Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Greenlight is stocked at 130 licensed dispensaries across Missouri, Oregon, and 5 other states, 77 of them in Missouri, with the deepest coverage in KCMO, St. Louis, Springfield, Cape Girardeau, and Joplin. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

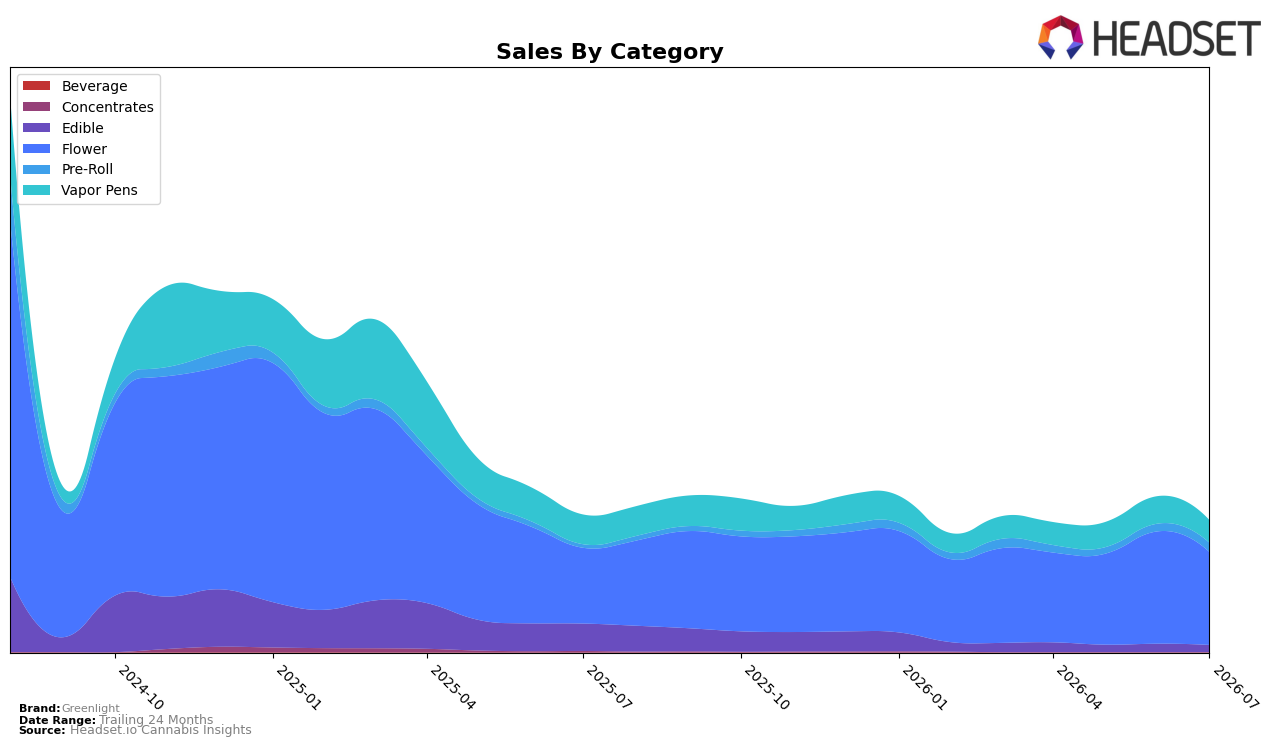

Greenlight concentrated 70.81% of July 2026 sales in Flower with a 22.80% year-over-year lift but a 17.34% month-over-month decline, while Vapor Pens held 17.11% share with a 23.93% YoY contraction and a 17.69% MoM pullback. Pre-Roll expanded to 6.81% share on 177.20% YoY growth and a 20.67% MoM increase, whereas Edible slid to 5.24% share with a 74.66% YoY drop and a 15.55% MoM decline; Concentrates remained at 0.03% share despite a 324.94% MoM spike and a 96.69% YoY fall. With average price up 5.85% YoY to $33.26 and total brand sales down 4.06% YoY, the mix suggests a pivot toward higher-priced Flower and resurgent Pre-Roll offset by Vapor Pens and Edible softness, implying reliance on core inhalables to buffer broader weakness.

Greenlight’s 25 rank in Flower in Missouri pairs with a 22.80% YoY Flower gain and a 17.34% MoM slip to indicate middle-of-pack traction that is sensitive to monthly volatility, while Pre-Roll’s 177.20% YoY surge and 20.67% MoM rise points to an on-ramp for share capture if sustained. The simultaneous 23.93% YoY decline in Vapor Pens and 74.66% YoY decline in Edible, alongside a 5.85% YoY increase in average price, points to a pricing-and-format mix that favors combustion formats over value-oriented alternatives; the thesis is that Greenlight’s positioning is consolidating around Flower leadership with Pre-Roll as a growth lever, but month-to-month stability will hinge on reducing exposure to Vapor Pens and Edible declines.

Competitive Landscape

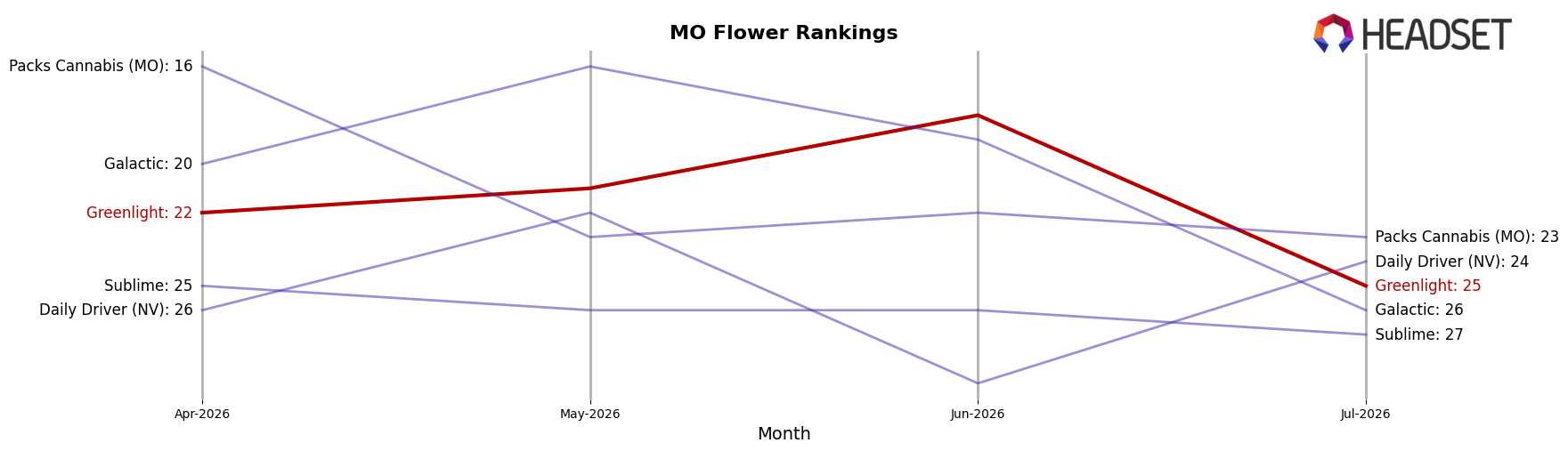

Greenlight sits at rank #25 in July 2026 in MO Flower, down 2 positions year over year from #23 and 3 positions from its April 2026 rank of #22; relative to the category peak of #5 in August 2024, the multi-quarter slide of 17 spots suggests persistent share erosion. In contrast, Sinse Cannabis climbed from #4 to #2 with a 8.99% year-over-year sales change while Local Cannabis Co. moved from #10 to #5 alongside a 41.83% sales increase, indicating competitors are consolidating higher-tier positions as Greenlight cedes rank; further, category leader Flora Farms held #1 year over year despite a -1.25% sales change, underscoring that Greenlight’s downward rank drift amid mixed top-tier momentum implies its competitive position is migrating from mid-pack contender toward lower-tier volatility unless trend drivers reverse.

Notable Products

Gold - Rainbow Snowman (3.5g) led July 2026 with a 26.8% month-over-month gain at rank 1, while Sativa Strawberry Gummies 10-Pack (100mg) slipped 7.0% to rank 10; with four of the top ten in Flower, the category’s weight at ranks 1, 2, 4, and 8 signals assortment gravity toward inhalables. Girl Scout Cookie Distillate Cartridge (1g) in Vapor Pens held rank 5 with a 1.4% lift versus Chem Cake Pre-Roll (1g) at rank 3 with a 1.9% rise, indicating cartridges are pacing steadier than pre-rolls despite lower rank mobility. The sales mix concentrates in higher-ranked Flower SKUs while Edibles contract at the fringe, implying Greenlight is orienting product strategy toward fast-turn inhalables and deprioritizing slower-moving format breadth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.