Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

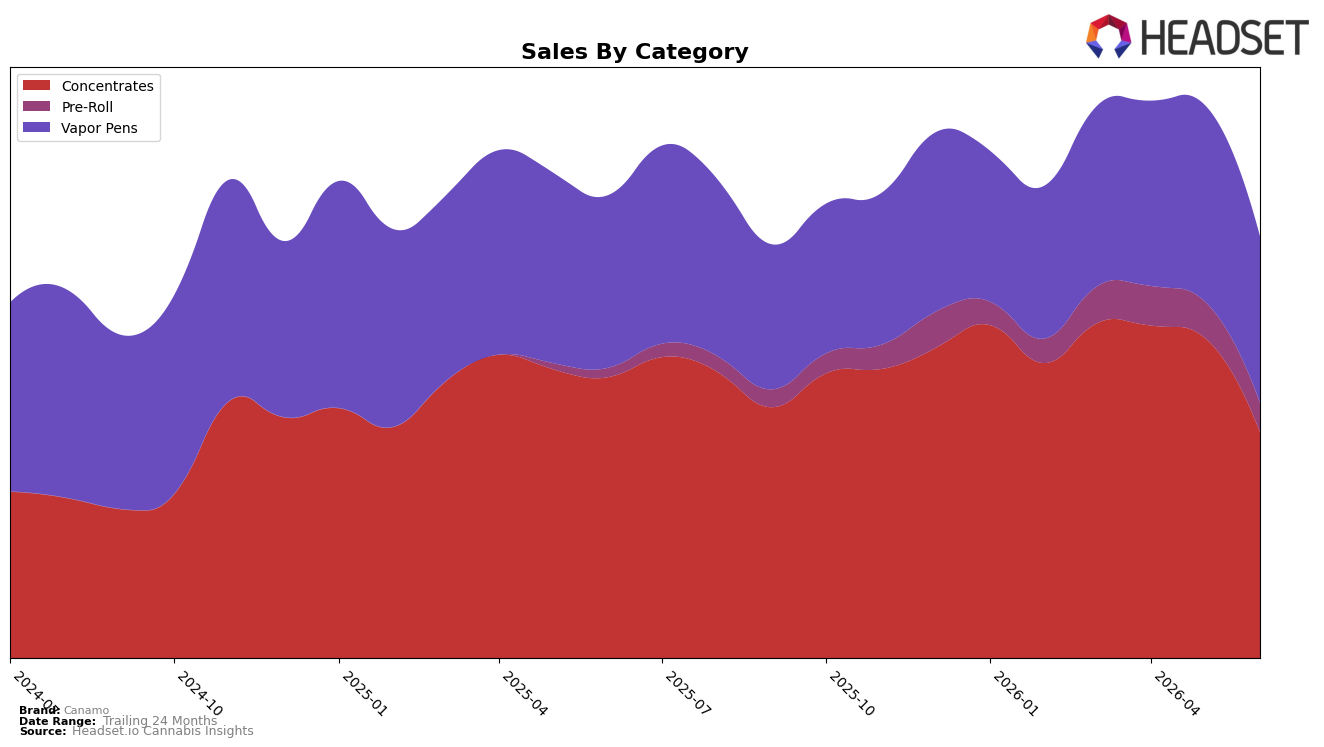

In June 2026, Canamo’s mix was concentrated in Concentrates at 53.56% share (ranked #2 in Concentrates in Arizona), with Vapor Pens at 39.50% and Pre-Roll at 6.94%. Year over year, Concentrates declined 19.67% while Vapor Pens slipped 3.53%, contrasted by a 220.26% surge in Pre-Roll; month over month, Concentrates fell 29.56% and Vapor Pens dropped 15.24%, with Pre-Roll down 19.32%. With average price down 17.08% year over year alongside brand sales down 8.92% year over year, the pattern implies price-led pressure in core categories while the rapidly expanding but small Pre-Roll base is not yet offsetting volume softness.

The shifts imply Canamo is overexposed to a weakening Core of Concentrates and Vapor Pens, where double-digit month-over-month declines of 29.56% and 15.24% outpaced the portfolio’s smaller Pre-Roll tail, despite Pre-Roll’s 220.26% year-over-year growth. Holding the #2 rank in Concentrates in Arizona while category sales contracted 19.67% year over year and 29.56% month over month suggests a defensive posture that relies on share retention rather than category expansion; the mix at 53.56% in Concentrates and 39.50% in Vapor Pens indicates that without reweighting toward faster-growing formats, Canamo’s June 2026 position will continue to translate into under-leveraged rank in a shrinking primary category.

Competitive Landscape

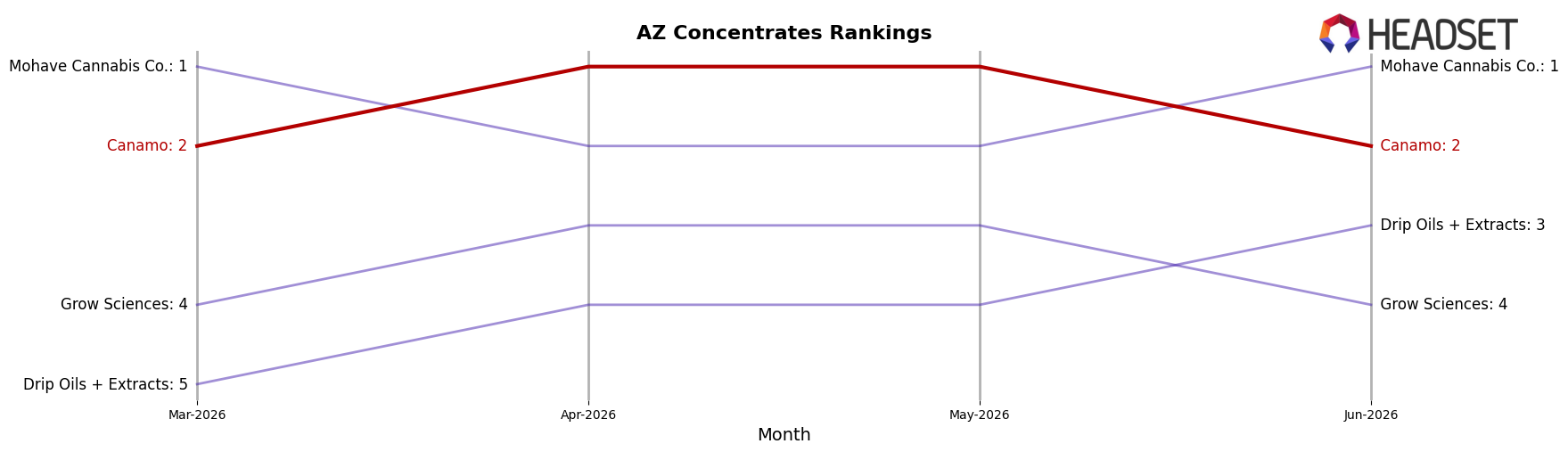

Canamo sits at rank #2 in AZ Concentrates in June 2026, unchanged YoY from rank #2, and held #2 for the last three months while peaking at #1 in May 2026; in contrast, Mohave Cannabis Co. stayed at #1 YoY and remains #1 in June 2026, and Drip Oils + Extracts climbed from #5 YoY to #3 with a 32.5% YoY sales gain. Meanwhile, Grow Sciences advanced from #7 YoY to #4 with 106.5% YoY sales growth, while WTF Extracts slipped from #3 YoY to #5 with a 14.4% YoY sales decline; this spread—competitors moving +2 to +3 ranks around a static #2—implies Canamo’s path back to #1 hinges on displacing a stable #1 while containing share leakage to faster-rising #3–#4 players.

Notable Products

Oishii Rainbow x Grape Ox Infused Pre-Roll (1g) posted the steepest decline at -20.8% month over month and slid to rank 9 in June 2026, signaling softness in infused pre-roll velocity relative to higher-ranked formats. Concentrates occupy 4 of the top 10 positions with ranks 1, 3, 5, and 8, while Vapor Pens sit at ranks 6 and 7, indicating that inhalables outside pre-rolls are carrying share even as the top pre-rolls at ranks 2 and 4 hold placement without evident growth rates. The Permanent Lime Live Resin Disposable (1g) at rank 6 and Kush Mints Live Resin Disposable (1g) at rank 7 cluster mid-table despite higher unit-value potential, with one Vapor Pen posting $31,807 in June 2026, implying pricing power is present but not yet translating into rank gains. Taken together, the mix points to Canamo leaning into concentrates and live resin vapes while reassessing infused pre-roll depth, prioritizing SKUs that can sustain rank without month-over-month volatility.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.