Market Insights Snapshot

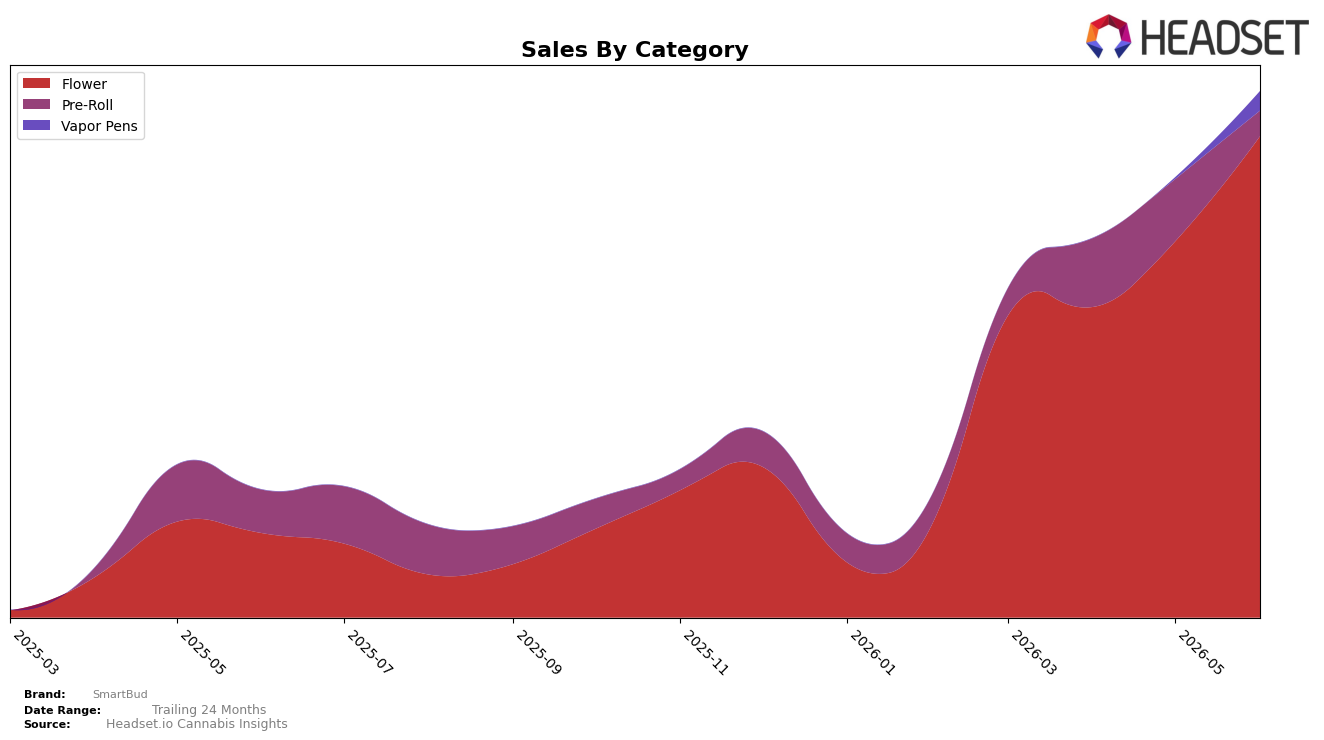

In June 2026, SmartBud concentrated 91.55% of sales in Flower, where year-over-year sales rose 471.30% and month-over-month grew 27.97%, while Pre-Roll contracted to 4.79% share with a -41.46% YoY and -59.32% MoM decline. Vapor Pens expanded to 3.66% share on a 1,141.78% MoM surge despite no YoY baseline, and average prices rose 69.10% YoY to $47.39, with Flower pricing at $48.72 and Pre-Roll at $37.55. The pattern implies SmartBud is consolidating around Flower momentum while rapidly testing into Vapor Pens and de-emphasizing Pre-Roll, shifting mix toward higher-priced formats and faster-growth segments.

Given Flower’s gains and a rank of 25 in Flower within New York, the mix shift signals a push to climb the middle tier by deepening Flower assortment while using Vapor Pens’ triple-digit MoM to open a second demand lane. The simultaneous Pre-Roll pullback and higher average prices suggest deliberate trade-up and capacity reallocation, implying SmartBud’s positioning is migrating toward premiumized inhalables anchored in Flower with Vapor Pens as the incremental share engine.

Competitive Landscape

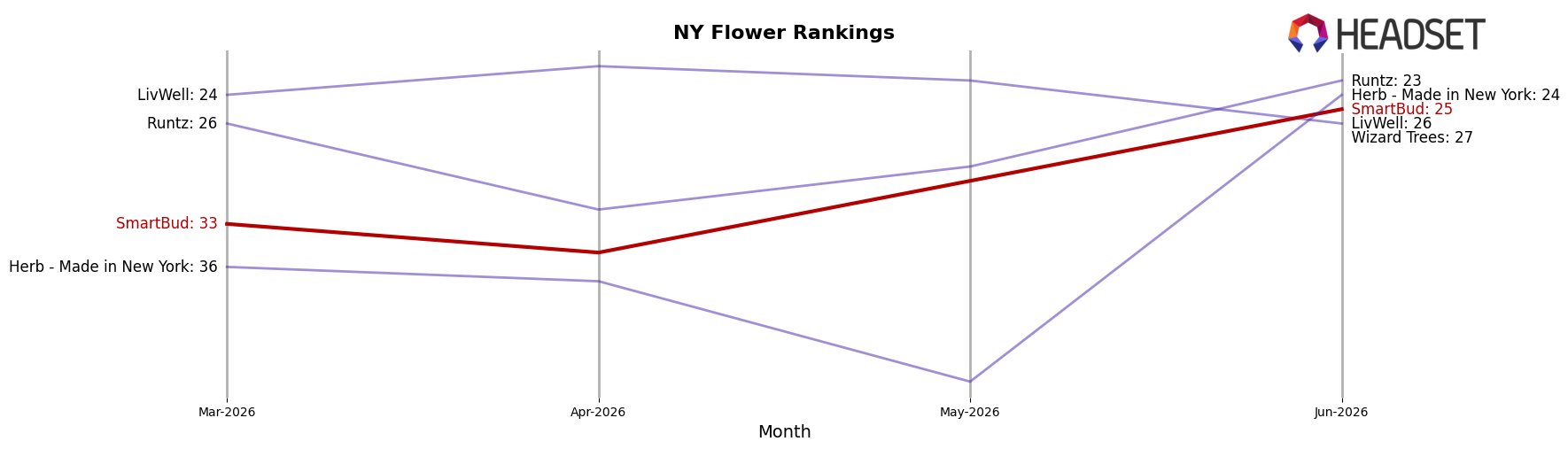

SmartBud sits at rank #25 in New York Flower in June 2026, rising 47 spots year over year from #72, and improving 8 positions since March 2026 when it was #33; this marks a new peak rank of #25 in June 2026 while still trailing the top tier. In contrast, Find. moved from #3 to #1 year over year and RYTHM advanced from #10 to #5 with 40.6% YoY sales growth, while Dank. By Definition slipped from #1 to #3 alongside a 50.7% YoY sales decline; this mix of upward and downward mobility around the top five indicates SmartBud’s jump from #72 to #25 is catching a window where leadership is rotating, implying the trajectory points to attainable entry into the top 20 if share gains persist faster than mid-pack rivals over the next two to three months.

Notable Products

Girl Scout Cookies (3.5g) posted the standout move in June 2026 with a +74.9% MoM surge to rank 1, while CandyLato Ground (14g) fell -60.8% to rank 10, marking a sharp bifurcation at the top and bottom of the list. Blue Dream (3.5g) advanced +47.1% MoM to rank 2, and with four of the top ten being 14g pre-ground SKUs, the format remains concentrated even as premium 3.5g packs gain momentum. The mix implies SmartBud is tilting toward a barbell of premium 3.5g trial and value-driven pre-ground volume, suggesting pricing architecture and pack-size strategy are now the primary levers for growth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.