Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Artizen Cannabis is stocked at 136 licensed dispensaries across Washington and California, 128 of them in Washington, with the deepest coverage in Seattle, Tacoma, Spokane, Bellevue, and Everett. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

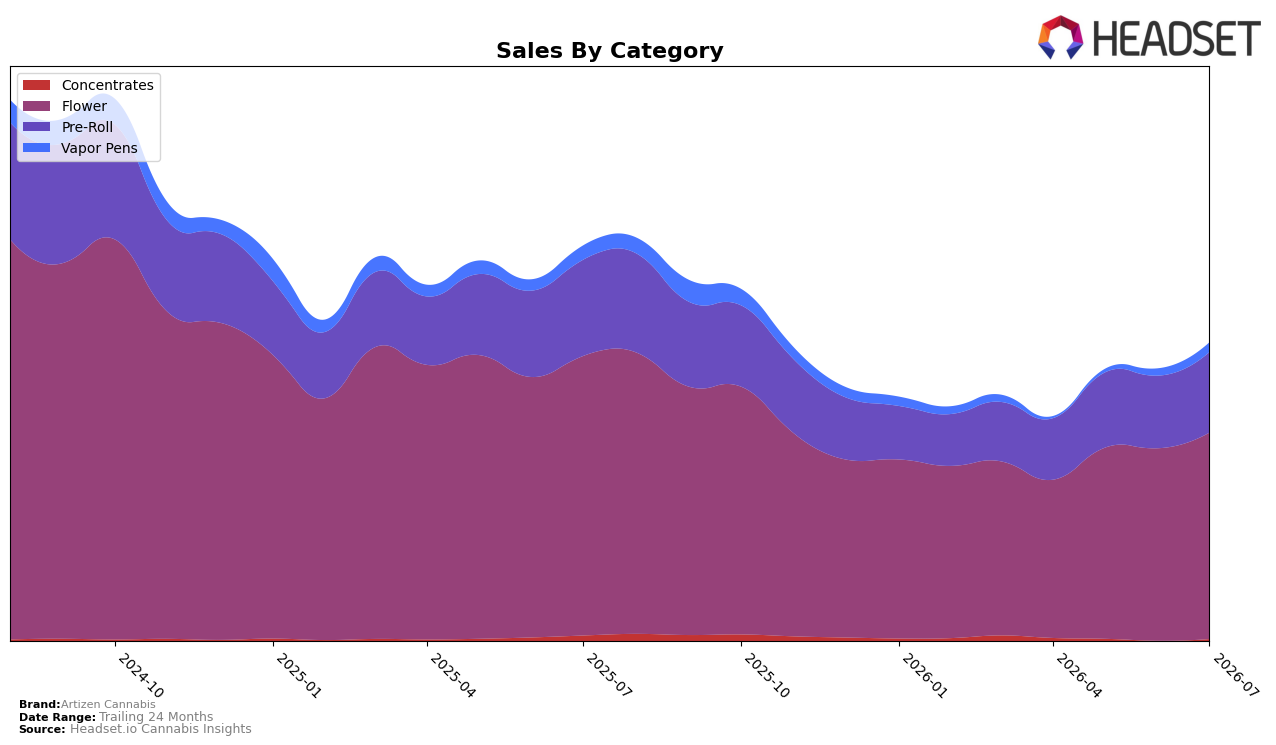

In July 2026, Artizen Cannabis concentrated 68.91% of sales in Flower, where year-over-year sales fell 26.11% while month-over-month rose 7.24%, and it held a rank of 13 in Flower in Washington. Pre-Roll carried 26.94% share with a 16.27% year-over-year decline and a 10.87% month-over-month rise, while Vapor Pens at 3.36% share dropped 31.21% year-over-year but climbed 32.22% month-over-month; Concentrates remained small at 0.78% share with a 60.28% year-over-year decline yet a 246.24% month-over-month surge. With brand-level sales down 24.41% year-over-year and average price down 3.71%, the mix points to reliance on Flower for scale and Pre-Roll for incremental recovery, implying that short-term momentum is being pulled by lower-priced formats even as the flagship Flower position at rank 13 caps upside.

The shifts imply a repositioning opportunity: Pre-Roll’s 10.87% month-over-month gain alongside a 3.71% brand-wide price decrease suggests elasticity that can absorb volume at mid-to-low price tiers, while Vapor Pens’ 32.22% month-over-month lift from a 3.36% share base signals headroom for mix diversification if retained above a 25–30% growth cadence. Concentrates’ 246.24% month-over-month bounce from 0.78% share does not offset a 60.28% year-over-year decline, indicating it functions as a tactical, not strategic, lever, whereas Flower’s 7.24% month-over-month increase against a 26.11% year-over-year drop and a rank of 13 in Washington implies that defending core shelf space while trading consumers into adjacent formats is the most viable path to stabilize the 24.41% brand sales contraction.

Competitive Landscape

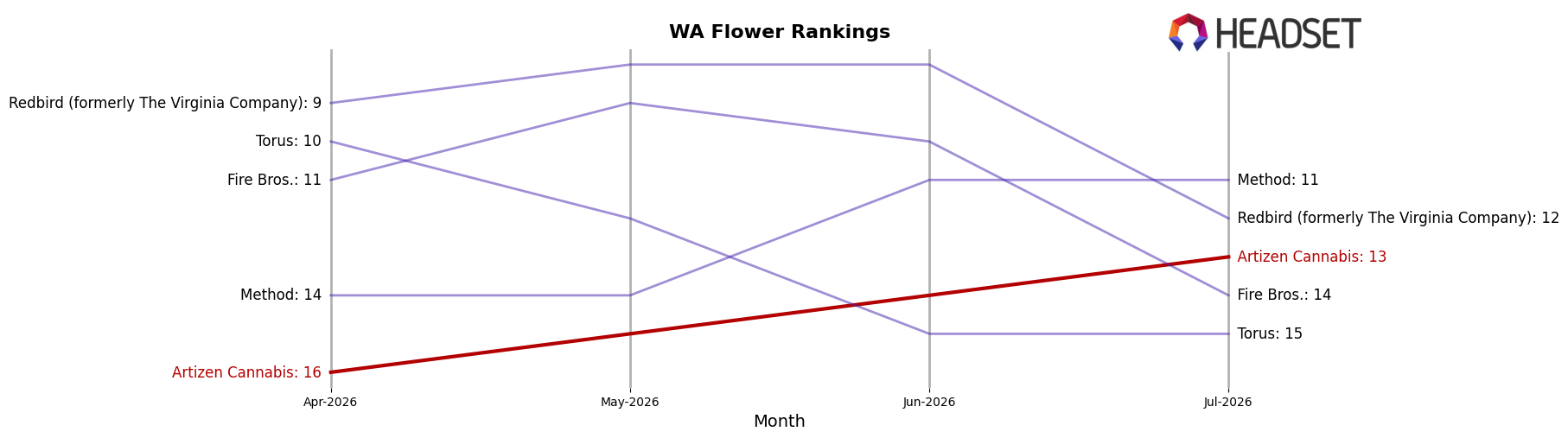

Artizen Cannabis sits at rank 13 in WA Flower in July 2026, down 7 spots year over year from rank 6, but up 3 positions from April 2026’s rank 16, while still well below its peak rank 3 from September 2024; in contrast, Phat Panda held rank 1 with an 18.6% year-over-year sales increase as Legends stayed at rank 2 despite a 22.9% year-over-year decline, and Lifted Cannabis Co climbed to rank 3 from rank 8 year over year with 13.1% growth; the combination of a 7-rank annual slide and a 3-position rebound over the last quarter implies Artizen Cannabis is stabilizing mid-pack but must outpace competitors who are either defending top slots or converting growth into rank gains.

Notable Products

Jack Herer (3.5g) posted the steepest decline at -8.16% month over month while slipping to rank 6, whereas Dutchberry (3.5g) rose 10.57% to rank 2 and Blue Dream (3.5g) advanced 11.22% at rank 5. Pre-Roll strength is concentrated with three of the top eight SKUs in July 2026, led by Dutchberry Pre-Roll 2-Pack (1g) up 10.33% at rank 1 and Jack Herer Pre-Roll 2-Pack (1g) up 9.84% at rank 4, implying the brand is leaning into convenient formats to stabilize velocity despite a mid-tier Flower softness.

Within Flower, Dutchberry (7g) added 5.81% at rank 7 while Mother of Berries (3.5g) eased -1.81% at rank 6, and Galactic Glue (3.5g) entered the top 10 at rank 9 without a reported month-over-month rate, totaling $14,508 in July 2026. The split performance—double-digit gains for two flagship eighths alongside a decline for Jack Herer (3.5g)—signals a portfolio tilt toward Dutchberry-led repeatability and format breadth over strain breadth for sustained shelf share.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.