Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Stratos is stocked at 113 licensed dispensaries across Colorado and Washington, 111 of them in Colorado, with the deepest coverage in Denver, Colorado Springs, Aurora, Boulder, and Fort Collins. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

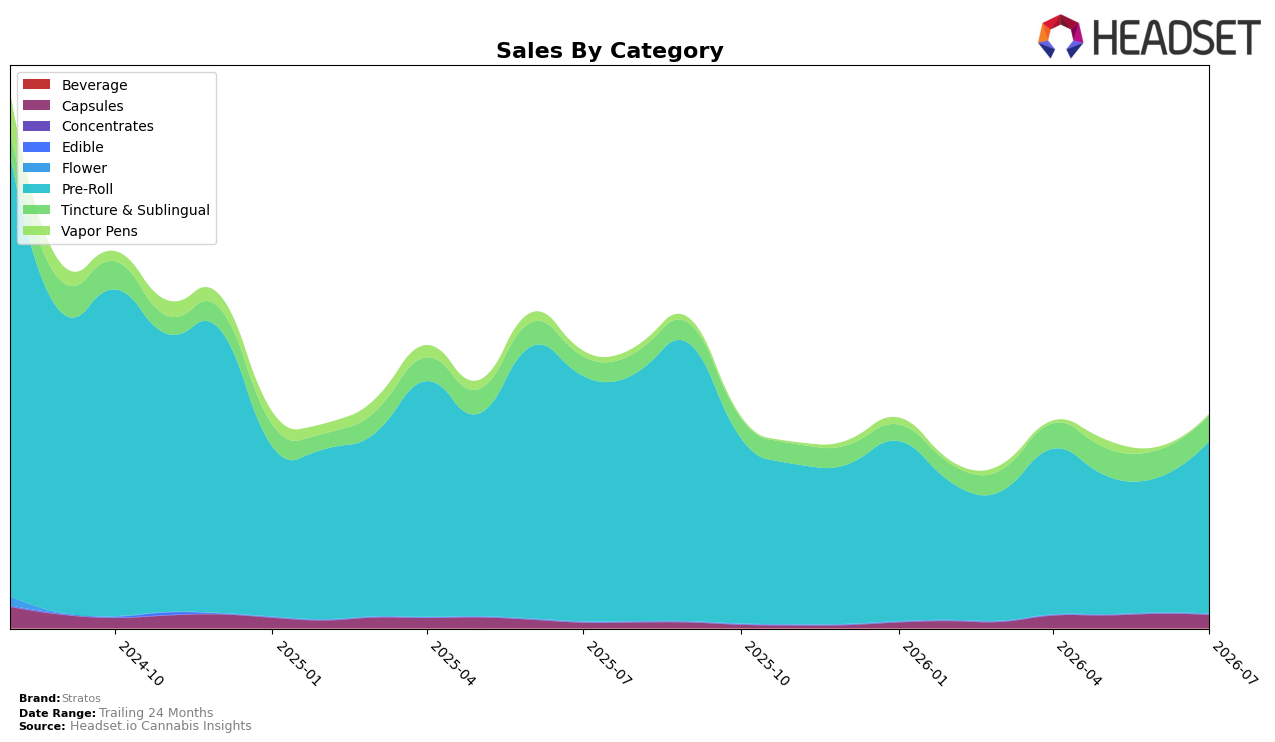

Stratos concentrated 81.24% of July 2026 sales in Pre-Roll, where year-over-year sales fell 29.93% but month-over-month rose 27.66%, while Tincture & Sublingual held 12.07% with a 32.80% YoY gain and a 5.66% MoM decline. Capsules expanded to 6.12% share with 150.74% YoY growth despite a 7.64% MoM pullback, and Vapor Pens shrank to 0.58% share after a 76.54% YoY and 57.42% MoM drop. Against a total brand sales change of -23.04% YoY and an average price decline of 11.55%, this mix implies reliance on Pre-Roll for volume recovery while growth in Capsules and Tincture & Sublingual partially offsets category-specific drag.

Positioning-wise, a 27.66% MoM rebound in Pre-Roll alongside a 29.93% YoY contraction, combined with a category rank of 23 in Pre-Roll in Colorado, indicates Stratos competes mid-pack on a price-forward strategy with an overall average price of $12.82 and a Pre-Roll price at $11.87. The 150.74% YoY surge in Capsules against a 7.64% MoM dip, paired with Tincture & Sublingual’s 32.80% YoY increase and 5.66% MoM decline, suggests the brand is building a therapeutic-oriented halo that diversifies risk away from Pre-Roll cyclicality; the pattern points to a dual-track approach where Pre-Roll drives near-term share maintenance while Capsules and Tincture & Sublingual seed longer-term resilience.

Competitive Landscape

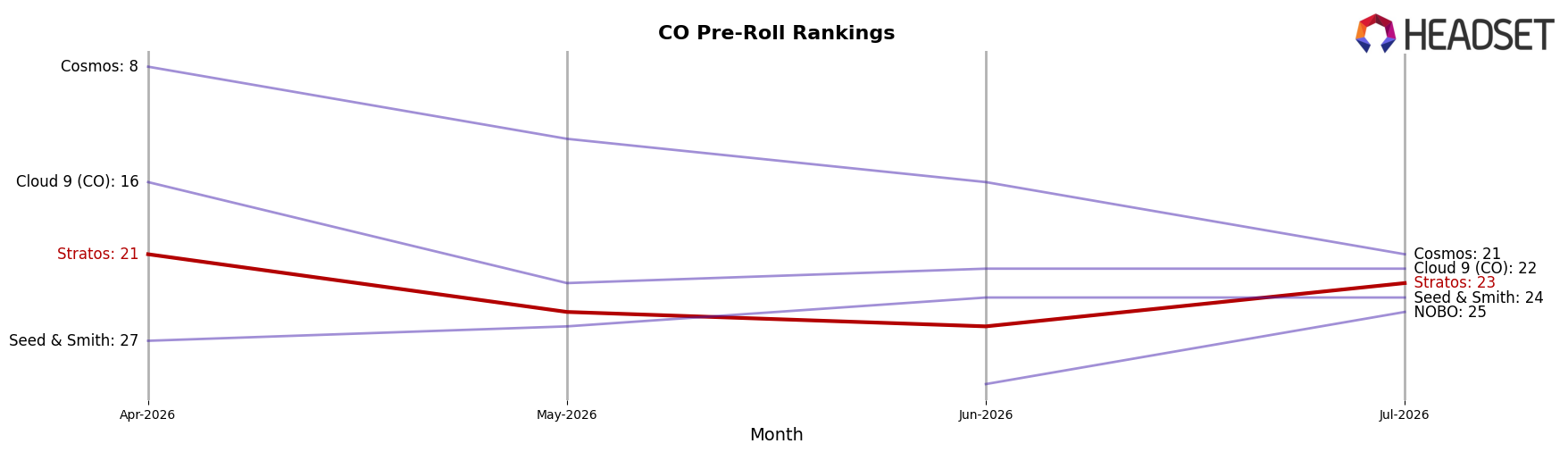

Stratos sits at rank #23 in Colorado Pre-Roll for July 2026, down 5 positions year over year from #18 and slipping 2 spots from April 2026’s #21, while still far off its peak of #6 in August 2024; in contrast, Green Dot Labs advanced from #3 to #1 with 91.9% YoY sales growth and TWAX jumped from #14 to #5 on 138.9% YoY growth, whereas Kaviar slid from #2 to #3 amid a 17.4% YoY decline. Against this backdrop, Cali-Blaze fell from #1 to #2 with a 0.4% YoY sales dip while Seed & Strain Cannabis Co. edged up from #5 to #4 with 47.2% YoY growth, indicating Stratos’s multi-quarter rank erosion reflects lost relative momentum versus peers expanding share at both the top and the fast-rising mid-tier.

Notable Products

Jupiter Joint - Pandora's Peach Infused Pre-Roll (1g) delivered the standout move in July 2026 with a 191.6% month-over-month surge to rank 1, while Dipper Joint - Pandora's Peach Infused Pre-Roll (0.5g) slid 19.6% and fell behind at rank 6. Jupiter Joints - Space Cowboy Infused Pre-Roll (1g) advanced 19.0% to rank 3 and Jupiter Joint- Moon Melon Infused Pre-Roll (1g) rose 22.9% to rank 5, whereas Slowburn - Super Boof Infused Pre-Roll (1g) declined 13.5% at rank 9. Four of the top ten are Pre-Roll SKUs within the Jupiter/Slowburn families concentrated in 1g formats, with only one notable 0.5g product in the top six, and the category’s leading position pairs a triple-digit gainer with two double-digit fallers. The pattern implies Stratos is consolidating around 1g infused pre-rolls with flagship momentum at the premium end, while smaller 0.5g line extensions face cannibalization and rank pressure.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.