Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

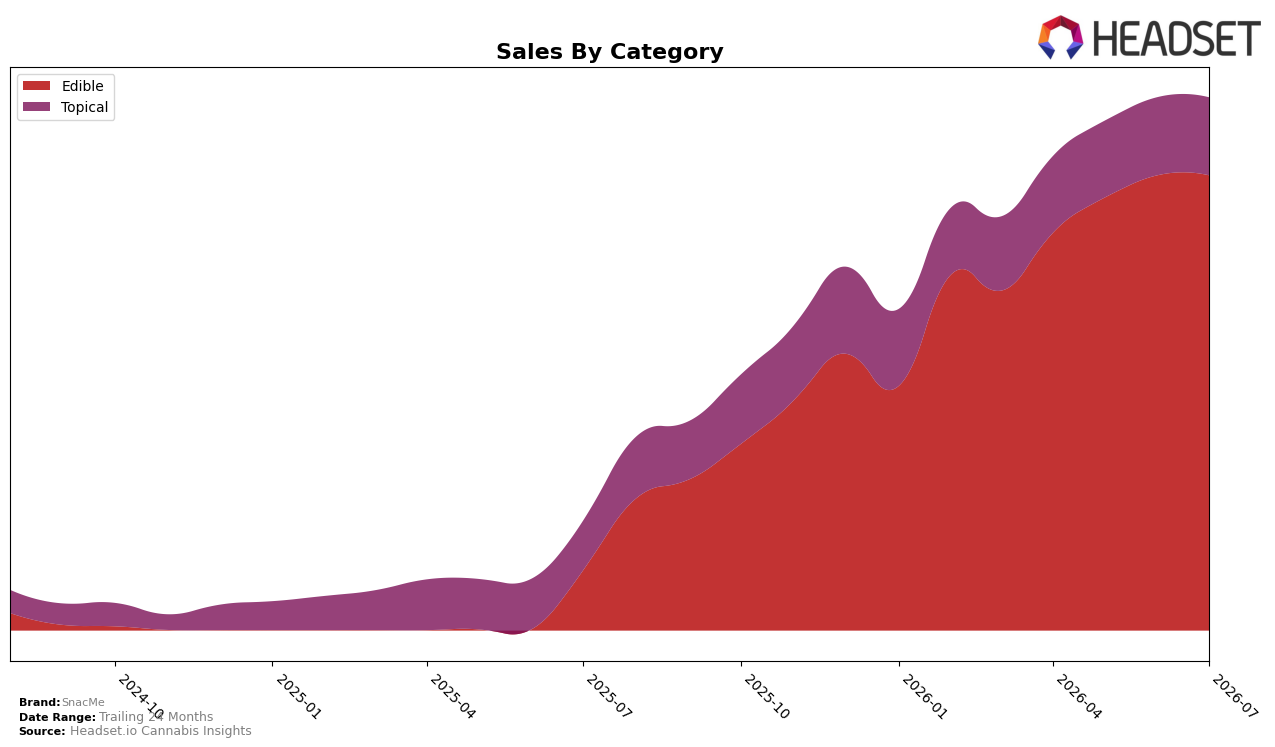

SnacMe concentrated 85.42% share in Edible with July 2026 sales up 663.18% year over year while month over month edged down 0.02%, and held 14.58% share in Topical with 57.48% year-over-year growth but a 13.38% month-over-month decline; the average price dropped 22.60% YoY to $6.04, with Edible averaging $5.71 and Topical $9.21. Within Washington Edible, the brand sat at rank 18 in July 2026, indicating category scale despite mixed monthly momentum; this pattern implies the portfolio is anchored in value-leaning Edibles that are expanding faster YoY than the rest of the mix, even as near-term pricing and MoM softness temper velocity.

The tilt toward Edible at 85.42% share versus 14.58% in Topical, alongside a 663.18% YoY surge in Edible compared to 57.48% in Topical and a rank position of 18 in Washington Edible, suggests SnacMe’s positioning is consolidating around accessible, lower-priced form factors. With Edible MoM at -0.02% versus Topical at -13.38% and a 22.60% YoY price decline, the mix signals a strategy prioritizing volume capture and shelf breadth in Edibles while de-emphasizing Topicals, implying that sustaining rank will depend on maintaining price-to-value differentiation rather than broadening into slower-moving segments.

Competitive Landscape

SnacMe sits at rank #18 in WA Edible in July 2026 after rising 20 positions from #38 year over year, and edging up 2 spots from #20 in April 2026 to hit a peak rank of #18 in July 2026; by contrast, Wyld held #1 with a 7.99% YoY sales increase while Hot Sugar stayed at #3 despite a -5.92% YoY decline, indicating SnacMe’s share gains are occurring as some leaders plateau and others contract. With Journeyman improving from #5 to #4 on 6.47% YoY growth and Craft Elixirs slipping from #4 to #5 alongside an -8.01% YoY sales change, the mix above SnacMe is fluid, which implies SnacMe’s rank trajectory toward the mid-teens is driven by relative outperformance versus declining incumbents and could sustain incremental share capture if the category’s top five remain bifurcated.

Notable Products

Blue Watermelon Gummy Bombs 10-Pack (100mg) set the tone in July 2026 with a -14.47% month-over-month decline while holding rank 3, indicating share leakage within the top tier despite Gummy Bombs - Candy Apple Gummies 10-Pack (100mg) rising 12.48% at rank 1. Gummy Bomb - Huckleberry Gummies 10-Pack (100mg) added 10.49% at rank 2, while Gummy Bombs - Luau Punch Gummies 10-Pack (100mg) and Gummy Bombs - Strawberry Guava Gummies 10-Pack (100mg) fell -8.35% and -8.31% at ranks 6 and 7, respectively, and the category concentration is clear with ten of the top ten as Edible SKUs. Gummy Bombs - Pink Razz Gummies 10-Pack (100mg) advanced 5.20% at rank 8 and Gummy Bombs - Mountain Peach Gummies 10-Pack (100mg) gained 8.48% at rank 9, while Gummy Bombs - Dragon Berry Gummies 10-Pack (100mg) slipped -2.05% at rank 5 and Gummy Bombs - White Nectarine Gummies 10-Pack (100mg) eased -3.98% at rank 10. The mix suggests SnacMe is consolidating around a few flagship gummy variants with positive MoM momentum at the very top offsetting mid-pack erosion, implying a need to curate flavors and defend rank positions rather than expand breadth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.