Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

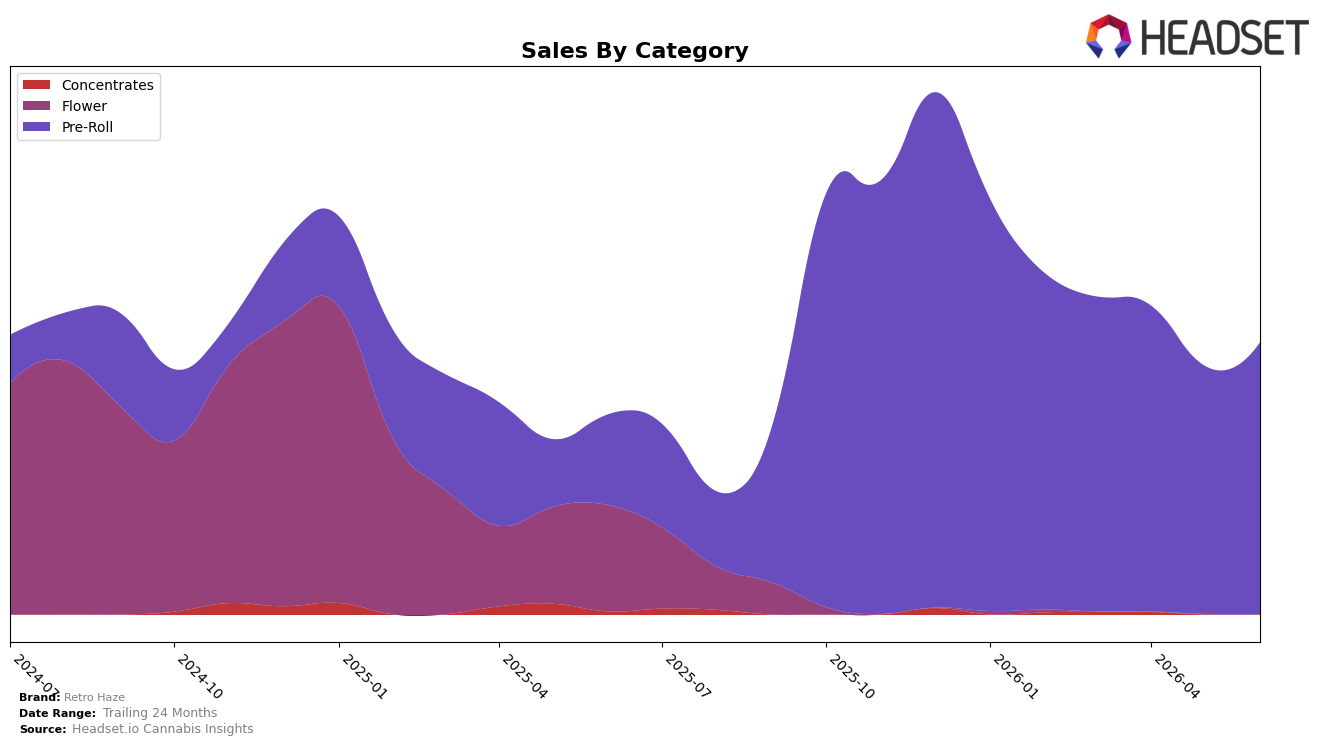

Retro Haze concentrated entirely in Pre-Roll during June 2026, with category mix at 100.0% share and a 9.4% month-over-month lift alongside a 200.3% year-over-year gain inside the segment. Despite a 56.4% year-over-year drop in average price to $13.81, brand sales grew 36.1% year over year, implying unit volume expansion outweighed price compression. With a Saskatchewan Pre-Roll rank at position 30 and a 48.7% two-year sales increase, the pattern implies the brand is trading down on price while leaning fully into a single-category footprint to capture incremental volume.

The full pivot to a 100.0% Pre-Roll mix, coupled with a 9.4% month-over-month rise and 200.3% year-over-year surge in that category, indicates a deliberate value-led positioning aimed at velocity over premium margin. Holding rank 30 in Saskatchewan while cutting average price by 56.4% and lifting sales 36.1% year over year suggests Retro Haze is prioritizing shelf throughput and basket entry, which could support near-term share capture but concentrates risk in one format.

Competitive Landscape

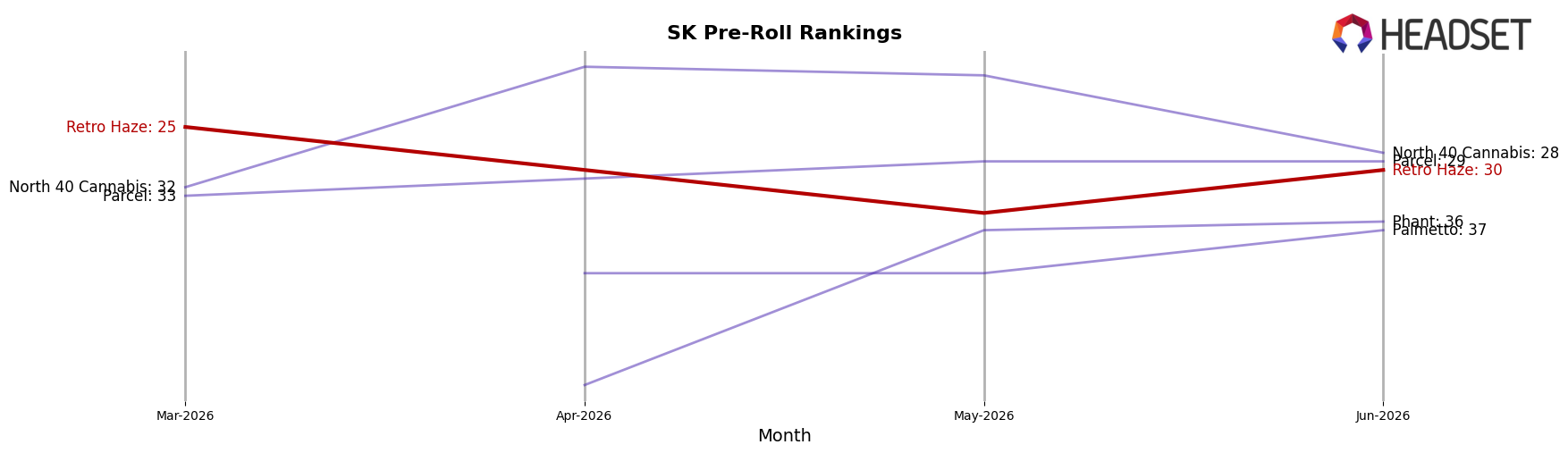

Retro Haze sits at rank #30 in SK Pre-Roll in June 2026, a YoY climb of 91 places from #121, while slipping 5 spots from #25 three months ago and 11 spots from its peak of #19 in December 2025; this mix of a 91-place annual jump and an 11-place decline from peak indicates momentum tempered by recent cooling. In contrast, Back Forty / Back 40 Cannabis held #1 YoY and remains #1 currently with sales up 134.2%, and Doobie Snacks climbed from #9 YoY to #3 with sales up 282.0%, outpacing Retro Haze’s rank trajectory both in current positioning and acceleration; the pattern implies Retro Haze’s surge is transitioning from breakout to consolidation, requiring share defense against faster risers at the top.

Notable Products

Jack Herer Pre-Roll 3-Pack (1.5g) led June 2026 with a +9.5% month-over-month lift at rank 1, while Jack Herer Pre-Roll 5-Pack (2.5g) inched up just +1.5% at rank 2. Two of the top ten are Pre-Roll SKUs from the Jack Herer line, indicating concentration at the top that could cap category breadth if growth stays limited to a single format. The absence of ranked or reported movement for Heritage Hash (2g) and Lemon Haze (3.5g) alongside a +9.5% gain at the flagship suggests the portfolio is over-indexed to Pre-Rolls rather than expanding into Concentrates or Flower. This pattern implies Retro Haze is consolidating around Pre-Rolls, prioritizing depth in one hero line over diversifying into adjacent categories.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.