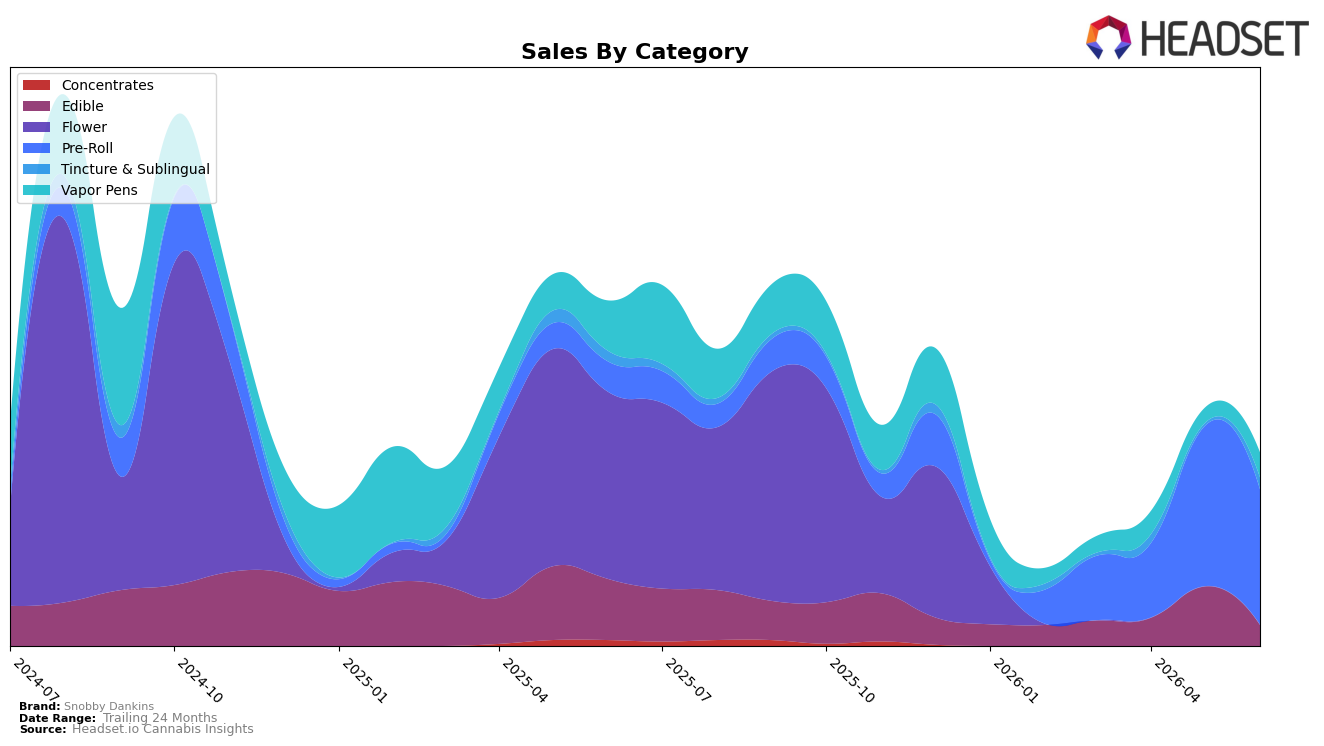

Market Insights Snapshot

In June 2026, Snobby Dankins concentrated 70.38% of sales in Pre-Roll on 350.02% year-over-year growth despite a 15.43% month-over-month decline, while Vapor Pens held 12.94% share with a 50.51% YoY drop but a 64.41% MoM rebound. Edible fell to 10.73% share with a 66.11% YoY and 65.16% MoM decline, and Tincture & Sublingual reached 5.96% share on 11.85% YoY growth and a 359.44% MoM surge; average price fell 42.15% YoY to $15.54. With overall brand sales down 44.18% YoY but up 61.44% over 24 months, the pattern implies a pivot toward value-priced Pre-Rolls and opportunistic re-entry via Tincture & Sublingual, while Edible contraction reduces exposure to New York category rankings.

The mix shift signals a positioning tradeoff: gaining transaction velocity via lower-price Pre-Rolls (share up to 70.38% as avg price in that segment sits at $13.12) while ceding premium share where Vapor Pens declined 50.51% YoY even with a 64.41% MoM bounce. The 359.44% MoM spike in Tincture & Sublingual alongside a 65.16% MoM pullback in Edible suggests resource reallocation into niche formats to offset volatility, implying Snobby Dankins is prioritizing basket-entry and trial over higher-priced differentiation, which may constrain pricing power even as it stabilizes unit throughput.

Competitive Landscape

Snobby Dankins sits at rank #82 in NY Edible for June 2026, down 27 spots year over year from #55, and essentially flat versus March 2026 at #83; the brand’s peak of #48 in September 2024 underscores a 34-rank slide since that high-water mark. Competitively, Off Hours moved down from #1 to #2 while Wyld held steady at #3 with 26.03% YoY sales growth, indicating that Snobby Dankins’ drop contrasts with stable or improving positions among category leaders; this trajectory implies that without a rank-recovery catalyst, Snobby Dankins is ceding long-term share to higher-ranked incumbents.

Notable Products

The Durbanator Pre-Roll 5-Pack (2.5g) sets the tone for June 2026 with a -22.6% month-over-month drop and a fall to rank 6, while Table Breakers - Sour Blue Raspberry Gummies 10-Pack (100mg) declines -39.2% at rank 8, implying volume is consolidating away from multipacks and non–Pre-Roll formats. At the top, Mixtape Vol 2 Infused Pre-Roll 2-Pack (1g) sits at rank 1 with share concentrated in two-pack infused SKUs, contrasted by Gorilla Mac Pre-Roll 5-Pack (2.5g) sliding -13.2% to rank 7, pointing to a favoring of smaller count packs over five-packs. Capital Kush Pre-Roll 2-Pack (1g) rises +18.3% at rank 2 alongside FLX Runtzilla Pre-Roll 2-Pack (1g) up +28.3% at rank 5, and eight of the top ten are Pre-Roll SKUs, signaling a lineup skew that rewards compact, infused formats even as larger multipacks lose pace. The pattern implies Snobby Dankins is tilting toward high-turn, infused two-packs and away from bulk packs and edibles, concentrating demand where trial and quick replenishment are highest.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.