Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Redwood is stocked at 30 licensed dispensaries across Nevada, with the deepest coverage in Las Vegas, Henderson, North Las Vegas, Reno, and Carson City. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

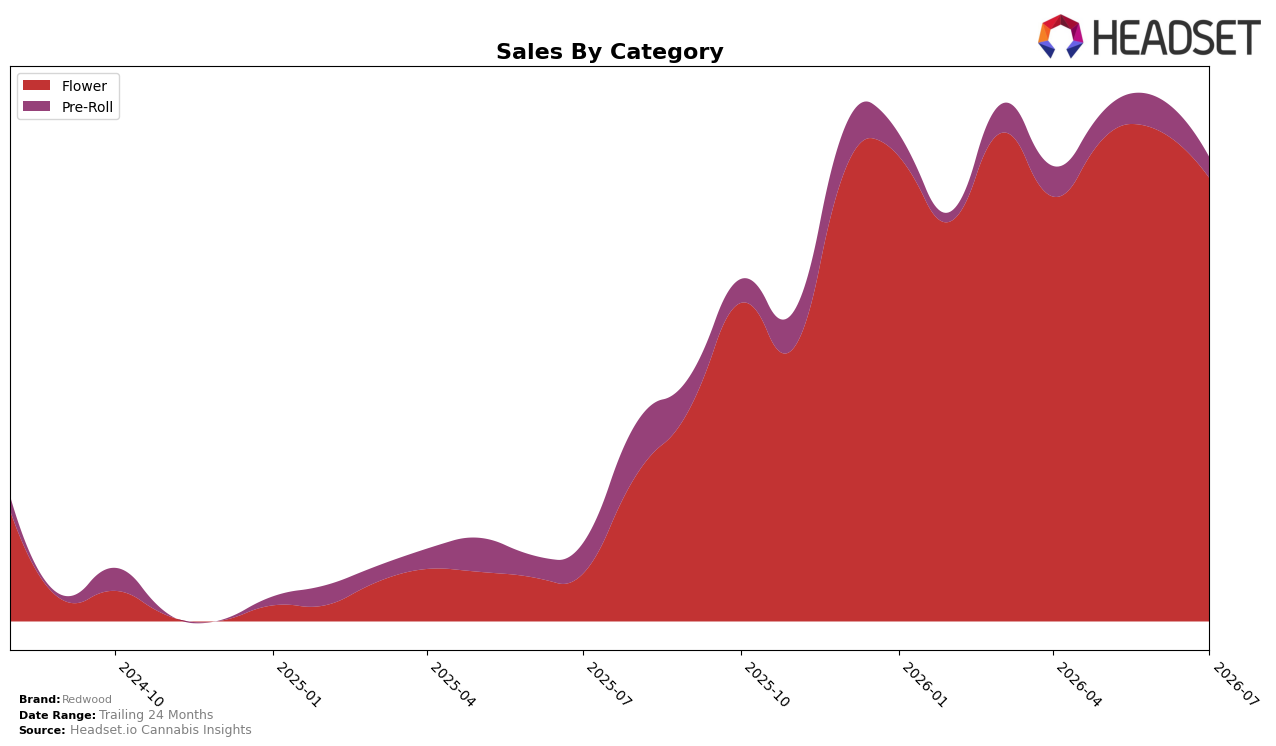

In July 2026, Redwood concentrated 95.59% of sales in Flower, while Pre-Roll accounted for 4.41%, indicating a sharper tilt than in typical mixed portfolios. Flower expanded 832.45% year over year but slipped 9.76% month over month, whereas Pre-Roll contracted 32.44% year over year and 36.69% month over month, a divergence that widens the reliance gap between the two categories. With overall brand sales up 495.72% year over year and average price up 13.60%, the mix shift implies volume-led gains centered in Flower despite short-term pullback, signaling that July 2026 momentum was anchored in a single category rather than balanced growth.

Holding Flower share above 95% while sitting at rank 7 in Flower within Nevada positions Redwood as a high-exposure specialist rather than a hedge-through-portfolio player, with the 9.76% month-over-month dip suggesting sensitivity to Flower seasonality or shelf dynamics. The 36.69% month-over-month decline in Pre-Roll alongside a 32.44% year-over-year drop reduces cross-category insulation, while the 13.60% increase in average price against an 832.45% Flower year-over-year surge implies pricing power sustained by velocity rather than SKU breadth. The pattern points to a strategy where maintaining top-10 Flower standing depends on stabilizing month-over-month Flower trends and selectively rebuilding Pre-Roll to diversify risk without diluting Flower focus.

Competitive Landscape

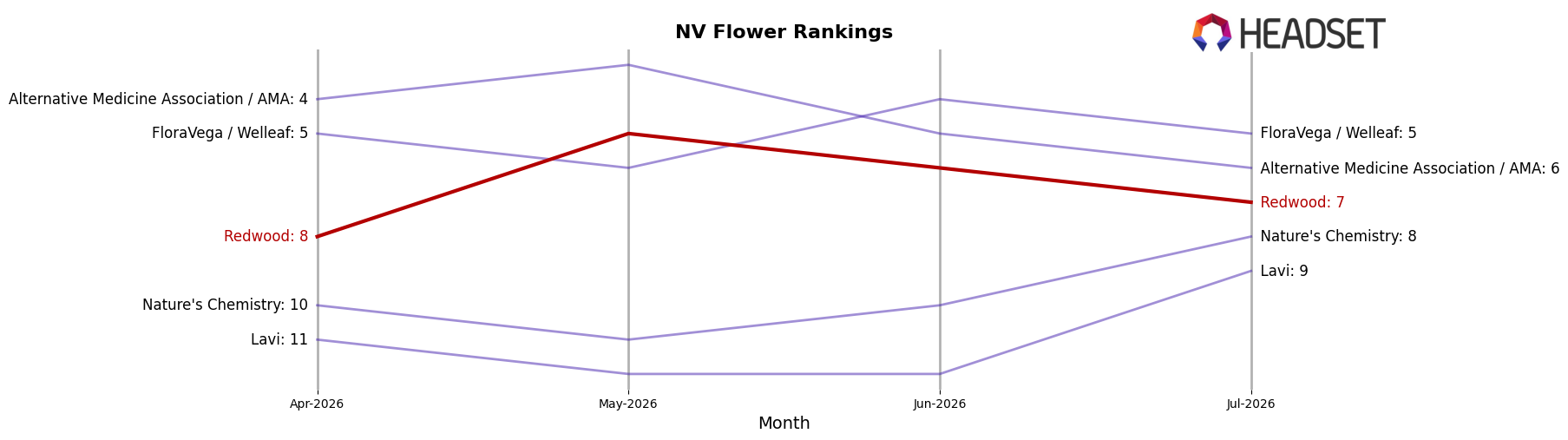

Redwood is currently ranked #7 in NV Flower in July 2026, a year-over-year climb of 48 positions from #55, and it improved 1 spot from #8 three months earlier while coming off a peak of #5 in May 2026; meanwhile, STIIIZY advanced from #2 to #1 with 31.5% YoY sales growth and RYTHM slipped from #1 to #2 with a 12.7% YoY decline, indicating Redwood’s rise is occurring amid both upward and downward competitor movements. With Neon Moon moving from #10 to #3 and FloraVega / Welleaf jumping from #24 to #5 alongside a 299.7% YoY sales increase, Redwood’s shift from #55 to #7 suggests momentum but also signals a crowded chase pack where maintaining a top-10 foothold will require outpacing fast climbers rather than merely recovering rank.

Notable Products

Grape Gasoline (3.5g) led July 2026 with a 379% month-over-month surge to $135,547 and jumped to rank 1, while Flat White (3.5g) followed with a 140% MoM increase at rank 2. Tangerine Skunk (3.5g) moved the other way with a -47.8% MoM decline at rank 7, creating a wide spread between the leaders and mid-pack. With eight of the top ten SKUs in the Flower category, the outsized gains at ranks 1 and 2 alongside a mid-tier contraction imply Redwood is concentrating demand into a few hero Flower strains while pruning or deprioritizing trailing SKUs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.