Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

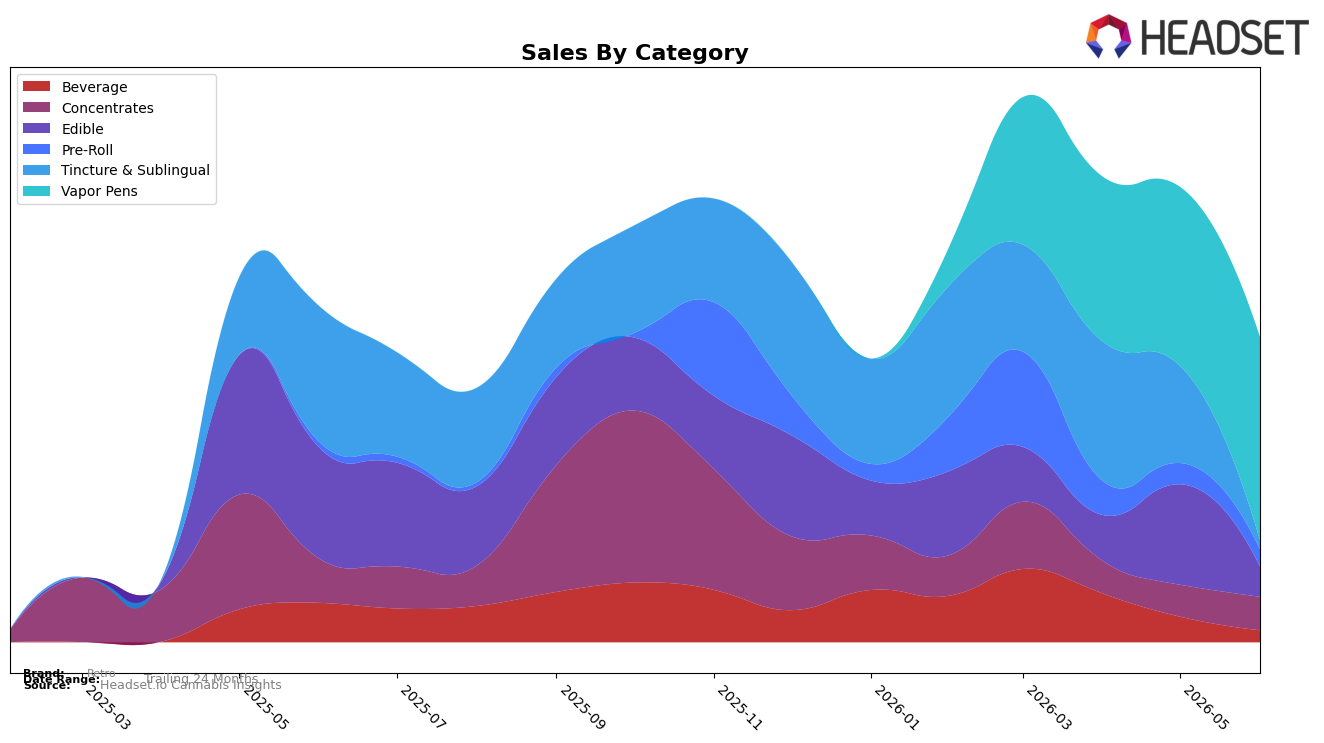

Retro concentrated 66.74% of June 2026 sales in Vapor Pens, up 13.50% month over month, while Pre-Roll held 5.59% share with a 19.06% MoM decline; at the edges, Beverage fell 53.25% MoM to 3.91% share and Tincture & Sublingual dropped 90.88% MoM to 2.91% share. Year over year, Pre-Roll expanded 205.54% and Concentrates contracted 24.17%, against brand-level sales down 9.25% YoY and an average price up 49.40%, implying Retro is leaning into higher-priced inhalables even as ingestible categories like Edible fell 72.86% YoY and Beverage fell 69.73% YoY. The pattern implies a deliberate shift toward Vapor Pens and selective Pre-Roll momentum to offset sharp ingestible retrenchment, concentrating mix where price tolerance is rising.

With Vapor Pens anchored as the top category and a rank of 83 in Alberta Vapor Pens, the 13.50% MoM lift alongside a 66.74% mix share suggests Retro is prioritizing penetration over breadth, while the 205.54% YoY growth in Pre-Roll amid a 19.06% MoM pullback indicates episodic wins rather than stable velocity. The simultaneous 72.86% YoY decline in Edible and 69.73% YoY decline in Beverage, coupled with a 49.40% increase in average price, implies Retro is trading consumers up within inhalables rather than defending value-led ingestibles, positioning the brand to compete on potency and device-driven formats rather than on low-price, low-velocity categories.

Competitive Landscape

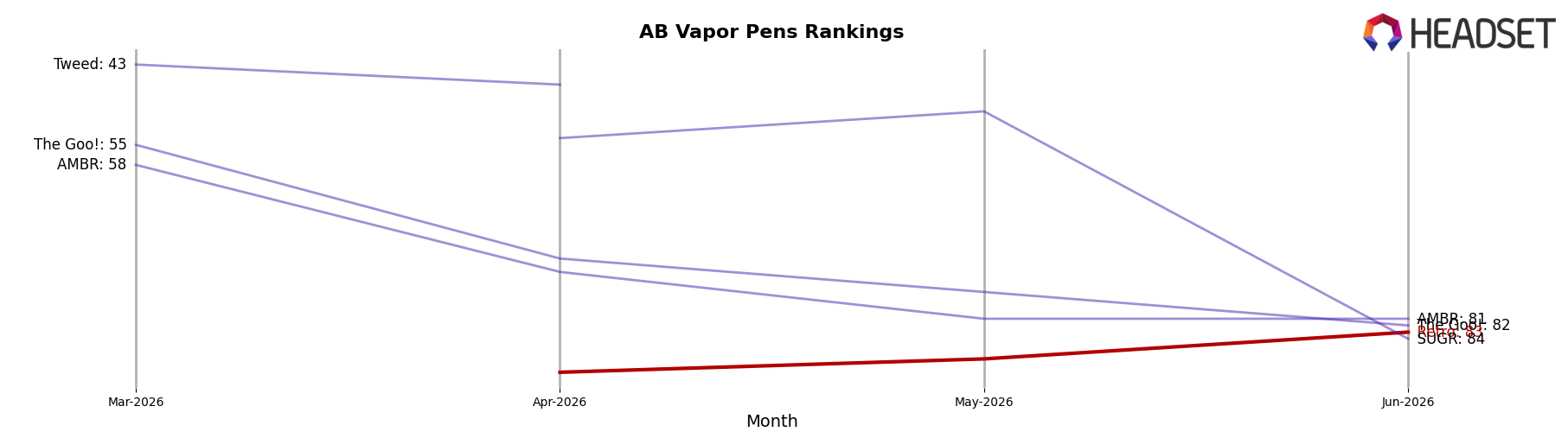

Retro is ranked #83 in AB Vapor Pens in June 2026, improving 8 positions from #91 in March 2026, while year-over-year rank data is unavailable and June 2026 marks its peak rank to date at #83; meanwhile, category leaders set a steep benchmark as Spinach holds #1 with a 43.97% YoY sales increase and Kolab moved from #8 to #4 with a 36.33% YoY lift, whereas General Admission slipped from #4 to #5 with a -14.82% YoY change, implying Retro’s recent rank gain is occurring in a tier where upward mobility is possible but sustained share capture will require closing a wide gap versus the top five.

Notable Products

Liquid Solventless Drop Tincture (100mg) posted the steepest decline in June 2026 at -90.9% MoM while sliding to rank 5, as Coffee & Donuts Milk Chocolate Bar (100mg) fell -92.0% MoM to rank 7. In contrast, Pink Kush Full Spectrum Honey Oil Cartridge (1g) rose +13.5% MoM and held rank 1, outpacing the broader set where Beverage SKUs at ranks 4, 6, 8, and 9 contracted between -39.1% and -74.4%. This pattern implies Retro’s demand is consolidating around a single Vapor Pens leader while peripheral formats shed velocity, signaling a portfolio tilt toward inhalable repeat-purchase behavior over niche form factors.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.