Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

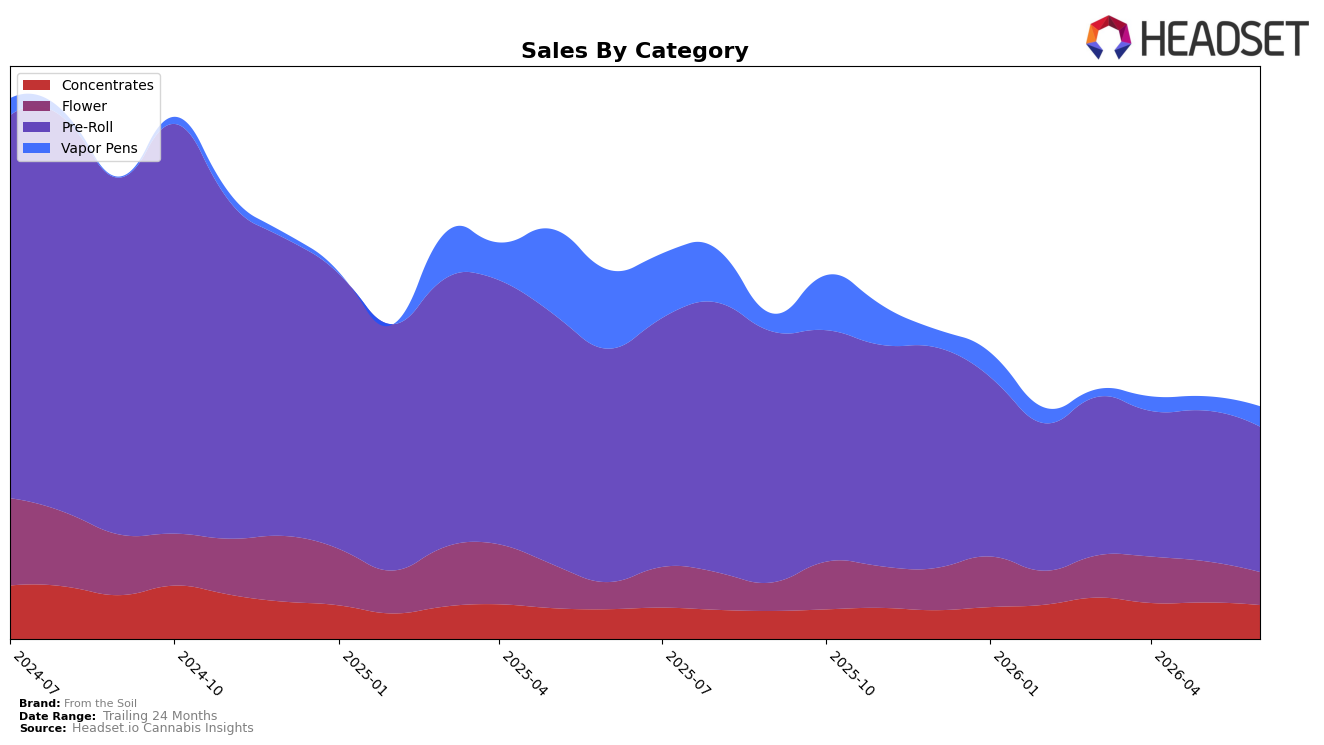

From the Soil’s mix in June 2026 is anchored by Pre-Roll at 53.31% share with year-over-year sales down 34.90% and month-over-month down 3.12%, while Vapor Pens hold 12.75% share with a 59.84% year-over-year decline but an 18.52% month-over-month lift. In contrast, Concentrates at 17.12% share grew 8.49% year-over-year but slipped 4.63% month-over-month, and Flower at 16.83% share rose 12.81% year-over-year yet fell 13.87% month-over-month. With brand-level sales down 30.71% year-over-year alongside a 3.57% average price decline, the pattern implies the current reliance on Pre-Roll is amplifying aggregate contraction, while near-term volatility in Flower and Vapor Pens is reshaping the monthly trajectory.

Given a Pre-Roll rank of 20 in Washington and a 53.31% category share within the brand’s mix, the double pressure of a 34.90% year-over-year decline and a 3.12% month-over-month dip suggests the core position is eroding even as Vapor Pens post an 18.52% month-over-month rebound and Flower shows a 12.81% year-over-year increase. Concentrates’ 8.49% year-over-year growth coupled with a 4.63% month-over-month pullback indicates steady contribution but not yet a counterweight to Pre-Roll’s drag; the implication is a needed reweighting toward categories with positive year-over-year momentum (Flower, Concentrates) while using the Vapor Pens month-over-month uptick to test recovery without overexposure to its 59.84% year-over-year decline.

Competitive Landscape

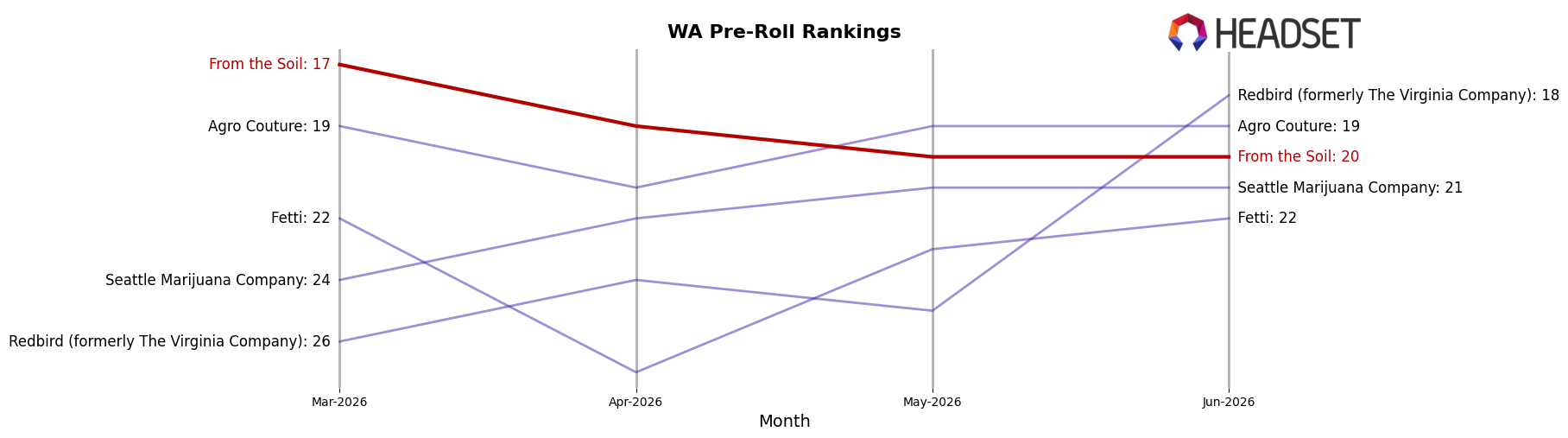

From the Soil is ranked #20 in WA Pre-Roll for June 2026, down 7 positions year over year from #13, and 3 spots below its March 2026 rank of #17; the brand’s peak of #5 in August 2024 contrasts with a current placement 15 ranks lower, indicating erosion in relative standing. Meanwhile, Ooowee moved from #2 to #1 and Lifted Cannabis Co advanced from #6 to #4, while From the Soil trended from #13 to #20, implying competitors are taking share faster than From the Soil can recover despite past peak performance. The pattern implies a shift from top-quintile presence to lower-tier positioning, signaling that without a rank reversal over the next two to three months the brand risks further shelf-space pressure relative to rivals advancing by 2–5 ranks year over year.

Notable Products

Chilly Willy Pre-Roll 2-Pack (1.5g) recorded the steepest movement in June 2026 with a -38.36% month-over-month drop while holding rank 8, signaling a sharp pullback that contrasts with Lemon Amnesia Pre-Roll 2-Pack (1.5g) at rank 1 with +50.80% growth. Across the top ten, seven SKUs are Pre-Rolls including positions 1, 3, 4, 6, 7, 8, and 10, indicating category concentration even as Indica RSO Syringe (1g) sits at rank 2 with a -4.38% dip. The spread between rank 1 at +50.80% and ranks 6 and 7 at -4.94% and -6.49% points to bifurcated Pre-Roll momentum rather than a uniform category lift.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.