Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

In July 2026, Natural History’s mix pivoted toward Pre-Roll at 55.36% share with year-over-year growth of 11.37% and month-over-month acceleration of 51.22%, while Flower contracted to 41.40% share with a year-over-year decline of 61.84% and a month-over-month drop of 35.13%; Vapor Pens remained a small 3.25% share but expanded 30.34% year-over-year and 32.59% month-over-month. Despite a brand-level year-over-year sales decline of 37.77% and an average price decrease of 5.86%, Natural History held a Pre-Roll category position at rank 51 in Alberta, implying that the top-line contraction is being counterbalanced by mix gains in faster-moving formats and a price-led volume strategy in July 2026.

The shift toward Pre-Roll, coupled with Vapor Pens’ double-digit month-over-month and year-over-year gains, suggests a deliberate tilt to quicker-turn, lower-ticket formats as Flower’s deep 61.84% year-over-year decline and 35.13% month-over-month pullback reduce reliance on a high-price segment. With Pre-Roll now leading share at 55.36% and the brand priced at an average of $27.94 alongside a 5.86% year-over-year price reduction, the July 2026 configuration points to a positioning that prioritizes penetration and basket frequency over premium Flower depth, aiming to trade off some average ticket for higher unit velocity and to solidify relevance in Alberta where the current Pre-Roll rank is 51.

Competitive Landscape

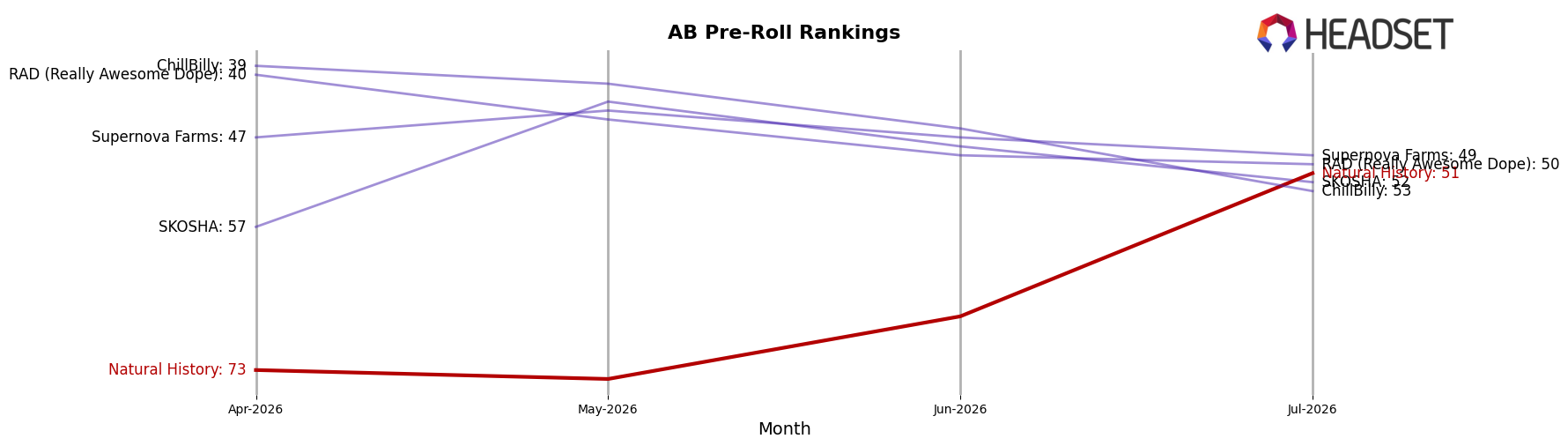

Natural History is currently ranked #51 in AB Pre-Roll, improving 8 positions year over year from #59, and climbing 22 spots versus April 2026 when it sat at #73; this July 2026 peak at #51 contrasts with General Admission holding at #1 year over year while posting a -14.5% sales change, and Back Forty / Back 40 Cannabis moving from #6 to #2 alongside a 34.3% sales increase. Against a mixed top tier where Space Race Cannabis slipped from #2 to #3 with -37.9% sales and Thumbs Up Brand jumped from #19 to #5 with 138.3% growth, Natural History’s steady rank ascent from #73 in April 2026 to #51 in July 2026 indicates momentum into the mid-pack that can convert into share if maintained as leaders either contract or churn.

Notable Products

Natural History Unlimited Blunts 3-Pack (1.5g) posted the most dramatic move in July 2026 with +188.2% month over month while holding rank 3, contrasted by Limited Reserve Hybrid Pre-Roll 3-Pack (1.5g) dropping -62.0% at rank 9. Ego Checker Pre-Roll 7-Pack (3.5g) surged +138.7% to rank 2 as AK Funk Pre-Roll 3-Pack (1.5g) rose +49.1% at rank 1, and five of the top ten are Pre-Roll SKUs, concentrating share in value multipacks. Limited Reserve - Rainbow Sherbert #11 (7g) fell -13.6% at rank 4 as Ego Checker (7g) slid -42.2% at rank 7, indicating Flower softness even as one Pre-Roll newcomer entered at rank 8 with no prior month baseline. The mix implies a pivot toward multi-pack Pre-Rolls as the commercial engine, with Flower de-emphasis likely continuing unless pricing or strain rotation reverses the -10% to -42% declines.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.