Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

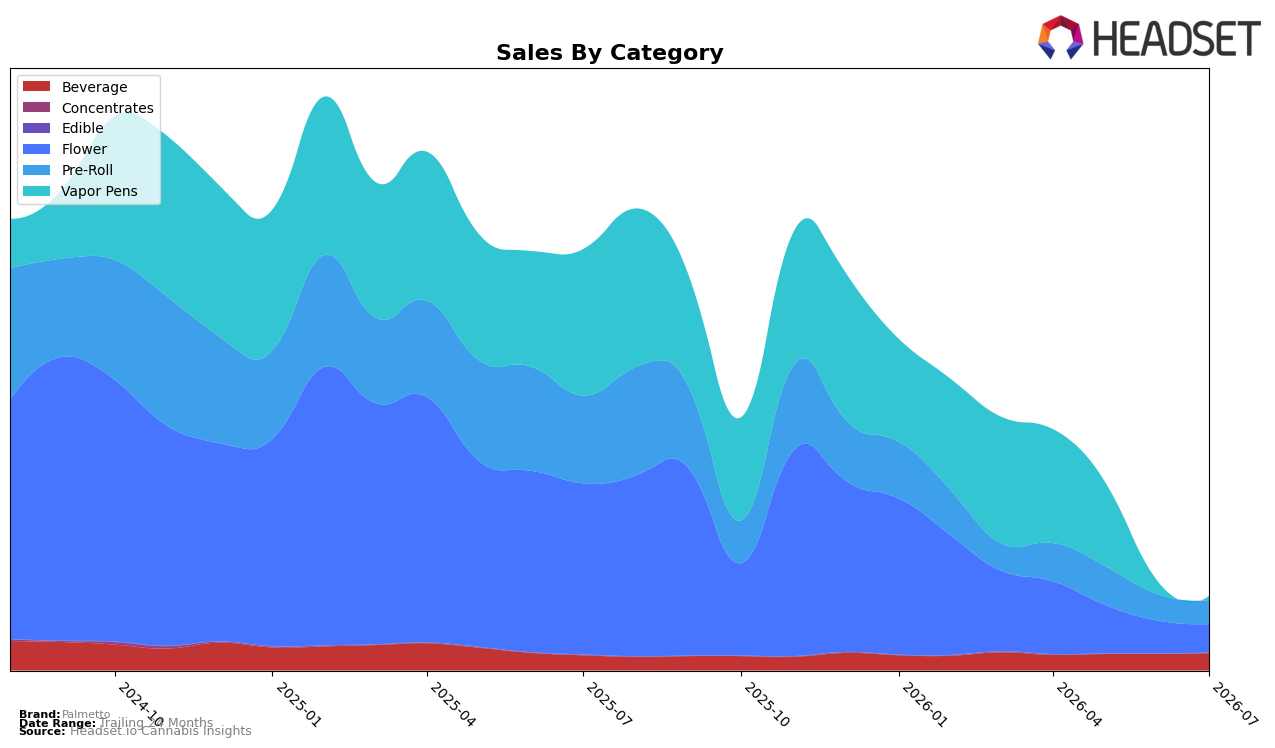

In July 2026, Palmetto’s mix tilted toward Flower at 38.8% share despite a year-over-year decline of 83.5% and a month-over-month drop of 13.1%, while Pre-Roll held 32.6% share with a 72.9% YoY decline and a 9.5% MoM decline. Beverage expanded to 23.5% share on 14.4% YoY growth and 4.6% MoM growth, contrasting with Vapor Pens at 5.2% share after a 97.4% YoY collapse and a 70.2% MoM contraction; the brand’s overall average price fell 51.3% YoY and Flower’s rank in British Columbia sat at 74. The pattern implies a pivot from inhalables toward value Beverage units as volume holds in lower-priced formats while legacy inhalables compress in both price and velocity.

These shifts point to a positioning anchored in entry-price and accessible formats: Beverage’s double-digit growth (14.4% YoY, 4.6% MoM) alongside a $5.76 average price indicates a demand corridor Palmetto can scale, whereas deep declines in Flower (83.5% YoY, 13.1% MoM) and Vapor Pens (97.4% YoY, 70.2% MoM) suggest shrinking consideration within higher-priced inhalables. With Pre-Roll still commanding 32.6% share but falling 72.9% YoY, and Flower ranked 74 in British Columbia, the implication is to consolidate around Beverage-led traffic and selectively defend Pre-Roll price tiers, rather than chase premium inhalable segments where price cuts of 51.3% YoY have not stabilized rank.

Competitive Landscape

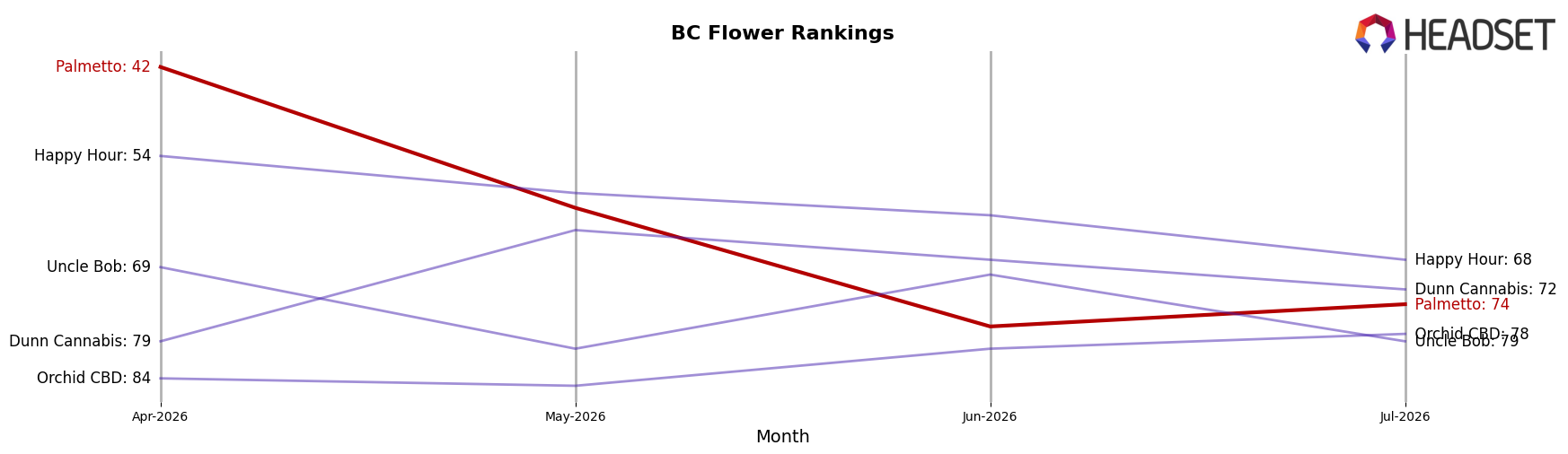

Palmetto sits at rank #74 in July 2026, down 53 positions year over year from #21, and down 32 spots versus April 2026 when it was #42; the trajectory from a peak of #13 in July 2024 to #74 now marks a multi-quarter slide. In contrast, Big Bag O' Buds is #1 with a +6.42% sales YoY change while climbing two ranks, and Good Supply is #2 after rising six ranks with +42.92% YoY sales growth; even Spinach advanced to #3 with a five-rank climb and +25.41% YoY sales. Meanwhile, The Original Fraser Valley Weed Co. slid to #4 with -23.87% YoY sales and Bake Sale is #5 with -15.59% YoY sales, indicating Palmetto’s decline is steeper in rank terms than some peers’ sales drops. The pattern implies Palmetto’s market position is being displaced by competitors that are adding share through rank gains despite mixed category YoY sales, so reversing the rank descent likely requires actions that address both visibility and relative velocity.

Notable Products

PALS - Blue Cheese Pre-Roll 10-Pack (4g) posted the steepest decline at -13.9% MoM while sliding to rank 4, whereas Orange Vanilla Cream Soda (10mg THC, 355ml) inched up 4.6% MoM to hold rank 1 with $44,445, indicating mix pressure away from one legacy pre-roll even as the lead beverage sustains share. Apple Jack (28g) climbed 28.1% MoM to rank 5 as Flower added depth, and Pre-Rolls occupied four of the top ten but included a -7.4% MoM dip for Orange Bud Blunt 5-Pack (2g), implying the category is bifurcating between value erosion and premium or novelty-led pockets. The pattern suggests Palmetto’s near-term commercial direction tilts toward defending the Beverage anchor while reallocating push into scalable Flower gains and selective pre-roll innovation rather than across-the-board pre-roll volume.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.