Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

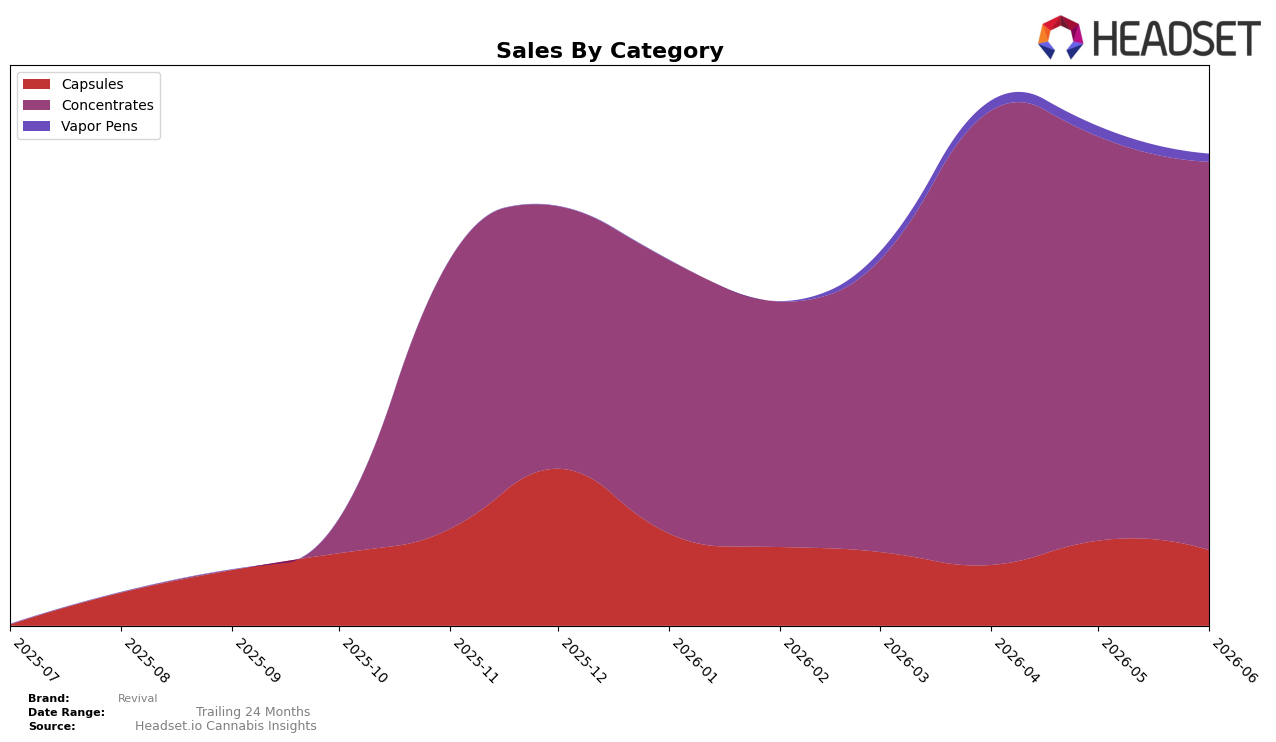

Revival concentrated 82.38% of June 2026 sales in Concentrates while Capsules held 15.97% and Vapor Pens 1.64%, indicating a tightly skewed mix toward a single category; within-month shifts leaned negative, with Concentrates down 3.88% MoM, Capsules down 11.27% MoM, and Vapor Pens down 22.59% MoM. In New York Concentrates, the brand sat at rank 34, and the overall average price across the portfolio was $37.85, compared with category-level average prices of $43.31 in Concentrates and $47.22 in Vapor Pens, implying that share concentration is anchored in higher-priced formats even as short-term volume momentum contracted across all categories.

The pattern suggests Revival is positioned as a Concentrates-first specialist whose reliance on an 82.38% share from one category amplifies exposure to category-specific swings, as evidenced by simultaneous MoM declines of 3.88% in Concentrates and 11.27% in Capsules alongside a steeper 22.59% drop in Vapor Pens. With a rank of 34 in New York Concentrates and only 17.62% of sales outside the core, the brand’s near-term trajectory is likely more sensitive to depth and differentiation within Concentrates than to diversification, implying that stabilizing or selectively growing Capsules could hedge volatility while Vapor Pens’ small 1.64% share limits its immediate impact despite sharper contraction.

Competitive Landscape

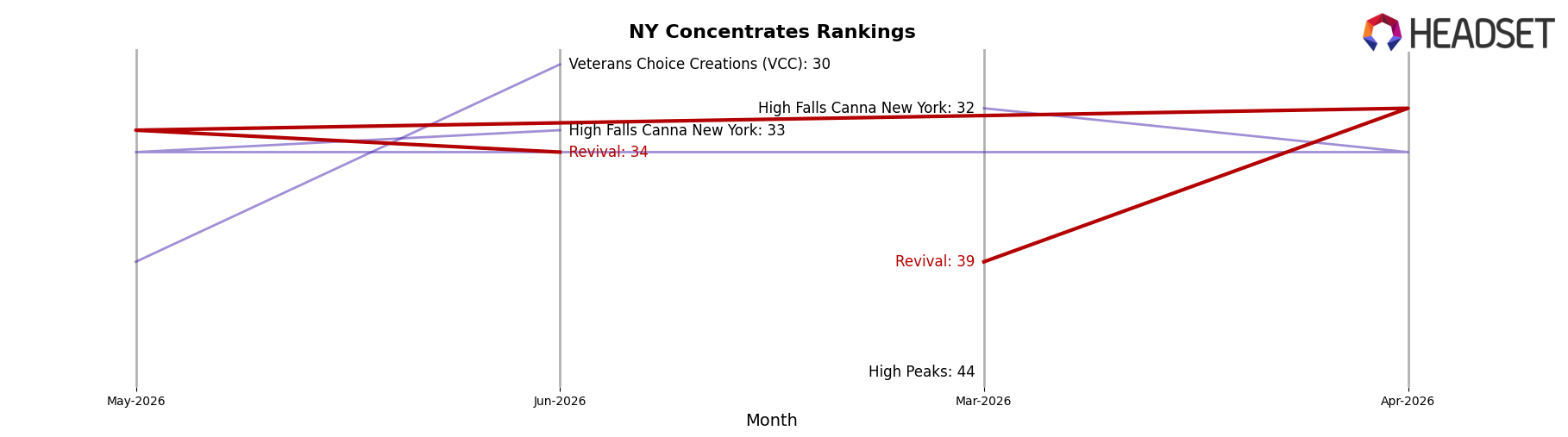

Revival ranks #34 in NY Concentrates in June 2026, with no year-over-year rank available, and it moved up 5 positions from #39 three months prior while still trailing its April 2026 peak of #32 by 2 ranks; this contrasts with Mfny (Marijuana Farms New York) holding #1 year over year at #1 and Jetpacks rising from #4 to #2, indicating category leaders are consolidating top spots as Revival inches forward. With UMAMII jumping from #26 to #3 alongside 1,648.3% YoY sales growth and RYTHM improving from #7 to #4 with 97.6% YoY sales growth, Revival’s modest rank gain of 5 places versus a 2-rank gap from its April 2026 peak implies the brand is stabilizing mid-pack but risks being outpaced by faster-climbing rivals unless momentum accelerates.

Notable Products

Papaya Bomb Live Rosin (1g) posted the steepest decline at -31.7% and slid to rank 2, while Superboof Cold Cured Live Hash Rosin (1g) fell -19.5% but held rank 1; four of the top ten are Concentrates, indicating concentration risk in a softening subcategory. Power Plant Live Hash Rosin (1g) was nearly flat at -0.9% at rank 4, whereas CBD/THC 1:1 Charge Tablets 20-Pack (100mg CBD, 100mg THC) dropped -20.5% at rank 8, contrasting with Flow Tablets 10-Pack (100mg) up 30.7% at rank 7. With Capsules mixed and Concentrates contracting at the top, the product mix points to overreliance on a few flagship Concentrates and an emerging need to diversify into stable Capsule formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.