Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Seattle Bubble Works is stocked at 106 licensed dispensaries across Washington, with the deepest coverage in Seattle, Bellevue, Bellingham, Spokane, and Lynnwood. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

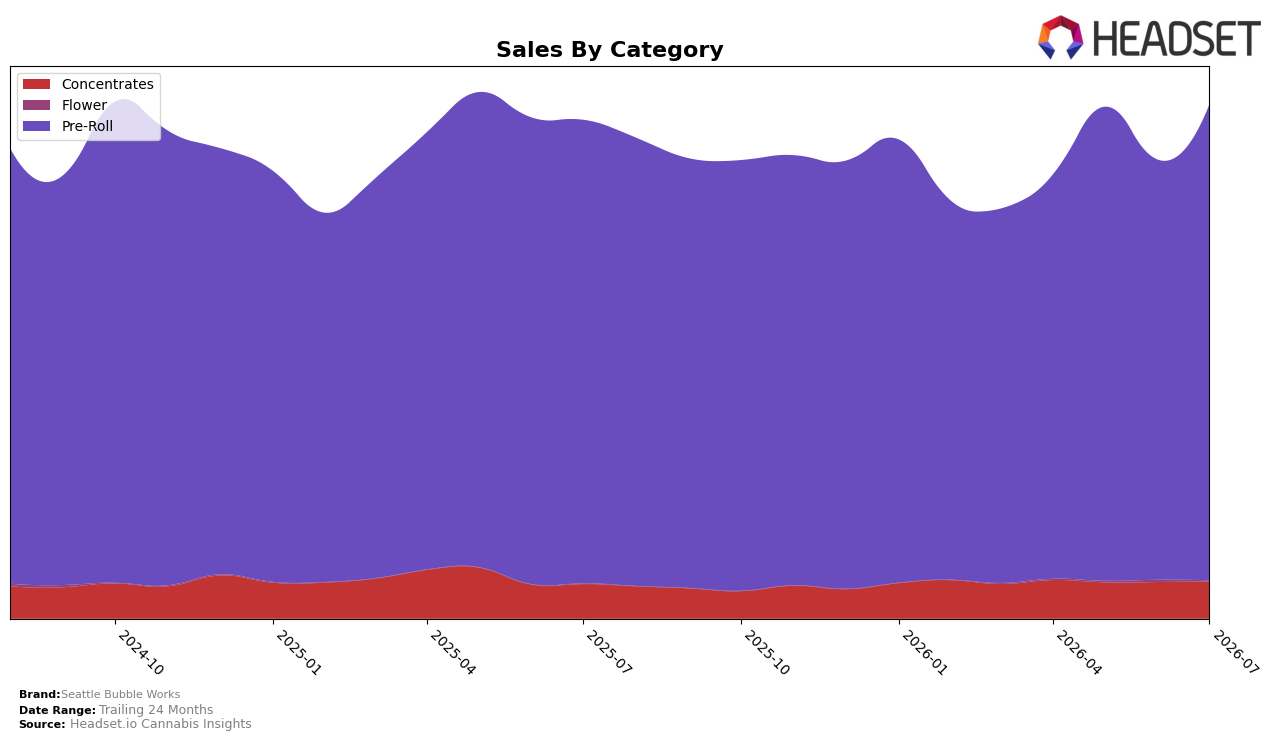

Seattle Bubble Works concentrated 92.70% of July 2026 sales in Pre-Roll with a 13.35% month-over-month gain and 2.70% year-over-year growth, while Concentrates held 7.16% share with 1.26% MoM and 7.48% YoY. Flower remained a rounding error at 0.14% share despite a 167.29% YoY swing, as the category fell 59.12% MoM, and the brand’s average price declined 8.41% YoY to $8.46 even as overall brand sales rose 3.12% YoY. With an eighth-place rank in Pre-Roll in Washington, the pattern implies Seattle Bubble Works is leaning further into value-leaning Pre-Rolls to capture incremental volume MoM while accepting price compression to defend share against higher-priced tiers.

The mix shift—13.35% MoM volume lift in a 92.70% Pre-Roll base and only 1.26% MoM growth in a 7.16% Concentrates niche—indicates a strategy anchored in high-frequency, lower-ticket products, reinforced by an 8.41% YoY price reduction. Coupled with a YoY sales uptick of 3.12% against only 2.70% YoY growth in the core Pre-Roll category for the brand, this positioning suggests the brand is trading price for velocity to sustain its eighth-place Pre-Roll rank in Washington, with limited diversification upside while Concentrates grows slowly and Flower volatility (−59.12% MoM despite +167.29% YoY) remains operationally irrelevant.

Competitive Landscape

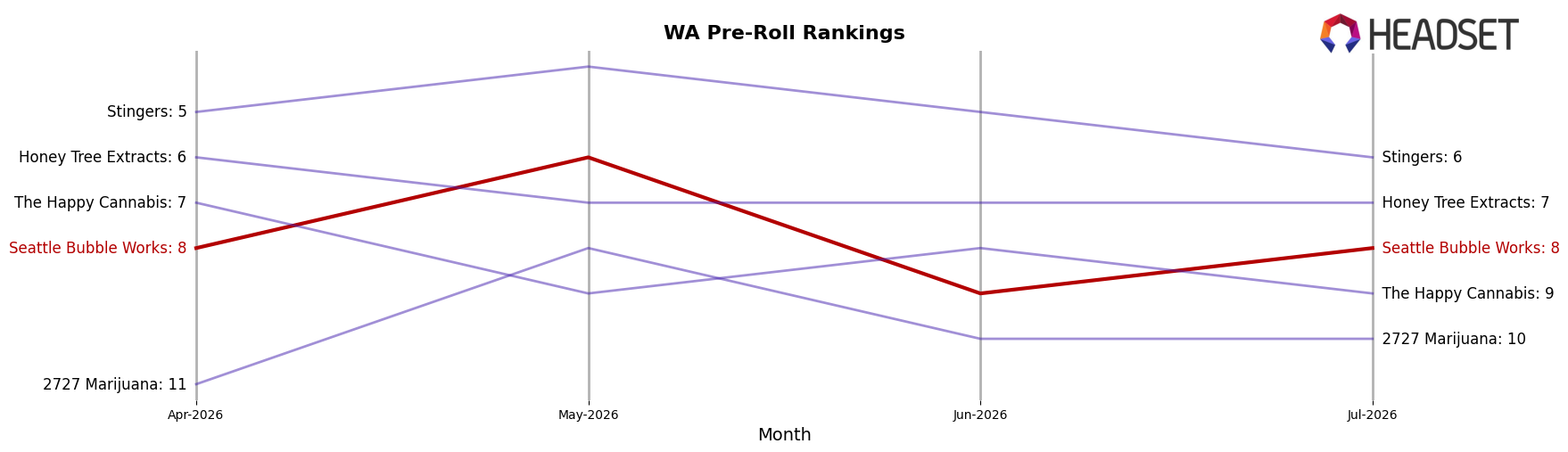

Seattle Bubble Works sits at rank #8 in WA Pre-Roll in July 2026, down 2 positions year over year from #6, and unchanged versus April 2026 at #8, while its peak of #6 in May 2026 marks a 2-rank retreat since then; meanwhile, Ooowee advanced from #2 to #1 with 59.5% year-over-year sales growth as Phat Panda slipped from #1 to #2 despite 1.2% growth, indicating that leaders are widening gaps on even flat-to-modest growers. With Lifted Cannabis Co rising from #7 to #4 alongside 30.0% growth and Fire Bros. jumping from #11 to #5 with 52.0% growth, Seattle Bubble Works’ slide from #6 to #8 amid peers’ upward mobility signals share is being redistributed toward faster-growing rivals, implying that without a change in velocity, the brand’s trajectory points to further mid-pack drift rather than a return to its May 2026 peak.

Notable Products

Wedding Cake Hash Infused Pre-Roll 2-Pack (1g) posted the sharpest move in July 2026 with +45.96% MoM, yet it held rank 5 while Blue Dream Hash Infused Pre-Roll 2-Pack (1g) at rank 1 advanced +34.16% MoM, indicating gains concentrated but not fully reordering the leaderboard. Granddaddy Purple Hash Infused Pre-Roll 10-Pack (5g) at rank 3 rose +32.19% MoM while the Blue Dream Hash Infused Pre-Roll 10-Pack (5g) at rank 6 climbed +24.79% MoM, and eight of the top ten are Pre-Roll 2-Packs or 10-Packs from the same infused family, pointing to format-driven demand around infused multi-packs rather than strain-specific shifts. Super Boof Hash Infused Pre-Roll 2-Pack (1g) slipped -7.99% MoM at rank 7 while Mystery Machine Hash Infused Pre-Roll 2-Pack (1g) edged down -2.09% at rank 10, suggesting underperformance is isolated within a largely expanding lineup. The mix implies Seattle Bubble Works is steering volume toward infused Pre-Roll multipacks where double-digit MoM growth and top-6 ranks cluster, supporting a scale strategy anchored in repeatable pack formats and fewer single-SKU bets, with July 2026 revenue led by the Blue Dream Hash Infused Pre-Roll 10-Pack (5g) at $38,991.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.