Where to Buy

Dope Dope is stocked at 28 licensed dispensaries across Nevada and Michigan, 26 of them in Nevada, with the deepest coverage in Las Vegas, Reno, Henderson, Carson City, and North Las Vegas. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

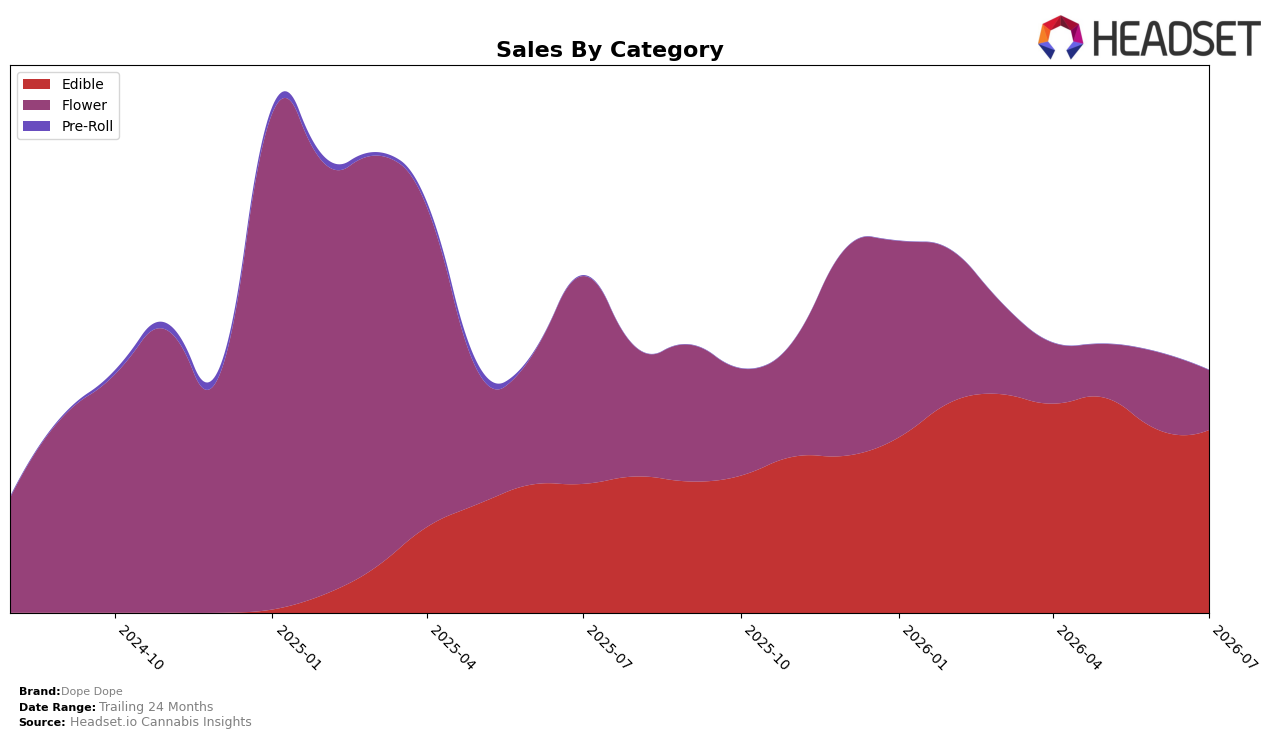

Market Insights Snapshot

Dope Dope concentrated 75.45% of July 2026 sales in Edible, up 41.83% year over year and down 0.20% month over month, while Flower fell to 24.55% share with a 71.31% YoY decline and a 22.83% MoM drop; this shift coincides with an average price decline of 43.22% YoY to $3.52 and a category-level Edible average price of 2.69. In Michigan Edible, the brand sat at rank 35, and total brand sales were down 28.05% YoY despite a 54.26% lift over 24 months, implying the portfolio is tilting toward lower-priced Edible volume while legacy Flower is contracting rapidly.

The mix pivot suggests Dope Dope is competing more on price-driven velocity in Edible—where rank 35 signals mid-pack breadth—than on premium positioning in Flower, where a 71.31% YoY contraction and 22.83% MoM slide point to weakened presence. With Edible only slightly negative MoM at 0.20% versus Flower’s 22.83% MoM decline, maintaining Edible share near 75% and a 2.69 average price implies the brand’s near-term positioning leans on affordable, high-turn SKUs in Michigan Edible while de-prioritizing Flower until price or rank dynamics improve.

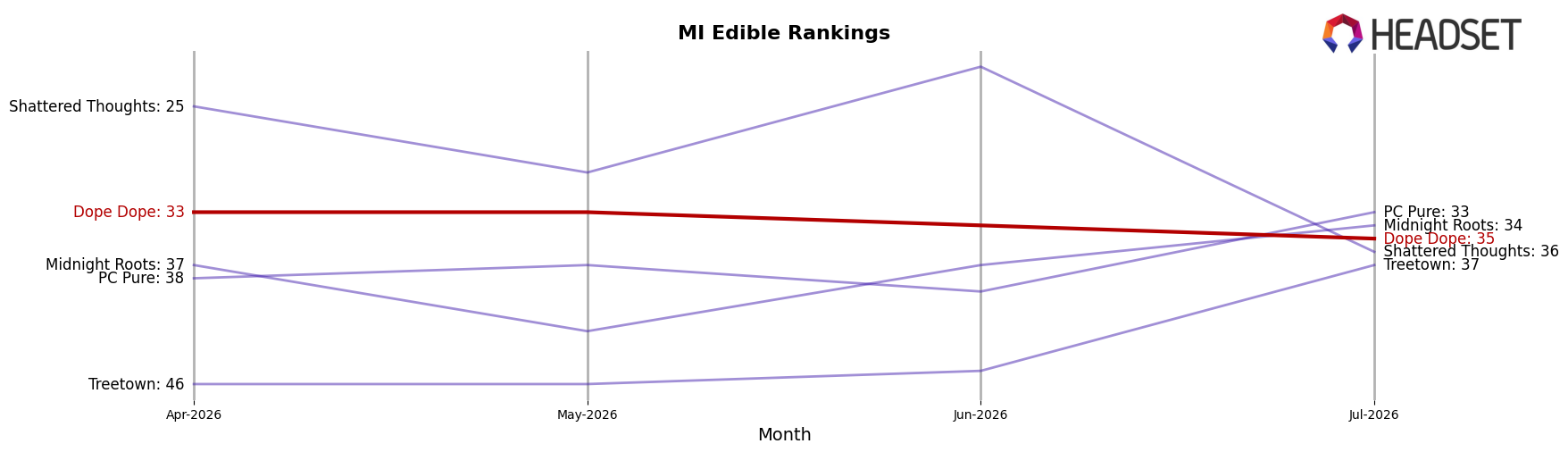

Competitive Landscape

Dope Dope is ranked #35 in MI Edible in July 2026, improving 12 positions from #47 year over year, but sliding 2 spots from #33 in April 2026, with a prior peak at #26 in February 2026; meanwhile, Wyld held #1 year over year and in July 2026 despite a -23.3% YoY sales change, and MKX Oil Company eased from #3 to #4 while posting +4.6% YoY sales, indicating Dope Dope’s rank gains are coming more from mid-pack churn than from displacing the top tier.

Notable Products

Grapes and Cream (14g) posted the steepest decline in July 2026 at -58.2% MoM and slid to rank 9, while Wedding Pie (14g) fell -49.0% to rank 10; in contrast, Grape Trip Gummy (200mg) rose 27.9% MoM and reached rank 6. Strawberry Banger Gummy (200mg) held rank 1 with a 5.3% MoM lift, and Wacky Watermelon Gummy (200mg) stayed at rank 2 with a 9.0% gain, indicating four of the top ten are Edible SKUs concentrated at ranks 1–6. This split—sharp double-digit declines in 14g Flower against steady single-digit gains and a high-20s riser in Edibles—implies Dope Dope’s mix is tilting toward Edibles as the growth engine while smaller-format Flower retrenches.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.