Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

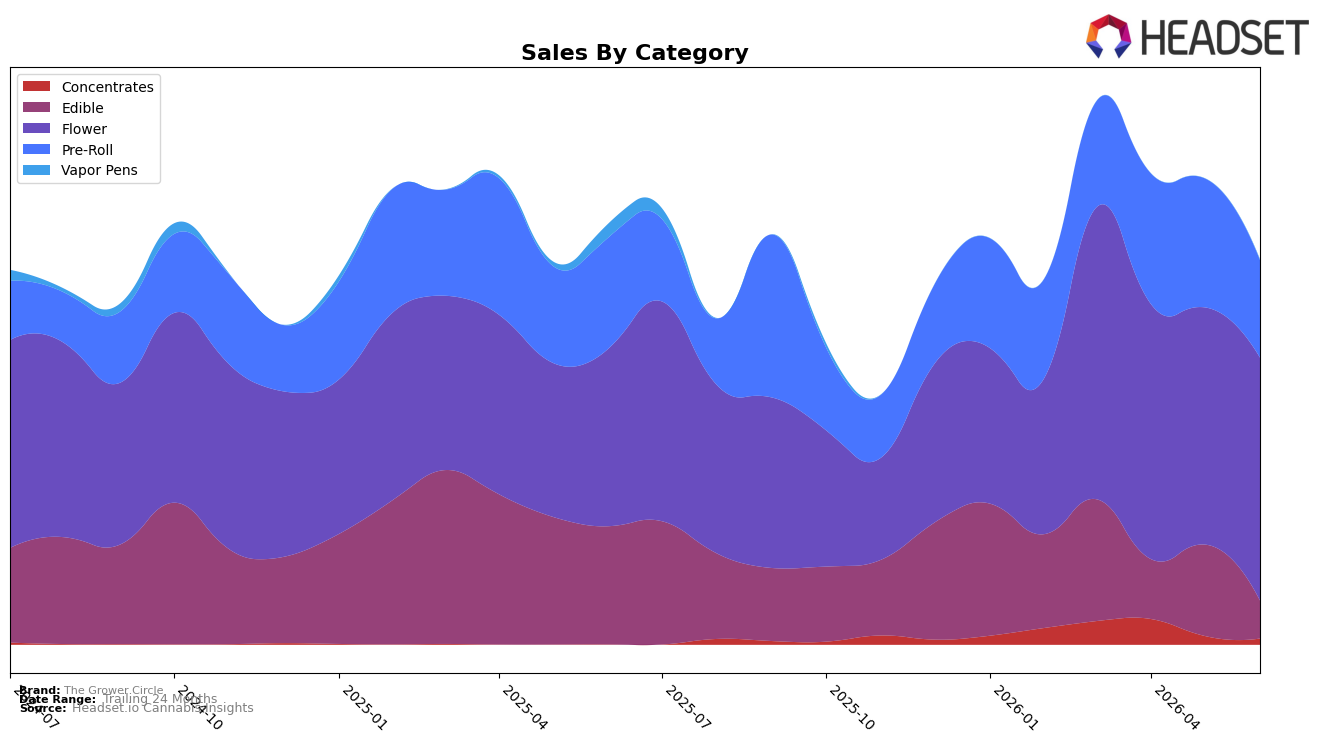

In June 2026, The Grower Circle’s mix concentrated further into Flower at 63.13% share, with Flower sales up 36.94% year over year and 2.39% month over month, while Pre-Roll retreated to 25.31% share on a 12.31% YoY decline and a 24.48% MoM drop. Edible contracted to 9.81% share with sales down 68.04% YoY and 58.60% MoM, and Concentrates, though only 1.57% share, posted a 9,253.47% YoY surge alongside a 30.12% MoM pullback. Vapor Pens fell to 0.18% share with a 94.96% YoY decline and no reported MoM figure. The pattern implies the brand is pivoting toward Flower-driven volume in Nevada while rapidly de-emphasizing Edible and Vapor Pens, using Concentrates as a small but volatile adjunct.

Positioning-wise, the heavier Flower weighting and price elasticity (average price down 12.03% YoY to $22.96 alongside 36.94% Flower YoY growth) signal a value-led push in its core category, whereas the 24.48% MoM contraction in Pre-Roll and 58.60% MoM contraction in Edible indicate pruning of lower-yield or less differentiated lines. With Flower ranked 21st in Nevada and only 0.18% share in Vapor Pens amid a 94.96% YoY decline, the brand’s near-term differentiation rests on deepening Flower penetration and selectively nurturing Concentrates despite its 30.12% MoM volatility. The implication is a deliberate narrowing toward categories where price moves can trade share efficiently, accepting rank pressure outside Flower to defend and improve its position at rank 21 within the state’s Flower set.

Competitive Landscape

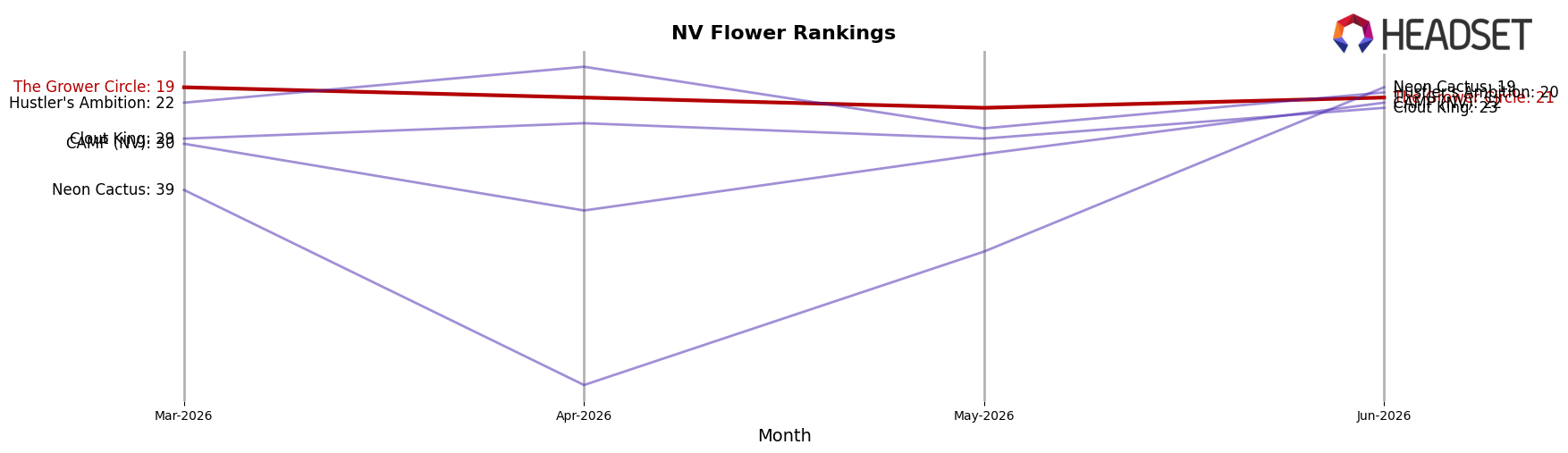

The Grower Circle sits at rank #21 in NV Flower in June 2026, improving 10 positions from #31 year over year, but down 2 spots from #19 in March 2026, signaling a mixed trajectory where recovery outpaces recent slippage. Against this backdrop, STIIIZY held #1 with a 5.17% YoY sales increase while RYTHM moved up to #2 from #4 despite a -6.87% YoY decline, and FloraVega / Welleaf surged to #3 from #22 with 260.35% YoY growth, indicating that upward rank mobility is achievable even amid contraction for some players. The Grower Circle’s climb of 10 ranks YoY alongside a 2-rank drop since March 2026 implies the brand is gaining baseline competitiveness but must convert sporadic peaks into sustained share capture as volatility at the top intensifies.

Notable Products

Waffle Cone (3.5g) posted the sharpest movement in June 2026 with a -37.3% month-over-month slide while dropping to rank 9, and StrawGuava Hash Rosin Infused Pre-Roll (1g) also contracted by -12.4% at rank 10; by contrast, Waffle Cone Pre-Roll (1g) in rank 4 eased only -2.6%. With Dulce (3.5g) at rank 1 and Jet Fuel Gelato (3.5g) at rank 2, six of the top ten are Flower SKUs, concentrating demand at the top despite the Waffle Cone decline; the rank spread between Flower leaders (ranks 1–3) and trailing Pre-Rolls (ranks 7–10) implies product-tier bifurcation. The skew toward premium Flower volume, including Dodie (3.5g) in rank 3, alongside mixed Pre-Roll momentum suggests The Grower Circle is leaning into Flower-led basket building while trimming exposure to underperforming infused variants; a single strong Flower anchor can carry revenue even as one sub-line retreats, with Dulce (3.5g) contributing $35,374.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.