Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

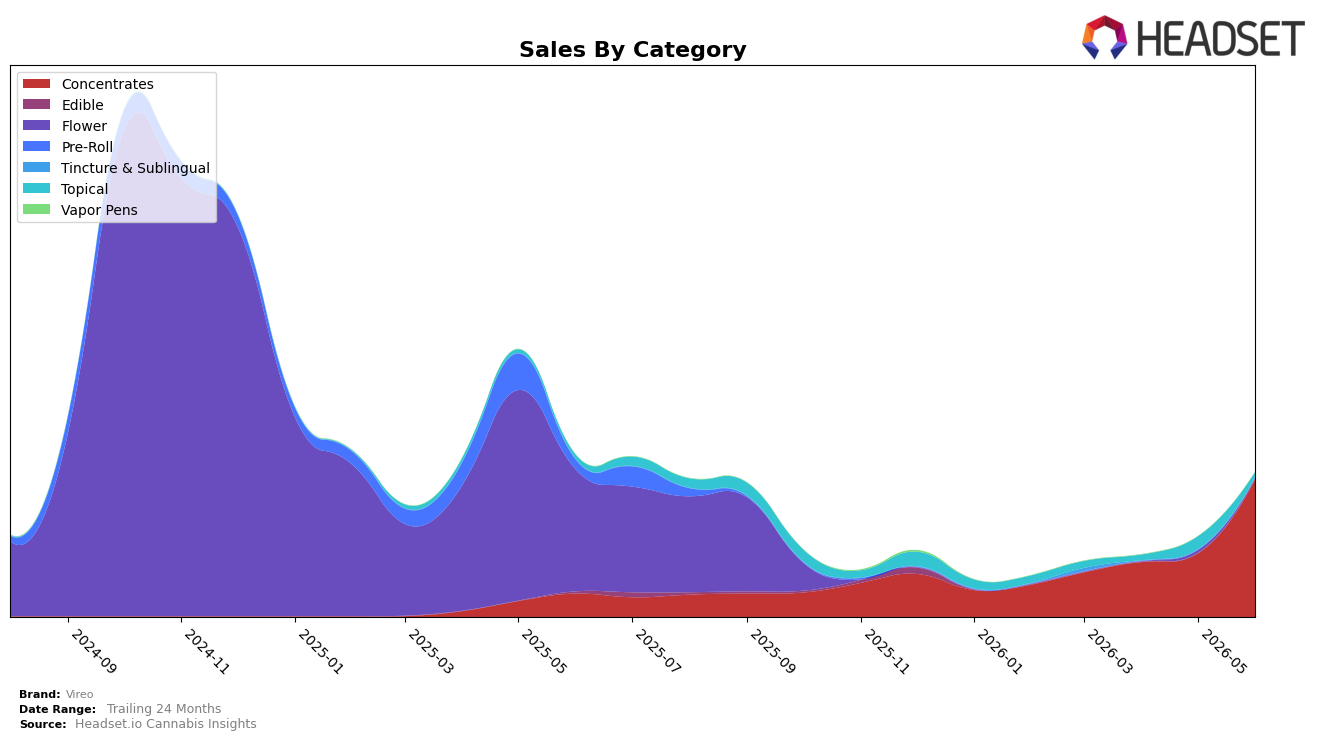

Vireo concentrated nearly all activity in Concentrates at 96.74% share while Topical held 3.26%, and within that mix Concentrates expanded 502.19% year over year alongside a 118.84% month over month jump. In contrast, Topical grew 16.11% year over year but fell 62.11% month over month, while average price lifted 90.89% year over year to $44.82. Despite category-level expansion, total brand sales declined 10.43% year over year, and in New York the brand sat at rank 15 in Concentrates; the pattern implies volume consolidation into a single category with price-led gains that are not offsetting broader revenue pressure.

The surge in Concentrates share to 96.74% combined with a 118.84% month over month increase and a 502.19% year over year rise points to a positioning pivot toward high-potency formats, while the 62.11% month over month drop in Topical and its 3.26% share indicate deprioritization of ancillary formats. With average price up 90.89% year over year and total brand sales still down 10.43% year over year, June 2026 performance suggests reliance on premiumized Concentrates to defend placement at rank 15 in New York, implying that sustaining growth will depend on either converting share into unit volume within Concentrates or rebuilding complementary categories to reduce single-category exposure.

Competitive Landscape

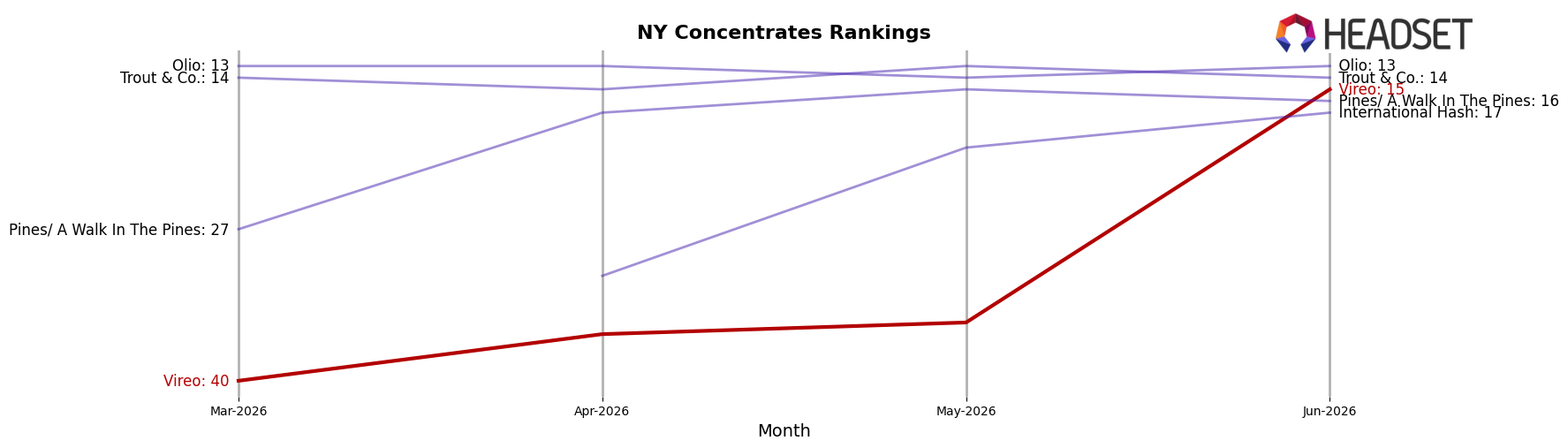

Vireo sits at rank #15 in New York Concentrates in June 2026, up 16 positions from #31 year over year and 25 positions from #40 three months ago, marking its peak rank to date and indicating accelerated share capture. In contrast, Mfny (Marijuana Farms New York) held #1 both year over year and currently while growing sales by 70.1%, and UMAMII surged from #26 to #3 alongside a 1,648.3% sales increase, signaling that Vireo’s rise from #31 to #15 narrows the gap with mid-tier peers but lags the pace of leaders’ step-changes. The pattern of a 16-rank YoY climb and a 25-rank improvement since March 2026 implies Vireo is transitioning from fringe presence to competitive relevance, but must convert rank momentum into sustained top-10 penetration.

Notable Products

Indica RSO Syringe (1g) posted the sharpest movement in June 2026 with a 198.6% month-over-month gain and climbed into rank 2, while Sativa RSO Syringe (1g) rose 136.2% MoM to rank 1. Hybrid RSO Syringe (1g) added 51.8% MoM and held rank 3, whereas CBD/THC 1:19 Red Balm (5mg CBD, 95mg THC, 1.5oz) fell 70.4% MoM at rank 4. With three RSO syringes occupying ranks 1–3 and the topicals declining 34.8%–70.4%, the mix indicates a pivot toward Concentrates driving the volume and away from legacy Topical SKUs, suggesting resource allocation should favor syringe production and adjacent concentrate formats over balms.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.