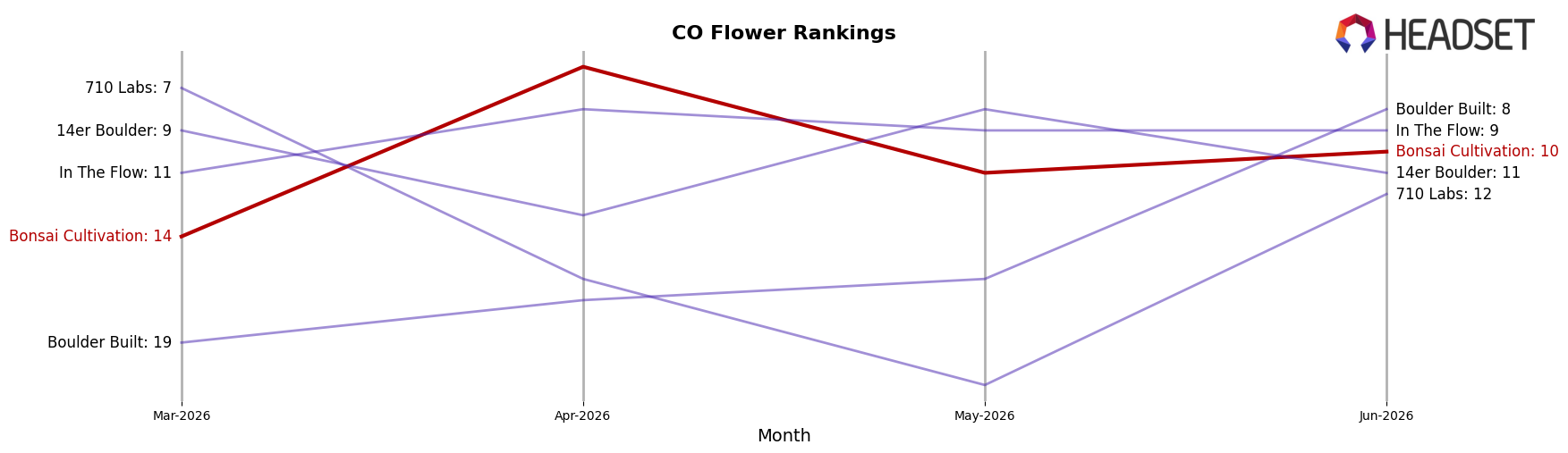

Bonsai Cultivation sits at rank #10 in June 2026 in CO Flower, down 2 positions year over year from #8, but up 4 spots since March 2026 when it was #14; by contrast, Seed & Strain Cannabis Co. moved up from #2 to #1 with a 62.8% YoY sales lift while Natty Rems surged from #28 to #5 on 221.0% YoY growth, and Good Chemistry Nurseries slipped from #1 to #3 alongside a 2.8% YoY sales decline; given Bonsai Cultivation’s fall from its April 2026 peak rank of #6 to #10 and the simultaneous upward mobility of faster-rising peers, the trajectory implies share preservation will require a pivot toward velocity drivers rather than relying on short-lived spikes.

Notable Products

Relaxation Pre-Roll (1g) posted the steepest decline in June 2026 at -12.8% MoM and slid to rank 3, while Energy Pre-Roll 2-Pack (1g) dropped -19.0% MoM at rank 4, indicating erosion within multipack and down-listing single formats. Energy Pre-Roll (1g) still leads at rank 1 with +22.9% MoM and $112,597, and Creativity Pre-Roll (1g) surged +154.9% MoM to rank 2, but four of the top ten are Pre-Roll SKUs, concentrating exposure in a single format despite mixed momentum. The split between a +154.9% riser at rank 2 and dual declines of -12.8% and -19.0% in ranks 3–4 implies volatility within the pre-roll portfolio rather than broad category lift. This pattern suggests Bonsai Cultivation’s commercial direction is leaning heavier into flagship single-stick pre-rolls while multipacks and secondary strains require repositioning to stabilize share.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.