Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

ROBHOTS is stocked at 138 licensed dispensaries across Colorado and Missouri, 76 of them in Colorado, with the deepest coverage in Colorado Springs, Denver, Boulder, Northglenn, and Pueblo. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

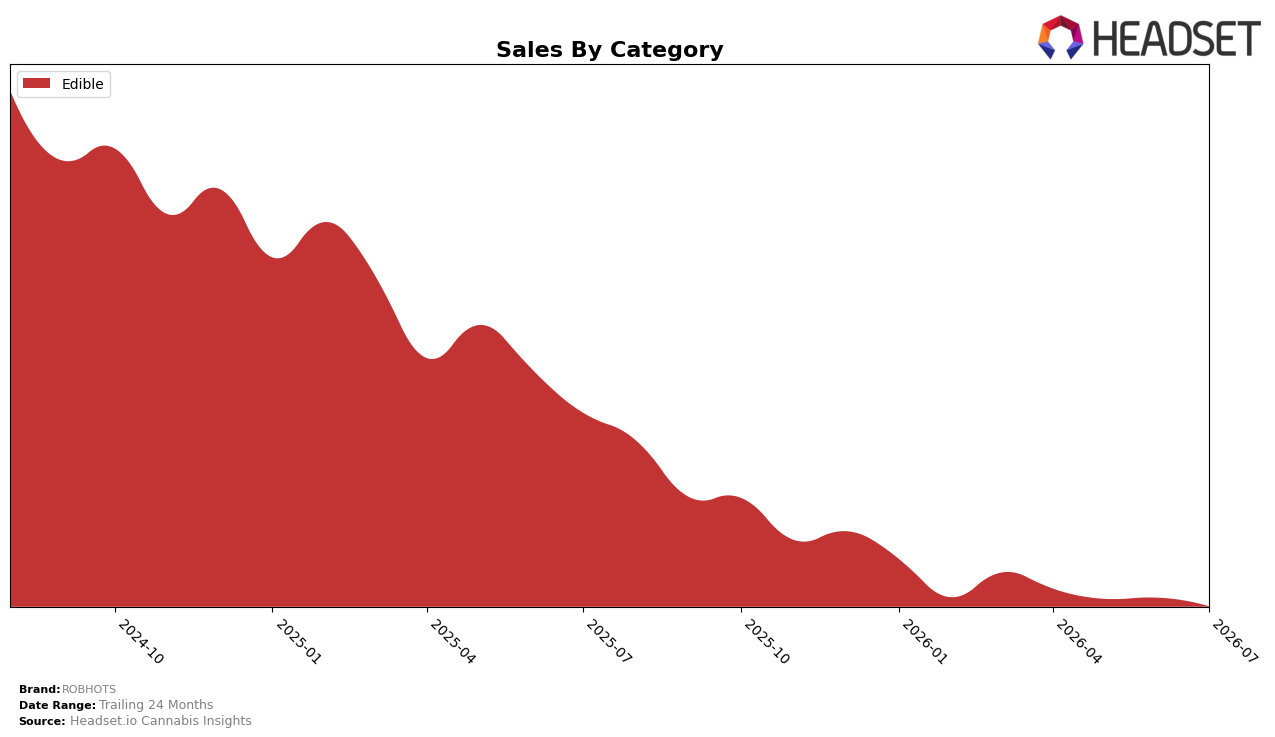

In July 2026, ROBHOTS remained 100.0% concentrated in Edible, with brand sales down 45.78% year over year and down 3.61% month over month, while average price rose 2.39% YoY. The Edible-only mix coincided with a 24‑month sales decline of 70.70%, and a category rank of 28 in Colorado Edible indicates a middle‑tier position; together, the single‑category exposure and simultaneous YoY and MoM contraction imply concentration risk that is not being offset by small price gains.

The persistence of a 100.0% Edible mix alongside a 3.61% MoM decline in July 2026 and a 45.78% YoY contraction suggests limited buffer against category‑specific volatility, and the rise in average price of 2.39% YoY while rank sits at 28 in Colorado implies price moves are not translating into share defense. The 70.70% sales drop over 24 months combined with unchanged category breadth signals a need to reframe positioning within Edible—either by sharpening differentiation at current price points or by adjusting pack/price architecture—because the current mix magnifies downside without evident offsetting volume elasticity.

Competitive Landscape

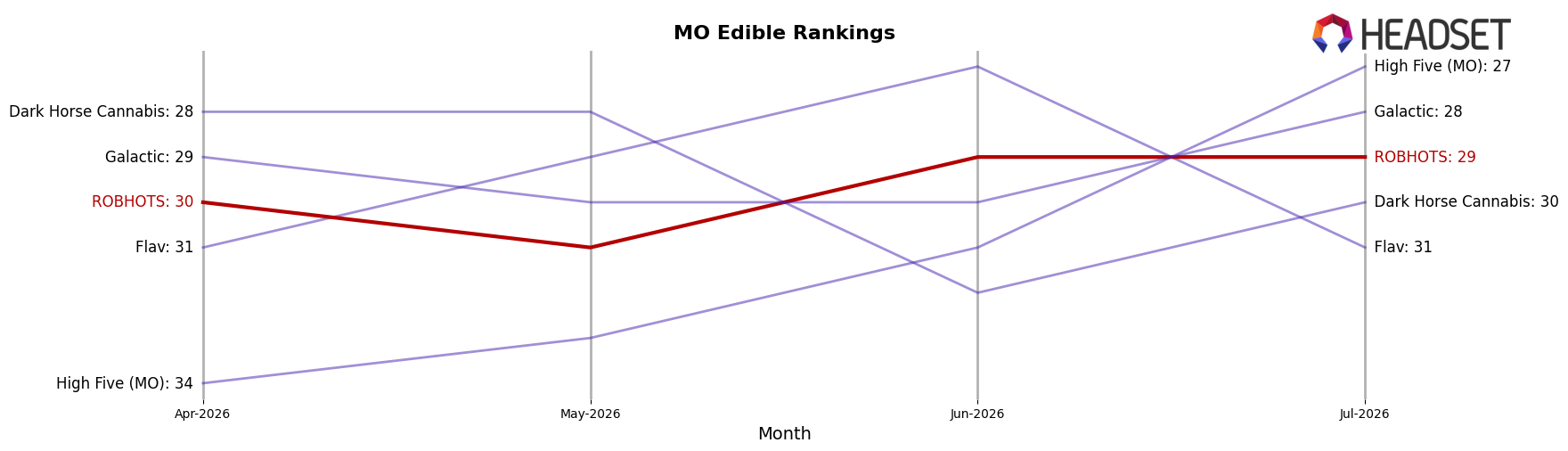

ROBHOTS sits at rank #29 in MO Edible in July 2026, down 4 positions from #25 year over year and up 1 position from #30 versus three months ago, while its peak of #16 in September 2024 remains 13 spots higher than today; by contrast, Good Day Farm improved from #3 to #2 as of July 2026 alongside an 11.8% YoY sales increase, and Smokiez Edibles slid from #2 to #5 with an 18.1% YoY decline, indicating that competitive share is redistributing at the top as ROBHOTS drifts lower. With category leaders diverging—Gron / Grön holding #1 despite a 5.5% YoY sales contraction and Good Taste rising from #8 to #4 on 63.8% YoY growth—ROBHOTS’ year-over-year rank slippage of 4 places alongside only a 1-position quarter-on-quarter lift implies a stalled recovery trajectory that risks further distance from its #16 peak unless mix or channel tactics change.

Notable Products

CBN/THC 1:1 Berry Relaxed Gummies 10-Pack (100mg CBN, 100mg THC) posted the standout move in July 2026 with a 102.7% month-over-month gain, jumping into rank 6, while Sour Blue Raspberry Gummies 2-Pack (100mg) fell 22.4% to rank 5. The category is concentrated in Edibles, with all ten top SKUs in the same category, and four of the top five are multi-cannabinoid or functionally positioned formulations, indicating a tilt toward effect-led offerings rather than flavor-only plays. The top two leaders—CBN/THC 2:1 Night Time Gummies 10-Pack (200mg CBN, 100mg THC, 30mg Melatonin) at rank 1 down 4.2% and Plus- CBD/THC 10:1 Sour Assorted Gummies 10-Pack (1000mg CBD, 100mg THC) at rank 2 down 4.3%—held share despite modest declines, together accounting for $92,777 in sales. This mix implies ROBHOTS is consolidating around functional CBN/CBD-led 10-packs while smaller 2-packs face pressure, signaling a migration toward higher-perceived utility formats and ratios.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.