Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

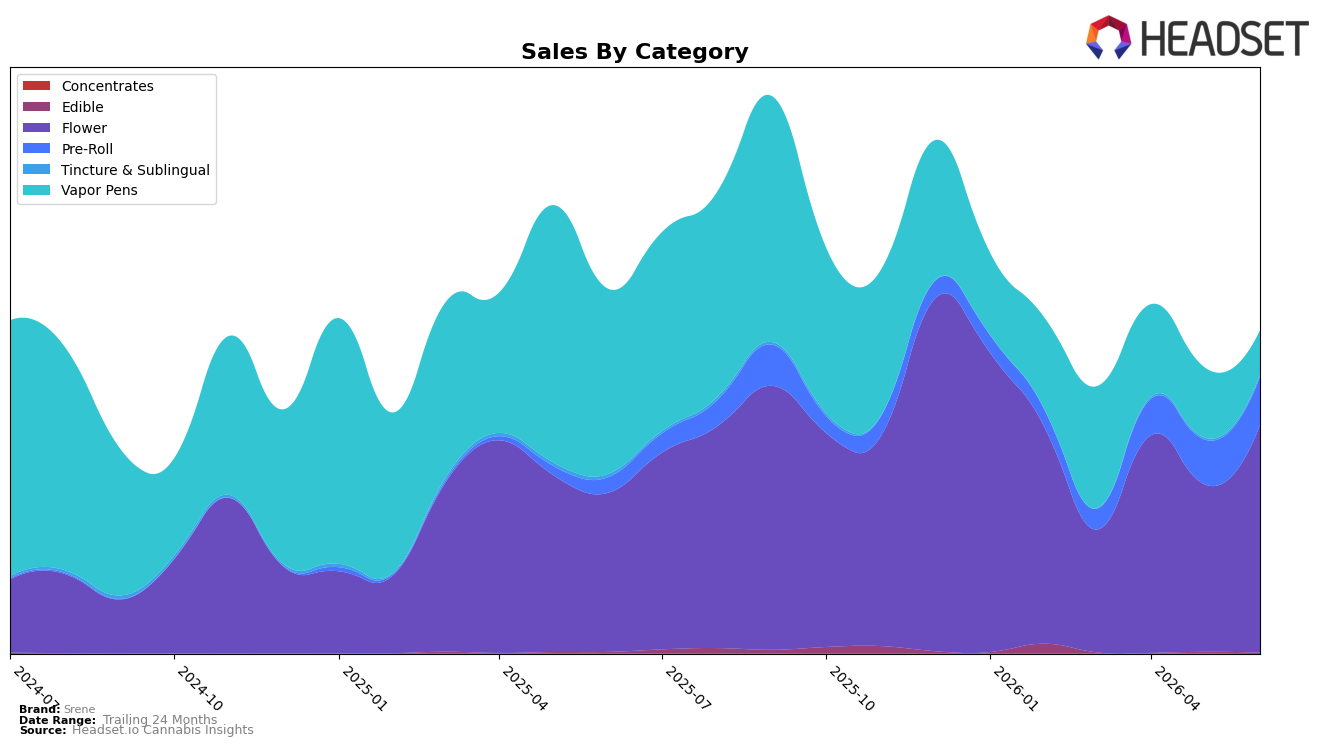

In June 2026, Srene leaned heavily into Flower at 70.68% share with year-over-year growth of 43.19% and month-over-month growth of 36.05%, while Pre-Roll expanded to 14.86% share with a 212.43% year-over-year increase and a 7.58% month-over-month lift. Vapor Pens contracted to 13.70% share with a 76.15% year-over-year decline and a 37.03% month-over-month drop, offsetting gains elsewhere as total brand sales fell 11.42% year-over-year despite a 17.19% decline in average price. The mix shift implies Srene is concentrating volume in lower-priced inhalables, using Pre-Roll momentum to backfill Vapor Pen losses, with Concentrates’ 197.32% month-over-month uptick from a 0.19% share and Tincture & Sublingual’s 14.04% month-over-month rise at 0.57% share adding only marginal ballast.

The category tilt raises Srene’s exposure to Flower pricing cycles and Pre-Roll promotional intensity, which could explain why share gains in Flower and Pre-Roll did not prevent a 7.19% two-year sales contraction alongside a rank of 17 in Flower for Nevada. With Flower averages at $32.67 and Pre-Roll at $9.39, the 17.19% average price compression suggests a deliberate trade-down strategy that stabilized unit throughput but deepened Vapor Pen attrition, so the near-term positioning is value-forward in inhalables with measured risk that June 2026 mix gains may not translate to sustained revenue without restoring Vapor Pen contribution.

Competitive Landscape

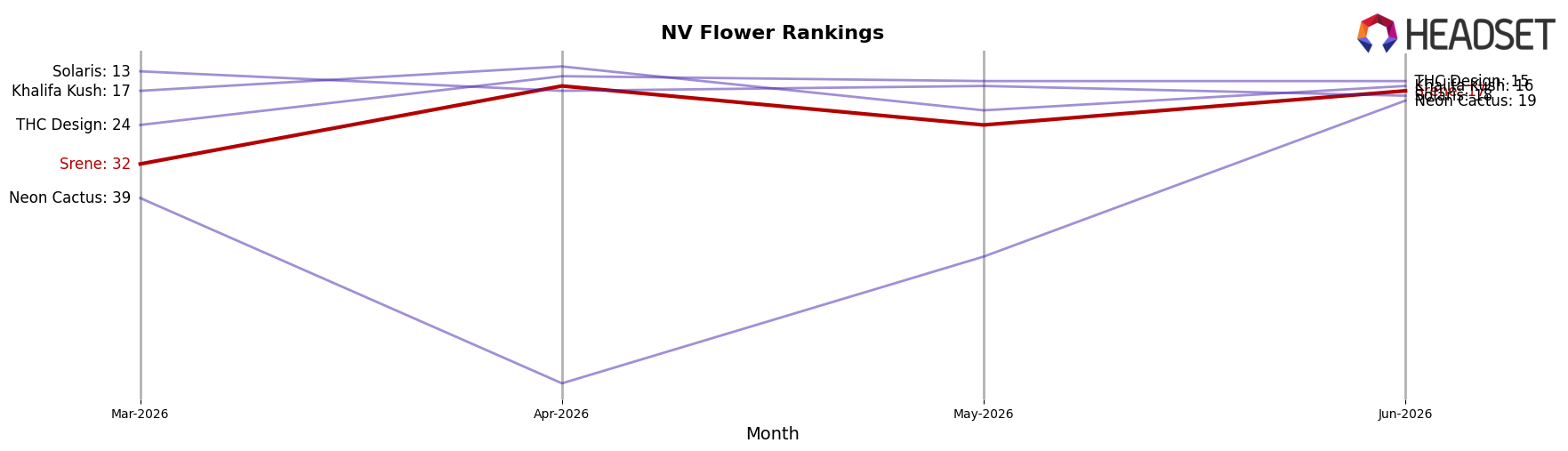

Srene sits at rank #17 in June 2026, improving 8 positions from #25 year over year and jumping 15 positions from #32 in March 2026, while still trailing its peak of #11 in December 2025; meanwhile, STIIIZY held steady at #1 with a 5.2% YoY sales increase and RYTHM advanced from #4 to #2 despite a -6.9% YoY sales decline, indicating that Srene’s mid-tier climb is outpacing recent months’ position but not yet converting into top-10 reentry, which implies a recovery trajectory that is improving in rank velocity yet still short of sustained category leadership.

Notable Products

DayStripper (14g) delivered the headline move in June 2026 with a 170.4% month-over-month surge to rank 1, while Sin City Funk Pre-Roll (1g) fell 12.5% to rank 8 and Space Junky Pre-Roll (1g) declined 17.4% at rank 10. Flower SKUs occupy 6 of the top 10 including ranks 1, 2, and 3, whereas Pre-Roll entries at ranks 4, 6, 8, and 10 posted mixed signals with +0.7% and +10.6% gains offset by double-digit drops. Limesicle (14g) and Stripper Glitter (14g) held ranks 2 and 3 without reported month-over-month rates, setting a concentration alongside DayStripper that tilts the leaderboard toward larger 14g formats; this mix implies Srene is pulling volume through value-oriented Flower packs over Pre-Rolls, pointing to a pricing/size-led strategy rather than format diversification.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.