Market Insights Snapshot

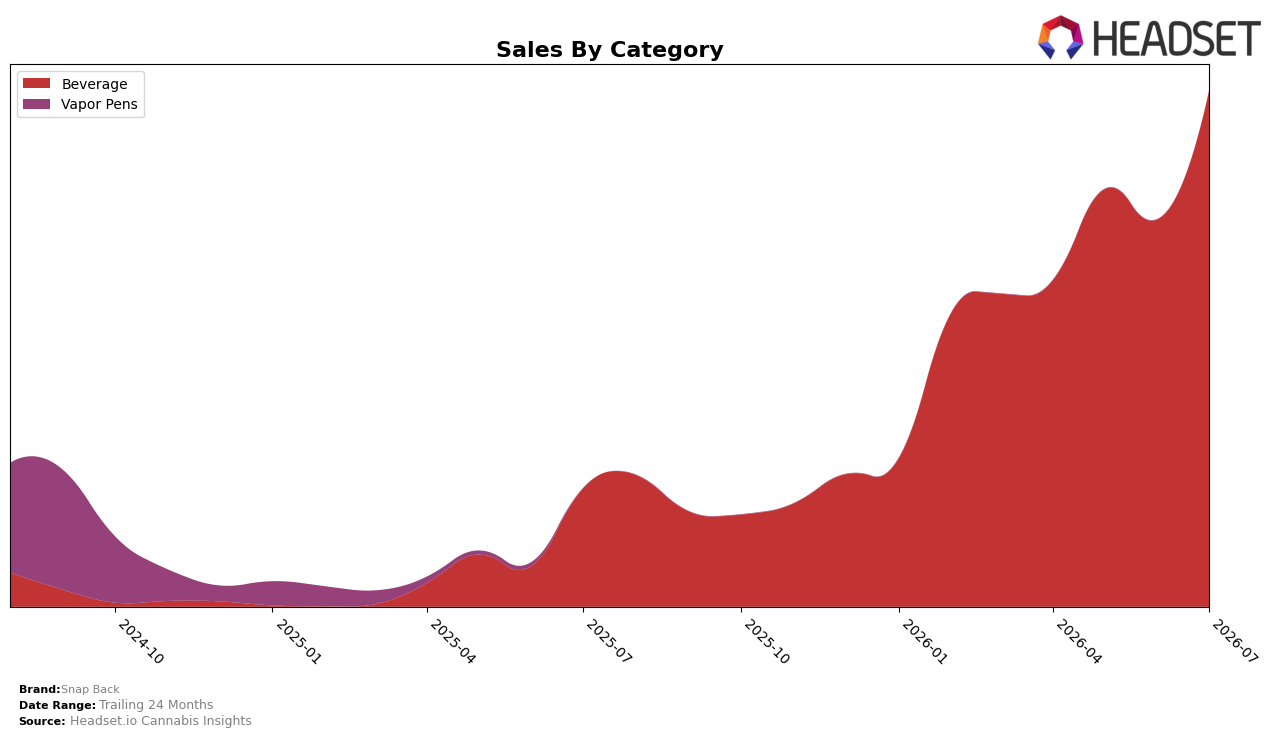

In July 2026, Snap Back operated as a single-category play with Beverage at 100.0% of mix and a category rank of 15 in Beverage within Alberta, pairing a 337.4% year-over-year sales increase with a 33.2% month-over-month climb. The average price moved down 7.9% year over year while Beverage volume scaled enough to support a 122.4% two-year sales lift, indicating that price elasticity is currently favorable and that rank 15 leaves headroom for category penetration without requiring mix expansion.

The consolidation into Beverage at 100.0% alongside a 33.2% month-over-month gain and a 7.9% year-over-year price decrease implies the brand is competing on velocity rather than premium positioning, using price to widen the buyer base while protecting contribution through volume. With July 2026 rank at 15 and July 2026 year-over-year sales growth at 337.4%, the path to move into the top 10 is most efficiently driven by continued price discipline and flavor/SKU depth within Beverage rather than diversifying mix, because share wins are occurring at current price tiers and the two-year growth of 122.4% signals repeatability in the existing lane.

Competitive Landscape

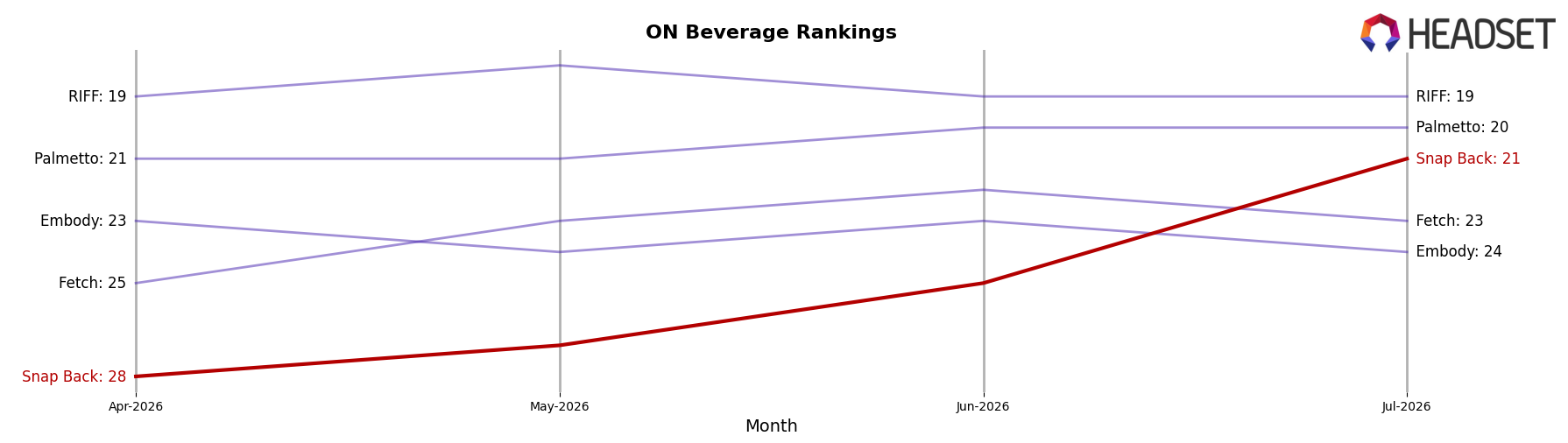

Snap Back sits at #21 in ON Beverage in July 2026, improving 8 ranks year over year from #29, and rising 7 positions from April 2026 when it was #28; this marks a new peak rank of #21 in July 2026 while the category leader mix shifted as Versus advanced from #3 to #1 and XMG fell from #1 to #2 with a -37.2% sales change, contrasting with Ray's Lemonade moving from #5 to #4 on +28.7% and Mary Jones climbing from #8 to #5 on +56.1% while Mollo slipped from #2 to #3 on -1.1%; the pattern implies Snap Back’s upward rank mobility is tied to mid-tier churn and leader volatility, creating a window to consolidate gains before faster-rising competitors compress the #15–#25 band.

Notable Products

Blackberry Creamsicle Rosin Soda (10mg THC, 12oz, 355ml) posted a 102.2% month-over-month surge to crack rank 4, while Strawberry Vanilla Cream Soda (10mg THC, 12oz, 355ml) rose 29.2% to hold rank 1. Blackberry Vanilla Cream Soda (10mg THC, 355ml) climbed 27.4% at rank 2, and Blood Orange Creamsicle Soda (10mg THC, 355ml) in rank 3 added 8.8%, with three of the top four concentrated in cream soda variants. The outsized gain in the rosin SKU alongside steady rank 1–3 performance implies Snap Back is pivoting toward higher-potency or premium formulations without diluting momentum in its core cream soda line.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.