Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

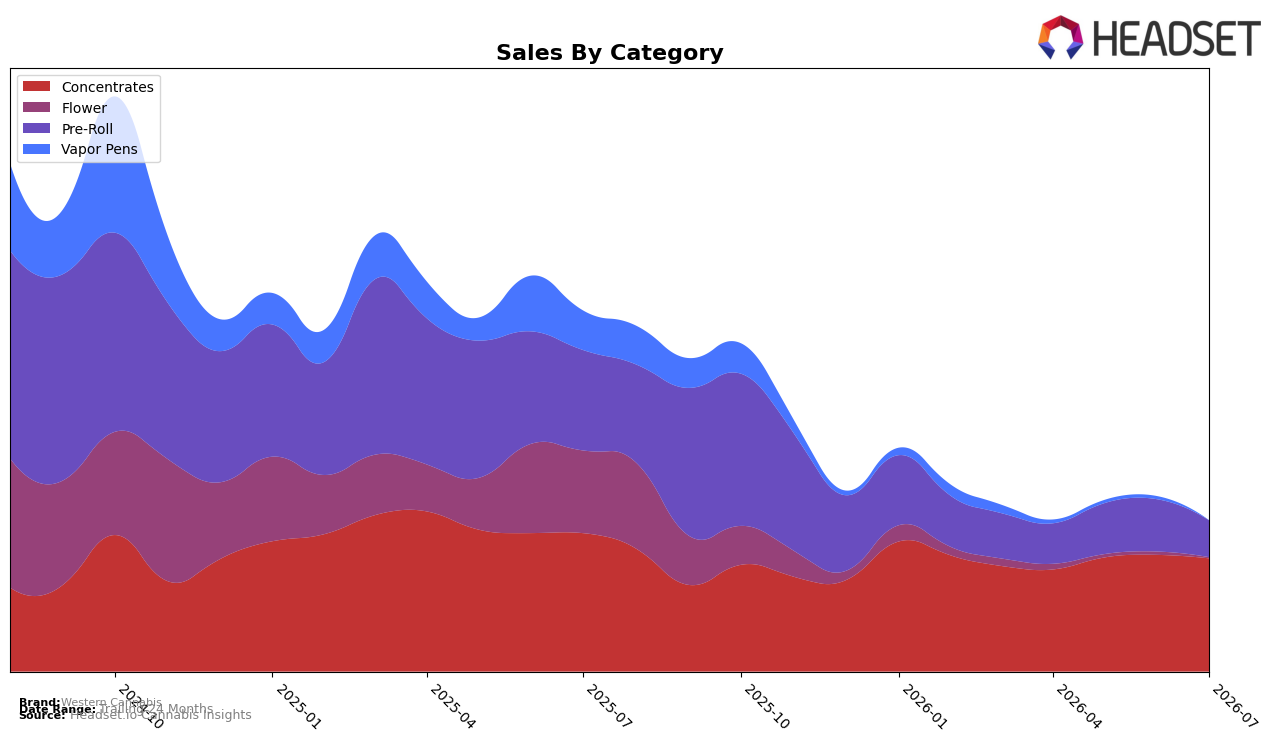

Western Cannabis concentrated into Concentrates at 74.02% share in July 2026 while Pre-Roll fell to 24.33%, with Flower and Vapor Pens together at just 1.66% share; this mix coincides with brand sales down 57.70% year over year and average price down 5.54%. Within categories, Concentrates declined 18.14% YoY and 2.95% MoM, whereas Pre-Roll contracted 62.96% YoY and 29.12% MoM, and the tail categories collapsed 97.88% and 98.06% YoY respectively; the pattern implies Western Cannabis is consolidating around Concentrates while exiting or deprioritizing low-scale segments.

Given a rank of 1 in Concentrates in Saskatchewan and a 74.02% internal mix weight, Concentrates serves as the positioning anchor, but the 18.14% YoY decline alongside a 29.12% MoM drop in Pre-Roll signals an overdependence risk if category headwinds persist. With average price at $27.46 and category prices ranging from $22.73 in Pre-Roll to $40.69 in Flower, the 5.54% YoY brand-wide price reduction likely aims to defend share in Concentrates while shedding unprofitable volume in Pre-Roll and Vapor Pens; the implication is that Western Cannabis is trading breadth for depth, prioritizing rank defense in a single category over multi-category presence.

Competitive Landscape

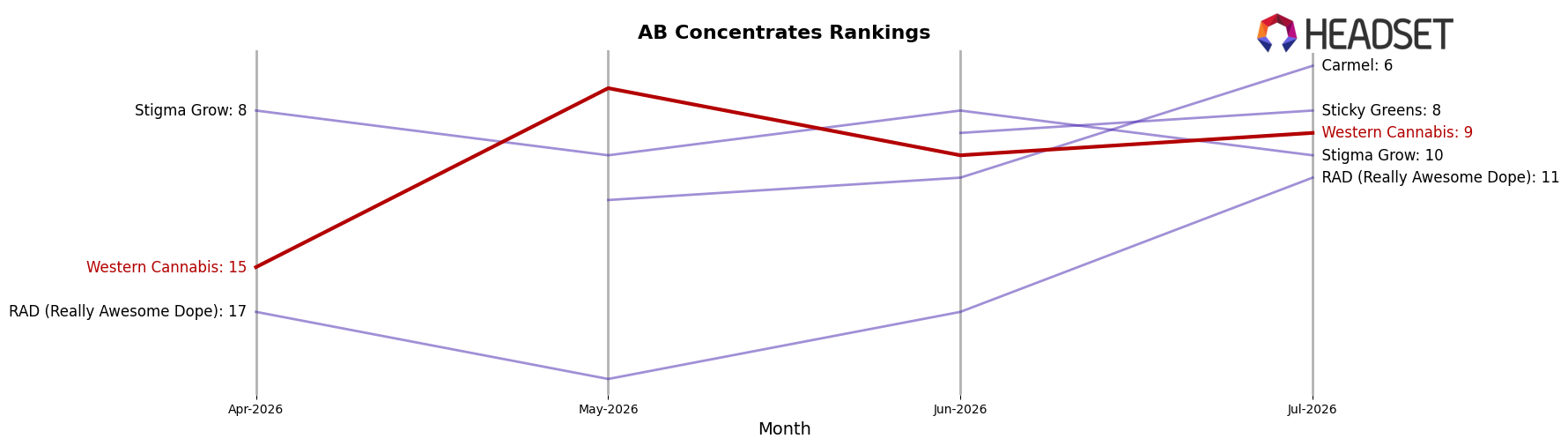

Western Cannabis is ranked #9 in AB Concentrates in July 2026, down 2 positions year over year from #7 and up 6 positions from April 2026’s #15, while its peak of #5 in February 2026 indicates mid-year slippage from earlier momentum; by contrast, BoxHot moved from #2 to #1 with 25.98% year-over-year sales growth and Endgame fell from #1 to #2 alongside a 25.49% year-over-year sales decline, signaling that leadership is rotating toward brands gaining share while laggards give up rank. Combined with Dab Bods holding #3 on 83.12% growth and 3Saints rising from #5 to #4 with 50.39% growth, the pattern implies Western Cannabis’s rank trajectory is stabilizing below the leaders and will require outpacing double-digit growth peers to re-enter the top 5.

Notable Products

Electric Cherry Shatter (1g) posted the steepest decline at -13.3% while holding rank 3, and Lime Soda Infused Pre-Roll 3-Pack (1.5g) fell -40.3% at rank 6, signaling a widening gap between concentrates and pre-rolls. Multipack of Madness Shatter (1g) rose +26.2% to rank 1 while Orange Creamsicle Shatter (1.2g) dipped -3.3% at rank 2, and five of the top ten are Concentrates, pointing to category concentration at the top. Orange Creamsicle Pre-Roll 12-Pack (6g) dropped -35.2% at rank 8 as Matanuska TF Shatter (1g) slid -35.5% at rank 9, and Grape Slushee Shatter (1g) inched +3.3% at rank 4 against Sour Watermelon Shatter (1g) up +15.4% at rank 5, implying product momentum is clustered in value-forward shatter while multi-pack pre-rolls retrench. The mix suggests Western Cannabis is leaning into shatter-led share defense rather than broad-based pre-roll expansion, with July 2026 performance reinforcing a concentrate-first commercial path anchored by a single top SKU delivering $31,822.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.