Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

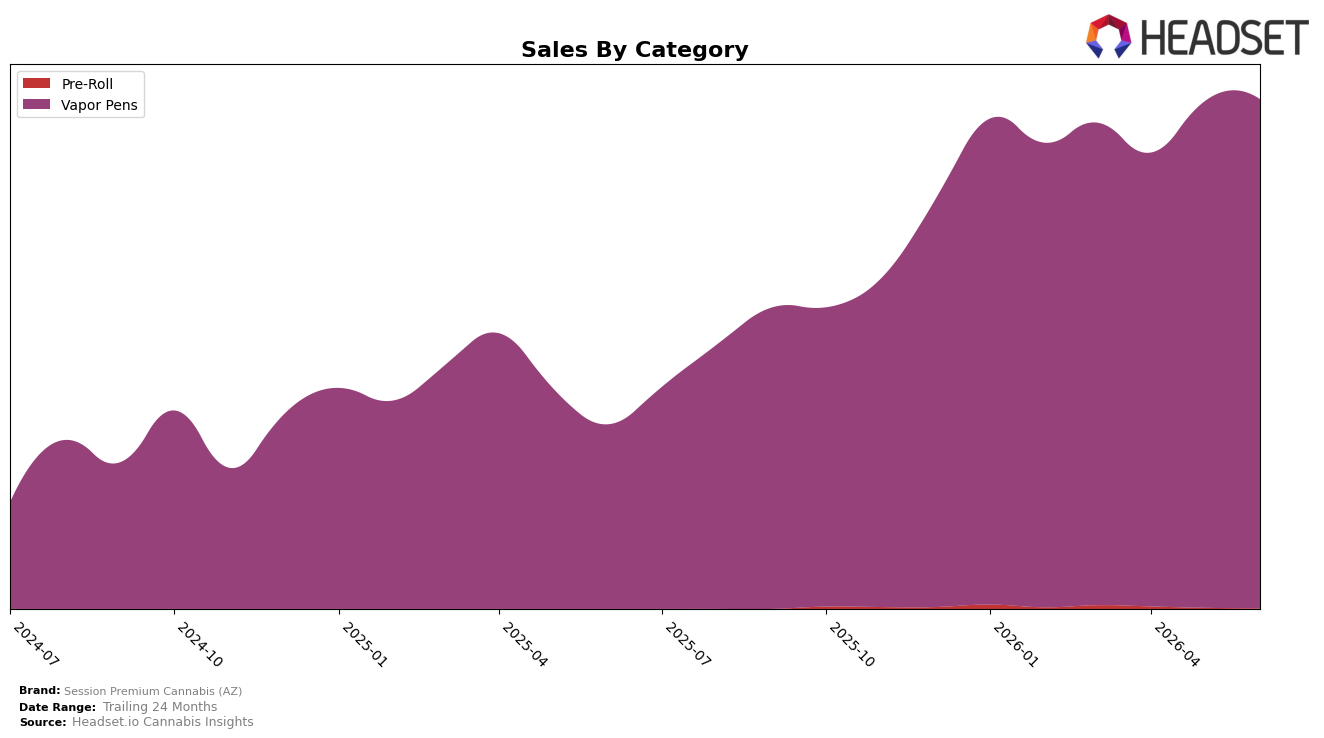

In June 2026, Session Premium Cannabis (AZ) derived 99.89% category share from Vapor Pens with a 176.27% year-over-year sales increase and a 0.53% month-over-month lift, while Pre-Roll held 0.11% share with a 47.12% month-over-month decline and no comparable year-over-year figure. The brand’s average price fell 4.65% year-over-year to $30.65 even as Vapor Pens’ average price sat at $30.78, and the brand ranked 8th in Vapor Pens in Arizona. The pattern implies a concentrated bet on Vapor Pens is expanding volume despite mild price compression, while Pre-Roll remains de minimis and a drag on diversification.

With 99.89% of sales concentrated in Vapor Pens and an 8th-place rank in Arizona, the 0.53% month-over-month gain paired with a 176.27% year-over-year surge suggests the brand is trading on scale and velocity rather than mix breadth, supported by a 4.65% decline in average price that likely aided unit pull-through. The 47.12% month-over-month contraction in Pre-Roll alongside a 0.11% share indicates limited traction outside the core, implying that near-term positioning relies on defending Vapor Pens rank and price architecture more than building secondary categories.

Competitive Landscape

Session Premium Cannabis (AZ) sits at rank #8 in AZ Vapor Pens in June 2026, improving 5 positions YoY from #13, while holding flat versus March 2026 at #8; this movement trails Abstrakt, which climbed from #5 to #2 alongside a 162.2% YoY sales lift, yet outpaces STIIIZY, which slipped from #4 to #5 with a 14.7% YoY decline. The brand’s peak rank of #7 in January 2026 and current #8 suggest a narrow band of competitiveness, whereas category leaders like Mfused held #1 YoY-to-current despite a 19.4% YoY sales contraction and Dime Industries edged from #2 to #3 with a 10.9% YoY increase; the pattern implies Session Premium Cannabis (AZ) is consolidating a mid-top-10 position, with advancement contingent on displacing softening incumbents rather than chasing breakout growers.

Notable Products

Jack Herer Live Resin Disposable (1g) posted the steepest decline at -38.1% month over month and slid to rank 7, while Cornbread Live Resin Disposable (1g) fell -25.9% at rank 10, indicating demand is consolidating away from legacy strain SKUs. In contrast, Tropsanto 90 Live Resin Disposable (1g) surged +50.6% to rank 2, narrowing the gap with rank-1 Donkey Butter Live Resin Disposable (1g) as Las Vegas Triangle Kush Live Resin Disposable (1g) inched up just +1.5% at rank 9. With all ten top products in Vapor Pens and five of the top six concentrated in Live Resin disposables, the mix points to a strategy prioritizing fast-turn, strain-rotated disposables over breadth, which implies deeper focus on a few breakout strains rather than wide catalog coverage.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.