Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

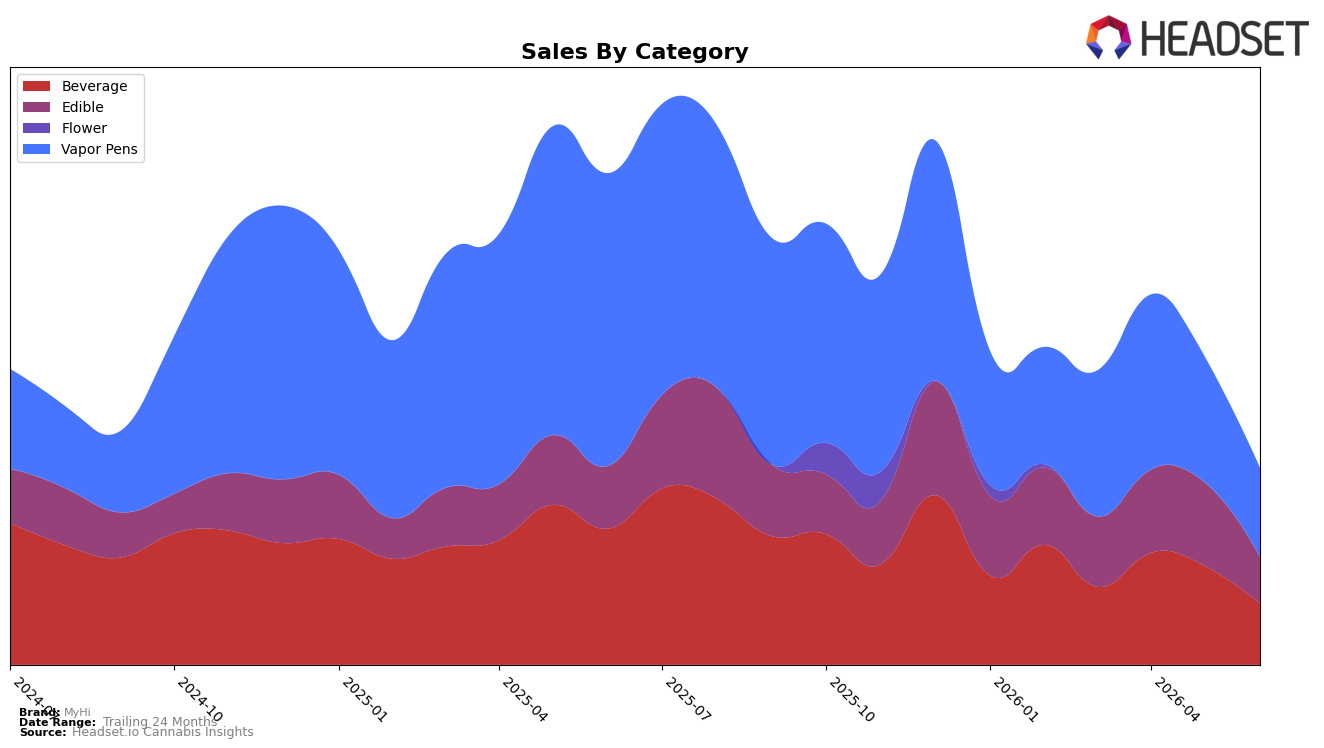

In June 2026, MyHi’s mix concentrated in Vapor Pens at 45.39% share, with Beverage at 31.13% and Edible at 23.48%, while category-level declines diverged: Vapor Pens fell 69.54% YoY and 29.11% MoM, Beverage dropped 55.12% YoY and 38.20% MoM, and Edible contracted 26.17% YoY and 44.62% MoM. The brand’s overall sales were down 60.03% YoY alongside a 17.14% YoY price decrease to $31.86, and within its anchor segment of Vapor Pens MyHi held rank 98 in New York, implying a scale-led vulnerability where heavier exposure to the most-declining segment (Vapor Pens) amplified total contraction versus the relatively less-severe Edible trajectory.

The sharper MoM pullbacks in Beverage (down 38.20%) and Edible (down 44.62%) versus Vapor Pens (down 29.11%) indicate a short-term retrenchment away from secondary formats even as long-run YoY risk is highest in Vapor Pens (down 69.54%), with June 2026 share still anchored there at 45.39% and rank 98 in New York. This mix-path suggests MyHi’s positioning is being set by a high-volatility core segment that drags annual performance while near-term share defense leans on the same segment, implying that reallocating toward the comparatively milder YoY decline in Edible (down 26.17%) could reduce variance but would require absorbing steeper near-term MoM softness.

Competitive Landscape

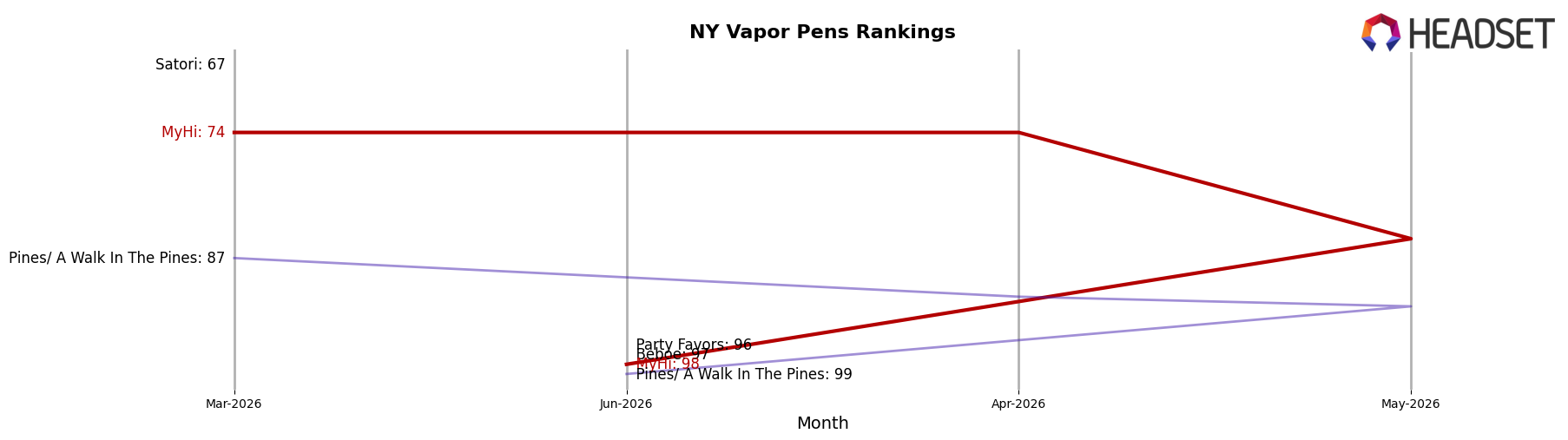

MyHi ranks #98 in NY Vapor Pens in June 2026, down 53 positions year over year from #45, and down 24 positions versus March 2026 when it was #74; meanwhile, Jaunty held at #1 year over year while Fernway moved up from #3 to #2. Compared with its peak at #45 in June 2025, the current #98 rank places MyHi 53 spots below its best, while Jetty Extracts surged from #23 to #5 with 238.23% YoY sales growth; this widening gap implies MyHi’s distribution or velocity has thinned relative to faster-ascending peers and that retention or assortment choices likely shifted away from the brand.

Notable Products

THC/CBD 1:1 Relax Indica Grape Live Rosin Gummies 10-Pack (100mg THC, 100mg CBD) posted the steepest decline at -79.13% and slipped to rank 10, while CBD/THC 1:3 Sour Diesel Live Rosin Disposable (1g) inched up 2.57% to hold rank 1. In contrast, THC/CBD 2:1 Super Tangerine Gummies 10-Pack (100mg THC, 50mg CBD) climbed 23.52% to rank 2, but its sibling THC/CBD 2:1 Super Sativa Berry Gummies 10-Pack (100mg THC, 50mg CBD) fell -23.36% at rank 3. Four of the top ten are Beverage stir sticks with MoM drops between -18.90% and -54.36% and two Vapor Pens split directionally with a -42.34% decline at rank 9 versus a rank-1 holder, implying the mix is tilting toward a single premium pen anchor while value-oriented beverages and several CBD/THC parity gummies are cycling down.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.